Industrial Automation Market was valued at USD 144.41 Billion in 2022, and it is expected to reach USD 255.63 Billion by 2029, exhibiting a CAGR of 8.5% during the forecast period (2023-2029) Industrial Automation is the control of machinery and processes used in various industrial sector by using autonomous technologies like robotics and computer software. MMR estimates that total value of implementing automation in the manufacturing industry across the world would reach $4.92 trillion by 2030. The manufacturing industry would be able to save about 749 billion working hours by automating 64.2% of manufacturing tasks and processes. The Industrial automation market is expected to witness growth 8.5% during the forecast period thanks to growing adoption of process automation technology across various industrial sector such as automotive, chemical, and energy utilities. The report has analyzed the impact of industrial automation on output, top line and supply chain as well the improvement in the quality of product. The experienced research analyst in the automation field has studied the return on investment in tangible as well as intangible benefits by industry and region. Industrial robotic market is too competitive with some serous entry barriers for new entrants. Entry barriers are different by segment and regions. The industrial automation industry is highly monopolistic since four major players Fanuc, Yaskawa, ABB and Kuka held 62% share in global industrial robotic market in 2022. The competitive landscape of the industry is covered by region with the benchmarking of services of market leaders, market followers and regional players.To know about the Research Methodology :- Request Free Sample Report

Research Methodology

Bottom up approach has been used to estimate the market size for global industrial robotic industry. Special focus has been given on each economies to arrive on market estimation for country, region and then global market size. Primary and secondary data collection methods have been used to collect the data. Secondary sources include paid sources, annual reports of key players, manufacturing associations of industrial robotics. Detailed secondary sources are provided in the report. Primary interviews carried out with stakeholders in industry that include manufacturers, end users, consultants. Combination of secondary and primary data collection made this report authentic. Micro level approach to understand the work culture by region and precedence of using robotics in manufacturing has helped repots to give local level key insights about future of robotics in manufacturing.Industrial Automation Market Dynamics:

Rising focus on real-time data analysis and predictive maintenance Rapid development in the manufacturing industry in Europe, the Middle East, and Africa is creating lucrative opportnutites for robotics industry..Industrial automation technologies enable firms to access plant floor data in real time, allowing them to consolidate corporate data and multi-plant operations. This feature is expected to accelerate the growth of the industrial automation market. For example, HMI allows manufacturers to carefully monitor manufacturing processes and act quickly to changing production demands, improving operational efficiency and decreasing unplanned downtime, and therefore providing greater visibility. Predictive maintenance and asset management systems provide user insight into the state of equipment by monitoring factors such as temperature, current, voltage, speed, vibration, and location. It also predicts when components are likely to break, allowing action to be taken, enhancing efficiency. As a result, unplanned downtime and production waste may be eliminated. Manufacturers in end-user industries such as oil and gas, food and beverage, automotive, and aerospace and defence are looking for solutions that aid real-time data analysis and proactive maintenance, as well as help them obtain better visibility of the manufacturing plant to improve plant efficiency. The growth factors in all these segmetns are anaysed and estimated in numbers to make user of this report understand the opportunities and threats in the industry. Increasing Intelligent Business Process Automation The increasing adoption of technologies such as industrial 4.0, AI-based smart robots, IoT, and others helps to reduce manufacturing costs while improving quality and dependability in the Automation. These criteria are critical for businesses to maintain a competitive edge in the marketplace. Mergers and collaborations among key companies are studied and given in order to understand the investment and conslodation in the industry. Increased need for safety compliance automation solutions A variety of processes used in industrial manufacturing can be dangerous to humans. Human mistakes or mechanical breakdowns can result in fatal incidents throughout the production process. As a result, it is critical for the manufacturing industry to implement safety measures in order to avoid such workplace fatalities. Safety compliance automation devices assist in the reduction of accident risks. For example, safety automation devices notify operators during crises and perform pre-programmed procedures to minimise the impact on human life. They discover faults in various machines and processes and perform diagnostics to find solutions as soon as possible. As a result, quick and reliable responses are required from these safety instrument systems (SIS). The International Electrotechnical Commission (IEC) and the International Standard Organization (ISO) regulate international safety standards for equipment in order to enhance worker safety while also ensuring product quality and technical compatibility of goods and services. These functional safety standards assist in obtaining the required degree of functional safety and performance in industries. As a result, the growing demand for safety compliance automation products and services presents an opportunity for the industrial automation market. High capital costs for installation and maintenance of industrial automation solutions The construction of brand-new automated manufacturing facilities necessitates the use of cutting-edge automation technologies such as SCADA, DCS, RTU, PLC, and HMI. Data collection via SCADA helps in eliminating calculation mistakes while enhancing product quality and manufacturing facility efficiency. The establishment of these production operations necessitates considerable financial expenditures in equipment, software, and training. For new entrants who are establishing their first factory, investing such a significant sum is tough. As a result, before deploying industrial automation systems and solutions, these businesses must conduct an in-depth examination of their return on investment. Furthermore, several companies are unable to replace their existing old systems due to the high prices of new and sophisticated systems, as well as the lack of connectivity with old systems. These legacy systems communicate via their own unique protocols, making it difficult to connect them to newer systems. Manufacturers have to pay significant additional costs to modify their existing systems.

