Hydrogen Buses Market by Application (Public Transit Buses, Municipal Fleets, School Buses, Intercity Buses, Commercial Passenger Buses), Fuel Cell Type (Proton Exchange Membrane Fuel Cell, Phosphoric Acid Fuel Cell, Others), Range (Up to 300 km, 300-500 km, Above 500 km), and Region - Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

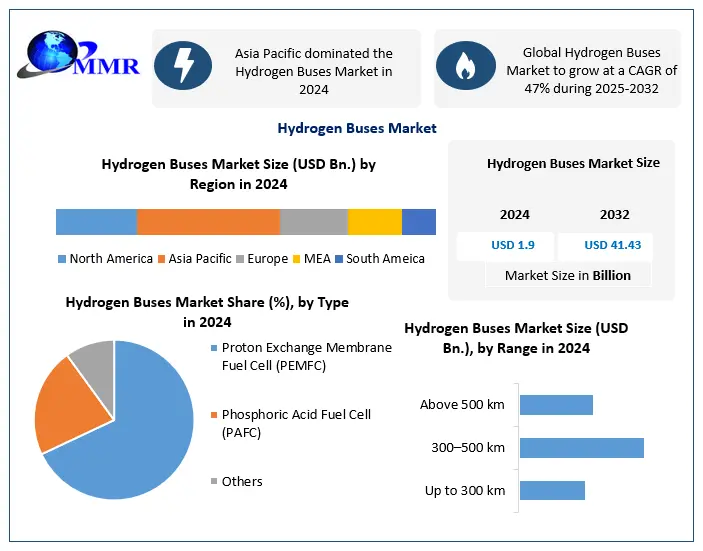

Hydrogen Buses Market was valued at USD 1.9 Bn. in 2024, and total global Hydrogen Buses Market revenue is expected to grow at a CAGR of 47% from 2025 to 2032, reaching nearly USD 41.43 Bn. Stringent government regulations on vehicle emissions.

Market Overview

Public transport buses that run on hydrogen fuel cells rather than conventional fossil fuels are known as hydrogen buses. Due to their capacity to provide a viable, clean, and effective public transit option, they are gaining popularity. These buses run on a fuel cell stack, which converts hydrogen and oxygen into energy to run the electric motor. Since water vapour is the sole result of this process, hydrogen buses are an alternative for zero-emission vehicles.

The Hydrogen Buses Market is growing rapidly, driven by a rising global demand for clean and sustainable transportation solutions. Governments worldwide are implementing initiatives and incentives aimed at reducing greenhouse gas emissions and improving air quality, contributing to the market's growth. Hydrogen buses emit zero pollutants or greenhouse gases during operation, making them an appealing option for transit agencies and governments looking to reduce their carbon footprint. Notably, countries such as Germany, the United Kingdom, Japan, South Korea, and China are investing in hydrogen bus fleets, with the Asia-Pacific region being a significant market for hydrogen buses due to significant investments in hydrogen fuel cell technology and infrastructure. According to the report, the global hydrogen bus market is projected to grow from $608.29 million in 2023 to $1750.53 million by 2030, with a compound annual growth rate of 16.3% during the forecast period. The market's growth is attributed to several factors, including government support, rising demand for clean energy solutions, and advancements in fuel cell technology. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Research Methodology

Primary and secondary data sources was used to gather information for the study of the Hydrogen Buses Market. The study has considered the potential market influencing aspects and these were assessed to produce results. The market prediction has taken into account the effects of numerous economic factors including inflation, regulatory changes, and policy changes, as well as the market size for top-level markets and sub-segments.

The bottom-up methodology and various data triangulation approaches was considered to assess the market size and forecast. The weights allocated to each segment based on their utilisation rate and average sale price will be used to determine the percentage splits, market shares, and segment breakdowns. Based on the proportion of the provided market size that is adopted or used in each area or nation, the total market and its sub-segments was analysed by country.

