Next Generation Anode Materials Market Size by Material, Application, End User and Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2032

Overview

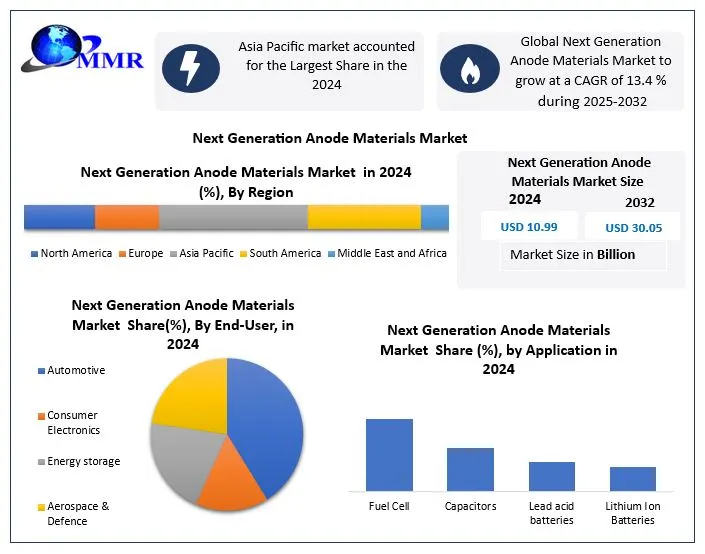

Next Generation Anode Materials Market was valued at USD 10.99 Bn in 2024, and the Global Next Generation Anode Materials Market is expected to reach USD 30.05 Bn by 2032, growing at a CAGR of 13.4 % during the forecast period.

Next Generation Anode Materials Market Overview:

Next Generation Anode Materials Market focuses on developing and commercializing advanced materials, such as silicon and lithium metal, for battery anodes. These materials aim to significantly improve energy density, fast-charging capabilities, and cycle life, primarily driven by the escalating demand for high-performance batteries in electric vehicles and consumer electronics.

Next Generation Anode Materials Market has been growing due to the rising demand of high-performance batteries, particularly in Electric Vehicles. This need drives development in materials such as silicon which has a better energy density and a higher charging rate. The market, however, does have considerable hindrances and difficulties, among them being the low levels of scalability and high production expenses of these hi-tech materials which necessitate intensive research and development investment and new procedures to manage. Asia Pacific dominated the Next Generation Anode Materials Market in 2024 and is also projected to dominate longer as rapid industrialization and the largest EV markets are the drivers.

Report Provides that major industry players, such as Shanghai Shanshan Technology, POSCO CHEMICAL, JSR Corporation, Resonac Holdings Corporation, and Tianqi Lithium Corporation, are very competitive, as they focus on the silicon-based innovation and vertical integration. The latest investment in silicon anode manufacturing, such as by Shanghai Shanshan and POSCO CHEMICAL, and further development of silicon anodes by Japanese companies. Market is characterized by such trends: Silicon-Based Anode Acceleration, Lithium Metal Revival, Beyond Automotive Expansion, Advanced Niobium and Tin-Based Materials, and AI-Driven Material Discovery. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Next Generation Anode Materials Market Dynamics:

Increasing demand for Electric Vehicles to boost the Next Generation Anode Materials Market growth

As the world moves towards a more sustainable future, the demand for electric vehicles (EVs) is increasing rapidly. Anode materials are a key component in the production of lithium-ion batteries used in EVs. As a result, the demand for Next Generation Anode Materials is expected to grow significantly over the forecast period. Advancements in technology are leading to the development of new anode materials that offer higher energy densities, faster-charging rates, and longer lifetimes. This is driving the adoption of next-generation anode materials in various applications, including consumer electronics, energy storage, and EVs. Governments around the world are implementing regulations to reduce greenhouse gas emissions and promote sustainable development. Leading to increased investment in the development and production of next-generation anode materials, which can help reduce carbon footprints and is expected to fuel the Next Generation Anode Materials Industry growth. Growing demand for renewable energy and the shift towards renewable energy sources such as wind and solar is driving the demand for energy storage solutions that can store excess energy generated during times of low demand. Anode materials are a critical component in the production of high-performance energy storage systems, which are essential for the efficient use of renewable energy. Due to increasing focus on sustainability consumers are becoming more aware of the impact of purchases on the environment.

Limited scalability and high manufacturing costs to hamper Next-Generation Anode Material Market growth

The manufacturing of next-generation anode materials is often complex and requires specialized equipment and processes. This results in higher manufacturing costs compared to traditional anode materials, which can make them less competitive in the market. Some next-generation anode materials are still in the early stages of development, and their scalability is uncertain. Scaling up production can be a challenge due to the need for specialized equipment and processes, which is expected to limit the commercial viability of Next Generation Anode Materials Market growth. The use of new materials in lithium-ion batteries introduces safety concerns, particularly if they have not been thoroughly tested or are not well understood, and result in resistance from end-users, regulators, and the general public. The supply chain for next-generation anode materials can be complex and require specialized knowledge and expertise, which makes it challenging to secure a reliable and cost-effective supply of materials, particularly if they are produced in limited quantities.