Industrial Automation Market Segment Analysis:

By Components, the Industrial sensors segment is expected to hold largest share of industrial automation components market in the middle east & africa during forecast period. The increased adoption of Industry 4.0 and IIoT, as well as the growth of the wireless sensor market, are driving the growth of the industrial sensors segment. Industrial sensors are widely utilised in the manufacturing industry, primarily to improve connection across diverse activities. Manufacturers all across the world have begun to integrate sensors for gathering real-time data from multiple data points. Sensors as an important component of predictive maintenance solutions are expected to see rapid growth in demand in the coming years, as predictive maintenance is expected to offer lucrative opportunities through sensor data capture in the coming years. By Industry, the semiconductor industries are the only end-users, which maintained or increased demand for collaborations in 2022, mainly in the Asian market. Automotive and electronics accounted for nearly 62% of robotics revenues in 2022 but automotive continues to be weak and the sector will not surpass 2019 levels of demand for robotic solutions until 2022. Electronics segement is expected to recover slightly than automotive, having shown good signs of recovery in 2022, again especially in the Asian markets. The chemical, pharmaceutical and food and beverage industries saw stable product demand throughout the COVID 19 and there was a very limited reduction in their demand for robotic solutions. Analysis predicts that growth and technological advances in these sectors will put significant pressure on demand for robots during the forecast period.By Solutions, the PAM segment is expected to grow at good xx% CAGR in forecast period. Plant asset management (PAM) is software that uses the intelligence built in industrial assets to properly measure and give data on the condition of the equipment in a plant. Manufacturers are increasingly using PAM because it increases decision-making and turnaround time by detecting production errors and, as a result, avoiding system breakdowns through real-time data collecting and quality management procedures. PAM enables manufacturers to decrease downtime and resource waste by recognising potential problems before to production and suggesting corrective measures. PAM systems are widely used in the food and beverage and automotive sectors because of ongoing technological advances and the demand for a full data record of installed equipment. Furthermore, the growing demand for PAM technology can be attributed to the benefits of lower manufacturing costs and improved operations of high-performance production assets that they provide.

Industrial Automation Market Regional Insights

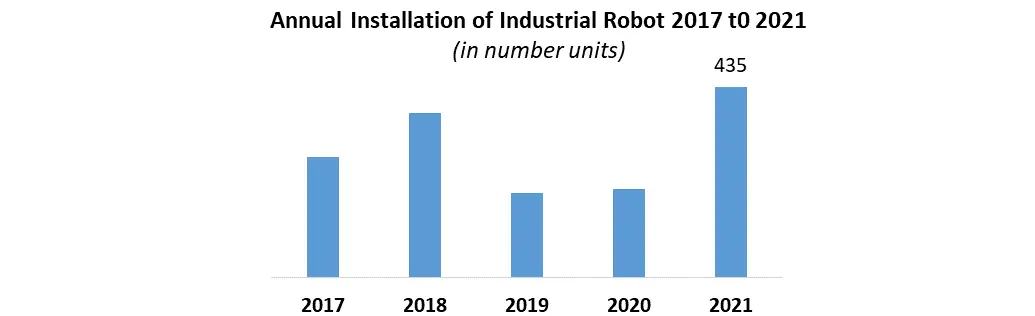

North America Industrial Automation Market is expected to grow at better spead than in 2021 to 2022 in terms of revenue during the forecast periodowing to the rising demand for innovative manufacturing robotic technologies across the industry. The robust production ability and trading potential of key companies is also a crucial factor accountable for the growth in this region. Recently, U.S. exported approximately USD 12.7 Billion worth of automation equipment. Moreover, the U.S. is third-largest global exporters after China and Germany. Globally, U.S. is a competitive top–tier supplier of the automation equipment market. In Europe Industrial Automation Market is likely to grow with the highest CAGR throughout the forecasted period. Germany belongs to the five major robot markets in the world (China, Japan, USA, Korea, Germany) and had a share of 36% of the total installations in Europe.The development in this region is due to the growing demand for IoT solutions for the innovative automation process in the automotive and manufacturing industry. Main companies in this region are concentrating on mergers and collaboration with other players to improve and launch innovative automated Automation Types. APAC has been a major contributor to the growth of the industrial control & factory automation market Owing to the construction sector, which is the key end user of industrial control & factory automation. The use of industrial automation and factory automation components and systems, such as SCADA, DCS, industrial sensors, and industrial robots is aided by the expanding population in this region's emerging countries as well as environmental awareness. Asia remains the world’s largest market for industrial robots. 