The major competitors in the market were also analysed based on metrics such as market revenue, pricing, services supplied, developments, mergers and acquisitions, and joint ventures. Market engineering and calculations for market statistics, market size estimations, market projections, market breakdown, and data triangulation were considered to gather information and verify and confirm the key figures. In order to provide decision-makers with a clear future vision of the industry, external and internal elements that are predicted to have an impact on the firm positively or adversely will be evaluated. By examining market segments and estimating market size, the research can also help in understanding the dynamic structure of the industry. The study will be an investor's guide thanks to the clear depiction of competition analysis of important companies by pricing, financial condition, development plans, and regional presence in the market.

Market Dynamics

Hydrogen Buses Market Major Drivers

The increasing demand for clean energy solutions and the need to reduce greenhouse gas emissions are the major drivers for the growth of the hydrogen bus market. The rising concern for the environment and the need to curb air pollution in urban areas have led governments to adopt eco-friendly transport solutions. Hydrogen buses emit only water vapor, making them a perfect alternative to diesel and petrol buses. Moreover, hydrogen fuel cell technology has witnessed significant advancements in recent years, making hydrogen buses more efficient and reliable. Governments worldwide are investing in hydrogen infrastructure to support the adoption of hydrogen buses, which is expected to drive the market growth in the coming years.

Hydrogen Buses Market Opportunities

The growth in the tourism industry and the need to provide sustainable public transport solutions are expected to drive the demand for hydrogen buses. Developing economies are expected to emerge as significant markets for hydrogen buses, owing to the rising concern for air pollution and the adoption of eco-friendly transport solutions. Moreover, the increasing demand for zero-emission buses in the public transport sector is expected to drive the demand for hydrogen buses. The development of advanced fuel cell technologies and the increasing focus on hydrogen fuel infrastructure development are also expected to offer lucrative opportunities for players in the hydrogen bus market. Overall, the hydrogen bus market is expected to witness significant growth in the coming years, driven by the growing need for clean energy solutions and sustainable public transport systems.

Hydrogen Buses Market Major Restraints

Major restraints in the hydrogen buses market include the high cost of hydrogen fuel cell technology compared to conventional diesel or electric buses. The cost of producing and storing hydrogen fuel is also high, which makes it challenging for mass adoption. Additionally, the lack of hydrogen refuelling infrastructure in many countries limits the reach of hydrogen buses, making it difficult to expand their use beyond a few select regions. Furthermore, the maintenance and repair of fuel cell systems are more complicated than those of conventional buses, requiring specialized knowledge and tools. The lack of trained personnel and infrastructure for fuel cell maintenance is also a challenge, hindering the growth of the hydrogen bus market.

Hydrogen Buses Market Challenges

Challenges in the hydrogen buses market include the limited range of hydrogen fuel cell buses compared to diesel or electric buses. This range limitation is due to the relatively low energy density of hydrogen fuel, which necessitates larger fuel tanks, heavier buses, and limited passenger capacity. Another challenge is the need for safety measures to be implemented for hydrogen fuel storage and handling, which requires specialized knowledge and skills. The safety risks associated with hydrogen fuel, such as the potential for fires or explosions, also need to be addressed. Furthermore, the production of hydrogen fuel is still largely dependent on non-renewable energy sources, which contradicts the environmental benefits of using hydrogen fuel cell buses. Finally, the lack of consumer awareness and government support for hydrogen buses is a significant challenge, as it limits the demand for hydrogen fuel cell buses and prevents the development of necessary infrastructure.

Hydrogen Buses Market Market trends

The hydrogen bus market is expected to experience significant growth in the coming years, driven by various market trends. The report highlights the increasing demand for zero-emission vehicles as a major trend, owing to concerns about air pollution and climate change. It also emphasizes the government support and initiatives for the adoption of hydrogen fuel cell technology in public transportation and the development of hydrogen infrastructure as significant trends driving the growth of the market.