Cost and Safety Concerns to Create Challenges for Next-Generation Anode Material Market

Many of the new materials being developed are more expensive than traditional anode materials, such as graphite. This means that in order for these materials to become commercially viable, their cost must be reduced. This requires significant investment in research and development, as well as in the development of new manufacturing processes. The safety of next-generation anode materials is a major concern. Some of the new materials being developed have the potential to be more reactive than traditional anode materials, which could increase the risk of battery fires or explosions. It is important to thoroughly test and evaluate the safety of these materials before they are used in commercial products.

Next Generation Anode Materials Market Segment Analysis

Based on End-user, the market is segmented by Automotive, Consumer Electronics, Energy storage, Aerospace & Defence, Industrial user, and Transportation. The consumer electronics segment dominated the market in 2024 with the highest Next Generation Anode Materials Market share and is expected to dominate the market over the forecast period. Modern electronics use incredibly precise engineering to create powerful devices that fit in the palm of hand with the use of anode material. Next-generation battery materials and technologies are at the cross-section of the revolution in energy and the automotive industry. Lithium-ion batteries are an important component to achieve sustainable electrification of transportation systems.

Based on Application, the market is segmented by Fuel Cell, Capacitors, Lead-acid batteries, and lithium-ion batteries. Lead acid batteries and lithium-ion batteries segment is expected to dominate the market over the forecast period. The need for eco-friendly and portable energy sources for application in automobile and even aerospace industries has led to increase research and innovation in lithium-ion battery technology. Lead-acid batteries are in a state of charge/discharge that is stable, but some of major restraints are their bulky size and high weight, which makes them unfit for use in portable, light electric devices.

Next Generation Anode Materials Market Regional Insights

Asia Pacific region is a key market for next-generation anode materials due to its growing demand for high-performance batteries in applications such as electric vehicles, energy storage systems, and consumer electronics. The region held the largest Next Generation Anode Materials Market share in 2024 and dominated the market and is expected to dominate the market over the forecast period. Rapid industrialization in the Asia Pacific region is experiencing rapid industrialization, which is expected to fuel the demand for advanced batteries to power industrial equipment and machinery and is creating opportunities for the next generation anode materials that offer higher energy density, longer cycle life, and improved safety.

The Asia Pacific region is home to some of the world’s largest and fastest-growing electric vehicle markets, including China, Japan, and South Korea. This is driving demand for high-performance batteries and offer longer driving ranges and faster charging times. Next-generation anode materials such as silicon and lithium metal offer the potential for higher energy density, which could help to meet this demand and is expected to boost the Next Generation Anode Materials Market growth.

Next Generation Anode Materials Market Competitive Landscape

Top key players in Next Generation Anode Materials Market are Shanghai Shanshan Technology Co., Ltd., POSCO CHEMICAL, JSR Corporation, Resonac Holdings Corporation, Tianqi Lithium Corporation. Next-generation anode materials market is intensely competitive, with players vying for supremacy in materials beyond traditional graphite, particularly silicon-based, due to their higher energy density and faster charging capabilities. Chinese giants like Shanghai Shanshan Technology Co., Ltd. lead in artificial graphite and are rapidly advancing into next-gen solutions with new ultra-fast charging and long-cycle graphite. POSCO CHEMICAL distinguishes itself through strong vertical integration, leveraging its parent company's resources from raw materials to final anode production, including silicon anode development. Japanese firms JSR Corporation and Resonac Holdings Corporation focus on high-performance materials, emphasizing unique particle structures and advanced composites for enhanced battery performance. While primarily a lithium producer, Tianqi Lithium Corporation's strategic position in the battery supply chain hints at its influence in the evolving anode landscape. In the US, Sila Nanotechnologies Inc. and Amprius Technologies are at the forefront of silicon anode innovation, with Sila focusing on a "drop-in" solution for mass production and Amprius pushing the boundaries of energy density with its silicon nanowire and SiCore™ platforms for demanding applications like aviation. NanoGraf Corporation competes with its silicon-graphene anode materials, aiming for cost parity with synthetic graphite and demonstrating strong performance in cycle life and reduced swelling. The competition centers on achieving higher energy density, faster charging, improved cycle life, and scalability while addressing cost and safety challenges associated with new material chemistries.

Next Generation Anode Materials Market Key Trends:

• Silicon-Based Anode Acceleration

Silicon and silicon-carbon (Si-C) composites are dominating, offering vastly higher energy density for longer EV range and device life. Research focuses on mitigating silicon's volume expansion.

• Lithium Metal Revival

Once challenged by safety, lithium metal anodes are seeing breakthroughs, particularly with solid-state electrolytes, making them a high-energy density option for future high-performance batteries.