76% of all newly deployed robots in 2022 were installed in Asia. Installations for the region´s largest adopter China grew strongly by 23% with 168,700 units shipped. Saudi Arabia's automotive sector is one of the largest in the Middle East, has remained reasonably steady, with a number of businesses reporting excellent results. Saudi Arabia is seeing substantial development in the manufacturing sector as a result of increasing deployment of various IoT-related software and services, which are propelling the Country to become a globally known technology-driven industry. Along with the industrial sector, the country's food processing industry is well established and poised to develop significantly in the future years.Industrial Automation Market Scope: Inquire before buying

Global Industrial Automation Market Report Coverage Details Base Year: 2022 Forecast Period: 2023-2029 Historical Data: 2018 to 2022 Market Size in 2022: US $ 144.41 Bn. Forecast Period 2023 to 2029 CAGR: 8.5% Market Size in 2029: US $ 255.63 Bn. Segments Covered: by Components 1. Industrial Robots 2. Machine Vision System 3. Process Analyzer 4. Field Instruments 5. Human Machine Interface (HMI) 6. Industrial PC 7. Industrial Sensors 8. Industrial 3D Printing 9. Vibration Monitoring by Solutions 1. Supervisory Control And Data Acquisition (SCADA) 2. Programmable Logic Controller (PLC) 3. Distributed Control System (DCS) 4. Manufacturing Execution System (MES) 5. Industrial Safety 6. Plant Asset Management (PAM) by Industry 1. Oil & Gas 2. Chemicals 3. Pharmaceuticals & Medical Devices 4. Food & Beverages 5. Energy & Power 6. Automotive 7. Machine Manufacturing 8. Water & Wastewater Treatment 9. Electronics & Semiconductors 10. Metals & Mining 11. Others Industrial Automation Market, by Region:

North America (United States, Canada and Mexico) Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe) Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC) Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A) South America (Brazil, Argentina Rest of South America)Industrial Automation Market, Key Players are:

1. FANUC (Japan) 2. Yaskawa Electric Corporation (Japan) 3. Toshiba Corporation (Japan) 4. Yokogawa Electric Corporation (Japan) 5. Fuji Electric Co., Ltd. (Japan) 6. Hitachi, Ltd. (Japan) 7. Omron Corporation (Japan) 8. Mitsubishi Electric Corporation (Japan) 9. Keyence Corporation (Japan) 10. Accurate Industrial Controls Pvt. Ltd. (India) 11. Honeywell International Inc (US) 12. Emerson Electric Co. (US) 13. General Electric Company (US) 14. Rockwell Automation, Inc (US) 15. Danaher Corporation (US) 16. NATIONAL INSTRUMENTS CORP (US) 17. Roper Technologies, Inc (US) 18. Voith GmbH (Germany) 19. Siemens AG (Germany) 20. Kuka AG (Germany) 21. Bosch Rexroth Corporation (Germany) 22. Phoenix Contact (Germany) 23. MARCO Limited (UK) 24. Schneider Electric SE (France) 25. Endress+Hauser (Switzerland) 26. ABB Ltd. (Switzerland) 27. Danfoss A/S (Denmark) 28. Tegan Innovations (Ireland) FAQs: 1. Which is the potential market for Industrial Automation in terms of the region? Ans. In the Asia Pacific region, the construction sector which is the key end user of industrial control & factory automation is expected to drive the market. 2. What is expected to drive the growth of the Industrial Automation market in the forecast period? Ans. Increasing focus on real-time data analysis and predictive maintenance are major factors driving the market growth during the forecast period. 3. What is the projected market size & growth rate of the Industrial Automation Market? Ans. Industrial Automation Market was valued at USD 144.41 Billion in 2022, and it is expected to reach USD 255.63 Billion by 2029, exhibiting a CAGR of 8.5 % during the forecast period. 4. What segments are covered in the Industrial Automation Market report? Ans. The segments covered are Components, Solutions, Industry, and region.