The report further notes the increasing partnerships and collaborations between hydrogen fuel cell manufacturers, bus manufacturers, and other stakeholders in the industry as another significant trend. Such partnerships are enabling the development of new and innovative products, driving technological advancements, and reducing costs, which is increasing the overall competitiveness of the market. Additionally, the report highlights the Asia-Pacific region as the fastest-growing market for hydrogen buses, with increasing population, urbanization, and growing concerns about air pollution driving the demand for sustainable public transportation.

In conclusion, the report by Maximize Market Research provides an overview of the market trends driving the growth and development of the hydrogen bus market, including the demand for zero-emission vehicles, government support and initiatives, the development of hydrogen infrastructure, partnerships and collaborations, and growth potential in the Asia-Pacific region. The report suggests that manufacturers and stakeholders in the industry need to capitalize on these trends to ensure the continued growth and development of the hydrogen bus market.

Hydrogen Buses Market Segment Analysis

Based on Range, the 300–500 km range segment dominated the hydrogen buses market in 2024 due to its optimal balance between fuel efficiency and route coverage. This range supports full-day city operations without the need for frequent refueling, making it highly suitable for urban transportation needs. Additionally, hydrogen refueling infrastructure is still limited in many regions, so this mid-range capability ensures flexibility without straining existing logistics. Most manufacturers such as Toyota and Hyundai are focusing their models within this range due to high demand from municipalities and public fleets. The 300–500 km range is becoming a standardized sweet spot for performance, cost, and practicality.

Based on Application, Public Transit Buses were the leading application segment in 2024 as city governments’ globally prioritized clean energy for reducing carbon emissions. These buses operate on fixed routes and at high frequency, making them ideal candidates for hydrogen fuel adoption due to their quick refueling time compared to battery-electric alternatives. Many pilot and full-scale deployments in regions like Europe, China, and California are focused on public transit networks. Additionally, funding support and green mobility mandates have accelerated hydrogen bus adoption in this segment. With increasing environmental regulations, public transit agencies continue to be the first movers in adopting zero-emission hydrogen buses.

Regional insights

Hydrogen Buses Market Asia-Pacific

The Asia-Pacific region is expected to be the fastest-growing market for hydrogen buses, with the increasing population, urbanization, and growing concerns about air pollution driving the demand for sustainable public transportation. Several countries in the region, including China, Japan, and South Korea, are investing heavily in hydrogen infrastructure and incentivizing the adoption of hydrogen buses. The partnerships and collaborations between hydrogen fuel cell manufacturers, bus manufacturers, and other stakeholders in the industry are also driving the growth of the market in the region.

Hydrogen Buses Market Europe

Europe is a significant market for hydrogen buses, with several countries introducing policies and initiatives to promote the adoption of zero-emission vehicles. The European Union has set ambitious targets for reducing carbon emissions, which is driving the demand for clean and sustainable public transportation. Several countries, including Germany, France, and the United Kingdom, have announced plans to phase out diesel buses and replace them with zero-emission alternatives, including hydrogen buses. The development of hydrogen infrastructure, including fuelling stations, is also driving the growth of the market in the region.

North America

North America is another significant market for hydrogen buses, with several cities in the United States and Canada deploying hydrogen buses for public transportation. The government of California has set ambitious targets for reducing carbon emissions, which is driving the adoption of zero-emission vehicles, including hydrogen buses. The development of hydrogen infrastructure is also gaining momentum in the region, with several fueling stations being built to support the deployment of hydrogen buses. The partnerships and collaborations between hydrogen fuel cell manufacturers, bus manufacturers, and other stakeholders in the industry are also driving the growth of the market in the region.

LAMEA

The LAMEA region is an emerging market for hydrogen buses, with several countries in the region announcing plans to introduce hydrogen buses for public transportation. The governments of several countries, including Brazil, Saudi Arabia, and South Africa, are investing in hydrogen infrastructure to support the deployment of hydrogen buses. The region's abundant renewable energy resources, including solar and wind power, provide significant opportunities for the production of green hydrogen, which can be used to power hydrogen buses. The partnerships and collaborations between hydrogen fuel cell manufacturers, bus manufacturers, and other stakeholders in the industry are also driving the growth of the market in the region.