• Beyond Automotive Expansion

While EVs are a major driver, next-gen anode materials are increasingly sought for aerospace, defense, grid-scale energy storage, and advanced consumer electronics, demanding diverse performance attributes.

• Advanced Niobium and Tin-Based Materials

Beyond silicon, there's growing interest in alternative materials like Niobium-Tungsten Oxide (NTO) and tin-based compounds. These offer unique benefits such as improved stability, better safety, and specific performance profiles for niche applications, providing diversification beyond silicon.

• AI-Driven Material Discovery & Optimization

Artificial intelligence and advanced modeling are increasingly used to accelerate the discovery, design, and optimization of new anode material compositions and structures. This speeds up R&D cycles, reduces trial-and-error, and enables tailored solutions for specific battery requirements.

Next Generation Anode Materials Market Key Development:

| Year | Company Name | Recent Development |

| May 3 2024 | Shanghai Shanshan Technology Co., Ltd. (China) | Announced a $1.5 billion investment in a silicon-based anode project in Xichang, Sichuan, with an annual capacity of 300,000 tonnes. The first phase (120,000 tonnes) is expected to begin operations by December 2024. |

| Oct 23 2023 | Shanghai Shanshan Technology Co., Ltd. (China) | Continued to maintain a leading market share in artificial graphite and saw fast-charging anode products maintain a leading share in downstream applications due to excellent performance. Deepened cooperation with global leading battery companies. |

| Feb 22 2023 | POSCO CHEMICAL (now POSCO Future M) (South Korea) | Announced a 300 billion KRW investment to build a 5,000-ton capacity silicon anode materials plant in Pohang, enhancing production capabilities in silicon-based anode materials. |

| SEP 28 2024 | JSR Corporation (Japan) | While JSR's public announcements in 2024/2025 primarily focus on photoresists and other electronic materials (e.g., expanding global photoresist development and production functions), their historical technical reviews indicate ongoing R&D in battery materials, including binders for graphite anodes and advanced polymer electrolytes for LIBs. |

Next Generation Anode Materials Market Scope: Inquire before buying

| Next Generation Anode Materials Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 10.99 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 13.4 % | Market Size in 2032: | USD 30.05 Bn. |

| Segments Covered: | by Material | Silicon-based anode materials Graphene-based anode materials Carbon nanotubes-based anode materials Lithium titanate-based anode materials Metal oxides-based anode materials |

|

| by Application | Fuel Cell Capacitors Lead-acid batteries Lithium-Ion Batteries |

||

| by End User | Automotive Consumer Electronics Energy storage Aerospace & Defence Industrial user Transportation |

||

Next Generation Anode Materials Market by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Next Generation Anode Materials Market Key Players:

North America

1. Sila Nanotechnologies Inc. (USA)

2. Amprius Technologies (USA)

3. NanoGraf Corporation (USA)

4. OneD Battery Sciences (USA)

5. Albemarle Corporation (USA)

6. NextSource Materials Inc. (Canada)

7. Targray Industries Inc. (Canada)

8. Redwood Materials Inc. (USA)

Europe

1. Nexeon Ltd. (UK)

2. LeydenJar Technologies BV (Netherlands)

3. Talga Group (Australia)

4. BASF SE (Germany)

5. SGL Carbon SE (Germany)

Asia Pacific

1. Shanghai Shanshan Technology Co., Ltd. (China)

2. POSCO CHEMICAL (South Korea)

3. JSR Corporation (Japan)

4. Resonac Holdings Corporation (Japan)

5. Tianqi Lithium Corporation (China)

6. LG Chem Ltd. (South Korea)

South America

1. CBMM (Brazil)

2. Mitsubishi Chemical Group Corporation (Japan)

Middle East & Africa

1. TAQAT Development (Saudi Arabia)

Frequently Asked Questions:

1] What is the growth rate of the Global Next Generation Anode Materials Market?

Ans. The Global Next Generation Anode Materials Market is growing at a significant rate of 13.4% over the forecast period.

2] Which region is expected to dominate the Global Next Generation Anode Materials Market during the forecast period?

Ans. Asia Pacific region is expected to dominate the Next Generation Anode Materials Market over the forecast period.

3] What is the expected Global Next Generation Anode Materials Market size by 2032?

Ans. The market size of the Next Generation Anode Materials Market is expected to reach USD 30.05 Bn by 2032

4] Who are the top players in the Global Next Generation Anode Materials Industry?

Ans. The major key players in the Global Next Generation Anode Materials Market are Shanghai Shanshan Technology Co., Ltd., POSCO CHEMICAL, JSR Corporation, Resonac Holdings Corporation, Tianqi Lithium Corporation

5] Which factors are expected to drive the Global Next Generation Anode Materials Market growth by 2032?

Ans. Increasing demand for Electric Vehicles is expected to drive the Next Generation Anode Materials Market growth over the forecast period (2025-2032).