1. Industrial Automation Market Introduction 1.1. Study Assumption and Market Definition 1.2. Scope of the Study 1.3. Executive Summary 2. Industrial Automation Market: Dynamics 2.1. Industrial Automation Market Trends by Region 2.1.1. North America Industrial Automation Market Trends 2.1.2. Europe Industrial Automation Market Trends 2.1.3. Asia Pacific Industrial Automation Market Trends 2.1.4. Middle East and Africa Industrial Automation Market Trends 2.1.5. South America Industrial Automation Market Trends 2.2. Industrial Automation Market Dynamics by Region 2.2.1. North America 2.2.1.1. North America Industrial Automation Market Drivers 2.2.1.2. North America Industrial Automation Market Restraints 2.2.1.3. North America Industrial Automation Market Opportunities 2.2.1.4. North America Industrial Automation Market Challenges 2.2.2. Europe 2.2.2.1. Europe Industrial Automation Market Drivers 2.2.2.2. Europe Industrial Automation Market Restraints 2.2.2.3. Europe Industrial Automation Market Opportunities 2.2.2.4. Europe Industrial Automation Market Challenges 2.2.3. Asia Pacific 2.2.3.1. Asia Pacific Industrial Automation Market Drivers 2.2.3.2. Asia Pacific Industrial Automation Market Restraints 2.2.3.3. Asia Pacific Industrial Automation Market Opportunities 2.2.3.4. Asia Pacific Industrial Automation Market Challenges 2.2.4. Middle East and Africa 2.2.4.1. Middle East and Africa Industrial Automation Market Drivers 2.2.4.2. Middle East and Africa Industrial Automation Market Restraints 2.2.4.3. Middle East and Africa Industrial Automation Market Opportunities 2.2.4.4. Middle East and Africa Industrial Automation Market Challenges 2.2.5. South America 2.2.5.1. South America Industrial Automation Market Drivers 2.2.5.2. South America Industrial Automation Market Restraints 2.2.5.3. South America Industrial Automation Market Opportunities 2.2.5.4. South America Industrial Automation Market Challenges 2.3. PORTER’s Five Forces Analysis 2.4. PESTLE Analysis 2.5. Technology Roadmap 2.6. Regulatory Landscape by Region 2.6.1. North America 2.6.2. Europe 2.6.3. Asia Pacific 2.6.4. Middle East and Africa 2.6.5. South America 2.7. Key Opinion Leader Analysis For Industrial Automation Industry 2.8. Analysis of Government Schemes and Initiatives For Industrial Automation Industry 2.9. Industrial Automation Market Trade Analysis 2.10. The Global Pandemic Impact on Industrial Automation Market 3. Industrial Automation Market: Global Market Size and Forecast by Segmentation by Demand and Supply Side (by Value in USD Million) 2022-2029 3.1. Industrial Automation Market Size and Forecast, by Components (2022-2029) 3.1.1. Industrial Robots 3.1.2. Machine Vision System 3.1.3. Process Analyzer 3.1.4. Field Instruments 3.1.5. Human Machine Interface (HMI) 3.1.6. Industrial PC 3.1.7. Industrial Sensors 3.1.8. Industrial 3D Printing 3.1.9. Vibration Monitoring 3.2. Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 3.2.1. Supervisory Control And Data Acquisition (SCADA) 3.2.2. Programmable Logic Controller (PLC) 3.2.3. Distributed Control System (DCS) 3.2.4. Manufacturing Execution System (MES) 3.2.5. Industrial Safety 3.2.6. Plant Asset Management (PAM) 3.3. Industrial Automation Market Size and Forecast, by Industry (2022-2029) 3.3.1. Oil & Gas 3.3.2. Chemicals 3.3.3. Pharmaceuticals & Medical Devices 3.3.4. Food & Beverages 3.3.5. Energy & Power 3.3.6. Automotive 3.3.7. Machine Manufacturing 3.3.8. Water & Wastewater Treatment 3.3.9. Electronics & Semiconductors 3.4. Industrial Automation Market Size and Forecast, by Region (2022-2029) 3.4.1. North America 3.4.2. Europe 3.4.3. Asia Pacific 3.4.4. Middle East and Africa 3.4.5. South America 4. North America Industrial Automation Market Size and Forecast by Segmentation (by Value in USD Million) 2022-2029 4.1. North America Industrial Automation Market Size and Forecast, by Components (2022-2029) 4.1.1. Industrial Robots 4.1.2. Machine Vision System 4.1.3. Process Analyzer 4.1.4. Field Instruments 4.1.5. Human Machine Interface (HMI) 4.1.6. Industrial PC 4.1.7. Industrial Sensors 4.1.8. Industrial 3D Printing 4.1.9. Vibration Monitoring 4.2. North America Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 4.2.1. Supervisory Control And Data Acquisition (SCADA) 4.2.2. Programmable Logic Controller (PLC) 4.2.3. Distributed Control System (DCS) 4.2.4. Manufacturing Execution System (MES) 4.2.5. Industrial Safety 4.2.6. Plant Asset Management (PAM) 4.3. North America Industrial Automation Market Size and Forecast, by Industry (2022-2029) 4.3.1. Oil & Gas 4.3.2. Chemicals 4.3.3. Pharmaceuticals & Medical Devices 4.3.4. Food & Beverages 4.3.5. Energy & Power 4.3.6. Automotive 4.3.7. Machine Manufacturing 4.3.8. Water & Wastewater Treatment 4.3.9. Electronics & Semiconductors 4.4. North America Industrial Automation Market Size and Forecast, by Country (2022-2029) 4.4.1. United States 4.4.1.1. United States Industrial Automation Market Size and Forecast, by Components (2022-2029) 4.4.1.1.1. Industrial Robots 4.4.1.1.2. Machine Vision System 4.4.1.1.3. Process Analyzer 4.4.1.1.4. Field Instruments 4.4.1.1.5. Human Machine Interface (HMI) 4.4.1.1.6. Industrial PC 4.4.1.1.7. Industrial Sensors 4.4.1.1.8. Industrial 3D Printing 4.4.1.1.9. Vibration Monitoring 4.4.1.2. United States Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 4.4.1.2.1. Supervisory Control And Data Acquisition (SCADA) 4.4.1.2.2. Programmable Logic Controller (PLC) 4.4.1.2.3. Distributed Control System (DCS) 4.4.1.2.4. Manufacturing Execution System (MES) 4.4.1.2.5. Industrial Safety 4.4.1.2.6. Plant Asset Management (PAM) 4.4.1.3. United States Industrial Automation Market Size and Forecast, by Industry (2022-2029) 4.4.1.3.1. Oil & Gas 4.4.1.3.2. Chemicals 4.4.1.3.3. Pharmaceuticals & Medical Devices 4.4.1.3.4. Food & Beverages 4.4.1.3.5. Energy & Power 4.4.1.3.6. Automotive 4.4.1.3.7. Machine Manufacturing 4.4.1.3.8. Water & Wastewater Treatment 4.4.1.3.9. Electronics & Semiconductors 4.4.2. Canada 4.4.2.1. Canada Industrial Automation Market Size and Forecast, by Components (2022-2029) 4.4.2.1.1. Industrial Robots 4.4.2.1.2. Machine Vision System 4.4.2.1.3. Process Analyzer 4.4.2.1.4. Field Instruments 4.4.2.1.5. Human Machine Interface (HMI) 4.4.2.1.6. Industrial PC 4.4.2.1.7. Industrial Sensors 4.4.2.1.8. Industrial 3D Printing 4.4.2.1.9. Vibration Monitoring 4.4.2.2. Canada Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 4.4.2.2.1. Supervisory Control And Data Acquisition (SCADA) 4.4.2.2.2. Programmable Logic Controller (PLC) 4.4.2.2.3. Distributed Control System (DCS) 4.4.2.2.4. Manufacturing Execution System (MES) 4.4.2.2.5. Industrial Safety 4.4.2.2.6. Plant Asset Management (PAM) 4.4.2.3. Canada Industrial Automation Market Size and Forecast, by Industry (2022-2029) 4.4.2.3.1. Oil & Gas 4.4.2.3.2. Chemicals 4.4.2.3.3. Pharmaceuticals & Medical Devices 4.4.2.3.4. Food & Beverages 4.4.2.3.5. Energy & Power 4.4.2.3.6. Automotive 4.4.2.3.7. Machine Manufacturing 4.4.2.3.8. Water & Wastewater Treatment 4.4.2.3.9. Electronics & Semiconductors 4.4.3. Mexico 4.4.3.1. Mexico Industrial Automation Market Size and Forecast, by Components (2022-2029) 4.4.3.1.1. Industrial Robots 4.4.3.1.2. Machine Vision System 4.4.3.1.3. Process Analyzer 4.4.3.1.4. Field Instruments 4.4.3.1.5. Human Machine Interface (HMI) 4.4.3.1.6. Industrial PC 4.4.3.1.7. Industrial Sensors 4.4.3.1.8. Industrial 3D Printing 4.4.3.1.9. Vibration Monitoring 4.4.3.2. Mexico Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 4.4.3.2.1. Supervisory Control And Data Acquisition (SCADA) 4.4.3.2.2. Programmable Logic Controller (PLC) 4.4.3.2.3. Distributed Control System (DCS) 4.4.3.2.4. Manufacturing Execution System (MES) 4.4.3.2.5. Industrial Safety 4.4.3.2.6. Plant Asset Management (PAM) 4.4.3.3. Mexico Industrial Automation Market Size and Forecast, by Industry (2022-2029) 4.4.3.3.1. Oil & Gas 4.4.3.3.2. Chemicals 4.4.3.3.3. Pharmaceuticals & Medical Devices 4.4.3.3.4. Food & Beverages 4.4.3.3.5. Energy & Power 4.4.3.3.6. Automotive 4.4.3.3.7. Machine Manufacturing 4.4.3.3.8. Water & Wastewater Treatment 4.4.3.3.9. Electronics & Semiconductors 5. Europe Industrial Automation Market Size and Forecast by Segmentation (by Value in USD Million) 2022-2029 5.1. Europe Industrial Automation Market Size and Forecast, by Components (2022-2029) 5.2. Europe Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 5.3. Europe Industrial Automation Market Size and Forecast, by Industry (2022-2029) 5.4. Europe Industrial Automation Market Size and Forecast, by Country (2022-2029) 5.4.1. United Kingdom 5.4.1.1. United Kingdom Industrial Automation Market Size and Forecast, by Components (2022-2029) 5.4.1.2. United Kingdom Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 5.4.1.3. United Kingdom Industrial Automation Market Size and Forecast, by Industry(2022-2029) 5.4.2. France 5.4.2.1. France Industrial Automation Market Size and Forecast, by Components (2022-2029) 5.4.2.2. France Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 5.4.2.3. France Industrial Automation Market Size and Forecast, by Industry(2022-2029) 5.4.3. Germany 5.4.3.1. Germany Industrial Automation Market Size and Forecast, by Components (2022-2029) 5.4.3.2. Germany Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 5.4.3.3. Germany Industrial Automation Market Size and Forecast, by Industry (2022-2029) 5.4.4. Italy 5.4.4.1. Italy Industrial Automation Market Size and Forecast, by Components (2022-2029) 5.4.4.2. Italy Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 5.4.4.3. Italy Industrial Automation Market Size and Forecast, by Industry(2022-2029) 5.4.5. Spain 5.4.5.1. Spain Industrial Automation Market Size and Forecast, by Components (2022-2029) 5.4.5.2. Spain Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 5.4.5.3. Spain Industrial Automation Market Size and Forecast, by Industry (2022-2029) 5.4.6. Sweden 5.4.6.1. Sweden Industrial Automation Market Size and Forecast, by Components (2022-2029) 5.4.6.2. Sweden Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 5.4.6.3. Sweden Industrial Automation Market Size and Forecast, by Industry (2022-2029) 5.4.7. Austria 5.4.7.1. Austria Industrial Automation Market Size and Forecast, by Components (2022-2029) 5.4.7.2. Austria Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 5.4.7.3. Austria Industrial Automation Market Size and Forecast, by Industry (2022-2029) 5.4.8. Rest of Europe 5.4.8.1. Rest of Europe Industrial Automation Market Size and Forecast, by Components (2022-2029) 5.4.8.2. Rest of Europe Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 5.4.8.3. Rest of Europe Industrial Automation Market Size and Forecast, by Industry (2022-2029) 6. Asia Pacific Industrial Automation Market Size and Forecast by Segmentation (by Value in USD Million) 2022-2029 6.1. Asia Pacific Industrial Automation Market Size and Forecast, by Components (2022-2029) 6.2. Asia Pacific Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 6.3. Asia Pacific Industrial Automation Market Size and Forecast, by Industry (2022-2029) 6.4. Asia Pacific Industrial Automation Market Size and Forecast, by Country (2022-2029) 6.4.1. China 6.4.1.1. China Industrial Automation Market Size and Forecast, by Components (2022-2029) 6.4.1.2. China Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 6.4.1.3. China Industrial Automation Market Size and Forecast, by Industry (2022-2029) 6.4.2. S Korea 6.4.2.1. S Korea Industrial Automation Market Size and Forecast, by Components (2022-2029) 6.4.2.2. S Korea Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 6.4.2.3. S Korea Industrial Automation Market Size and Forecast, by Industry (2022-2029) 6.4.3. Japan 6.4.3.1. Japan Industrial Automation Market Size and Forecast, by Components (2022-2029) 6.4.3.2. Japan Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 6.4.3.3. Japan Industrial Automation Market Size and Forecast, by Industry (2022-2029) 6.4.4. India 6.4.4.1. India Industrial Automation Market Size and Forecast, by Components (2022-2029) 6.4.4.2. India Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 6.4.4.3. India Industrial Automation Market Size and Forecast, by Industry (2022-2029) 6.4.5. Australia 6.4.5.1. Australia Industrial Automation Market Size and Forecast, by Components (2022-2029) 6.4.5.2. Australia Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 6.4.5.3. Australia Industrial Automation Market Size and Forecast, by Industry (2022-2029) 6.4.6. Indonesia 6.4.6.1. Indonesia Industrial Automation Market Size and Forecast, by Components (2022-2029) 6.4.6.2. Indonesia Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 6.4.6.3. Indonesia Industrial Automation Market Size and Forecast, by Industry (2022-2029) 6.4.7. Malaysia 6.4.7.1. Malaysia Industrial Automation Market Size and Forecast, by Components (2022-2029) 6.4.7.2. Malaysia Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 6.4.7.3. Malaysia Industrial Automation Market Size and Forecast, by Industry (2022-2029) 6.4.8. Vietnam 6.4.8.1. Vietnam Industrial Automation Market Size and Forecast, by Components (2022-2029) 6.4.8.2. Vietnam Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 6.4.8.3. Vietnam Industrial Automation Market Size and Forecast, by Industry(2022-2029) 6.4.9. Taiwan 6.4.9.1. Taiwan Industrial Automation Market Size and Forecast, by Components (2022-2029) 6.4.9.2. Taiwan Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 6.4.9.3. Taiwan Industrial Automation Market Size and Forecast, by Industry (2022-2029) 6.4.10. Rest of Asia Pacific 6.4.10.1. Rest of Asia Pacific Industrial Automation Market Size and Forecast, by Components (2022-2029) 6.4.10.2. Rest of Asia Pacific Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 6.4.10.3. Rest of Asia Pacific Industrial Automation Market Size and Forecast, by Industry (2022-2029) 7. Middle East and Africa Industrial Automation Market Size and Forecast by Segmentation (by Value in USD Million) 2022-2029 7.1. Middle East and Africa Industrial Automation Market Size and Forecast, by Components (2022-2029) 7.2. Middle East and Africa Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 7.3. Middle East and Africa Industrial Automation Market Size and Forecast, by Industry (2022-2029) 7.4. Middle East and Africa Industrial Automation Market Size and Forecast, by Country (2022-2029) 7.4.1. South Africa 7.4.1.1. South Africa Industrial Automation Market Size and Forecast, by Components (2022-2029) 7.4.1.2. South Africa Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 7.4.1.3. South Africa Industrial Automation Market Size and Forecast, by Industry (2022-2029) 7.4.2. GCC 7.4.2.1. GCC Industrial Automation Market Size and Forecast, by Components (2022-2029) 7.4.2.2. GCC Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 7.4.2.3. GCC Industrial Automation Market Size and Forecast, by Industry (2022-2029) 7.4.3. Nigeria 7.4.3.1. Nigeria Industrial Automation Market Size and Forecast, by Components (2022-2029) 7.4.3.2. Nigeria Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 7.4.3.3. Nigeria Industrial Automation Market Size and Forecast, by Industry (2022-2029) 7.4.4. Rest of ME&A 7.4.4.1. Rest of ME&A Industrial Automation Market Size and Forecast, by Components (2022-2029) 7.4.4.2. Rest of ME&A Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 7.4.4.3. Rest of ME&A Industrial Automation Market Size and Forecast, by Industry (2022-2029) 8. South America Industrial Automation Market Size and Forecast by Segmentation (by Value in USD Million) 2022-2029 8.1. South America Industrial Automation Market Size and Forecast, by Components (2022-2029) 8.2. South America Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 8.3. South America Industrial Automation Market Size and Forecast, by Industry(2022-2029) 8.4. South America Industrial Automation Market Size and Forecast, by Country (2022-2029) 8.4.1. Brazil 8.4.1.1. Brazil Industrial Automation Market Size and Forecast, by Components (2022-2029) 8.4.1.2. Brazil Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 8.4.1.3. Brazil Industrial Automation Market Size and Forecast, by Industry (2022-2029) 8.4.2. Argentina 8.4.2.1. Argentina Industrial Automation Market Size and Forecast, by Components (2022-2029) 8.4.2.2. Argentina Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 8.4.2.3. Argentina Industrial Automation Market Size and Forecast, by Industry (2022-2029) 8.4.3. Rest Of South America 8.4.3.1. Rest Of South America Industrial Automation Market Size and Forecast, by Components (2022-2029) 8.4.3.2. Rest Of South America Industrial Automation Market Size and Forecast, by Solutions (2022-2029) 8.4.3.3. Rest Of South America Industrial Automation Market Size and Forecast, by Industry (2022-2029) 9. Global Industrial Automation Market: Competitive Landscape 9.1. MMR Competition Matrix 9.2. Competitive Landscape 9.3. Key Players Benchmarking 9.3.1. Company Name 9.3.2. Business Segment 9.3.3. End-user Segment 9.3.4. Revenue (2022) 9.3.5. Company Locations 9.4. Leading Industrial Automation Market Companies, by market capitalization 9.5. Market Structure 9.5.1. Market Leaders 9.5.2. Market Followers 9.5.3. Emerging Players 9.6. Mergers and Acquisitions Details 10. Company Profile: Key Players 10.1. FANUC (Japan) 10.1.1. Company Overview 10.1.2. Business Portfolio 10.1.3. Financial Overview 10.1.4. SWOT Analysis 10.1.5. Strategic Analysis 10.1.6. Scale of Operation (small, medium, and large) 10.1.7. Details on Partnership 10.1.8. Regulatory Accreditations and Certifications Received by Them 10.1.9. Awards Received by the Firm 10.1.10. Recent Developments 10.2. Yaskawa Electric Corporation (Japan) 10.3. Toshiba Corporation (Japan) 10.4. Yokogawa Electric Corporation (Japan) 10.5. Fuji Electric Co., Ltd. (Japan) 10.6. Hitachi, Ltd. (Japan) 10.7. Omron Corporation (Japan) 10.8. Mitsubishi Electric Corporation (Japan) 10.9. Keyence Corporation (Japan) 10.10. Accurate Industrial Controls Pvt. Ltd. (India) 10.11. Honeywell International Inc (US) 10.12. Emerson Electric Co. (US) 10.13. General Electric Company (US) 10.14. Rockwell Automation, Inc (US) 10.15. Danaher Corporation (US) 10.16. NATIONAL INSTRUMENTS CORP (US) 10.17. Roper Technologies, Inc (US) 10.18. Voith GmbH (Germany) 10.19. Siemens AG (Germany) 10.20. Kuka AG (Germany) 10.21. Bosch Rexroth Corporation (Germany) 10.22. Phoenix Contact (Germany) 10.23. MARCO Limited (UK) 10.24. Schneider Electric SE (France) 10.25. Endress+Hauser (Switzerland) 10.26. ABB Ltd. (Switzerland) 10.28. Danfoss A/S (Denmark) 10.29. Tegan Innovations (Ireland) 11. Key Findings 12. Industry Recommendations 13. Industrial Automation Market: Research Methodology 14. Terms and Glossary