Hydrogen Buses Market Competitive landscape

According to a recent report the hydrogen bus market is highly competitive, with major players such as Toyota Motor Corporation, Hyundai Motor Company, Daimler AG, MAN Truck & Bus AG, and Ballard Power Systems Inc. dominating the industry. These companies are investing heavily in research and development activities to develop innovative hydrogen fuel cell technology for buses, and partnerships and collaborations between fuel cell and bus manufacturers are further driving the competitiveness of the market.

The report highlights how companies are expanding their market presence by securing contracts for supplying hydrogen buses to various regions, such as Daimler Buses securing a contract to deliver 15 hydrogen buses to Transports Metropolitans de Barcelona (TMB) in Spain. Additionally, the development of hydrogen infrastructure, including fueling stations, is a crucial factor in the competitiveness of the market. Companies are collaborating with governments and other stakeholders to develop hydrogen infrastructure to support the deployment of hydrogen buses. For instance, Ballard Power Systems Inc. has partnered with Siemens AG and other companies to develop a fuel cell module for Siemens' Mireo Plus H hydrogen-powered train.

Overall, the report emphasizes that the hydrogen bus market is expected to remain highly competitive as major players continue to invest in research and development, partnerships and collaborations, and market expansion strategies. The development of hydrogen infrastructure is also a key factor in shaping the industry's competitive landscape, and companies are actively collaborating with governments and other stakeholders to develop this infrastructure.

Hydrogen Buses Market Scope: Inquire before buying

| Hydrogen Buses Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 1.9 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 47% | Market Size in 2032: | USD 41.43 Bn. |

| Segments Covered: | by Type | Proton Exchange Membrane Fuel Cell (PEMFC) Phosphoric Acid Fuel Cell (PAFC) Others |

|

| by Range | Up to 300 km 300–500 km Above 500 km |

||

| by Application | Public Transit Buses Municipal Fleets School Buses Intercity Buses Commercial Passenger Buses |

||

Hydrogen Buses Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Hydrogen Buses Market Key Players

1.Alstom(France)

2.Ballard Power Systems(Canada)

3.Bluebus(Brazil)

4.CaetanoBus(Portugal)

5.Daimler AG(Netherlands)

6.ElringKlinger AG(Germany)

7.FlixBus(Germany)

8.Hino Motors(Japan)

9. Hyundai Motor Company(South Korea)

10.Iveco(Italy)

11.MAN Truck & Bus (France)

12. McPhy Energy S.A.(Canada)

13.New Flyer Industries Inc.(USA)

14.Nikola Motor Company(USA)

15.Solaris Bus & Coach(Poland)

16.Stellantis(Netherlands)

17.Tata Motors(India)

18. The Lion Electric Co.(Canada)

19. Toyota Motor Corporation(Japan)

20.Van Hool N.V.(Belgium)

21. VDL Bus & Coach(Netherlands)

22.Volvo Group(Sweden)

23. Wrightbus(United Kingdom)

24.Yutong Bus Co., Ltd.(China)

25.Zenith Motors.(United States of America)

FAQS:

1. What are the growth drivers for the Hydrogen Buses Market?

Ans. The growth drivers for the Hydrogen Buses Market include increasing government support and investments in zero-emission transportation solutions, rising environmental concerns, and technological advancements in fuel cell technology.

2. What is the major restraint for the Hydrogen Buses Market growth?

Ans. The major restraint for the market growth is the high initial cost of hydrogen buses compared to conventional diesel or gasoline-powered buses.

3. Which region is expected to lead the global Hydrogen Buses Market during the forecast period?

Ans. Asia Pacific is expected to lead the global Hydrogen Buses Market during the forecast period, due to increasing government initiatives and investments in hydrogen fuel cell technology, particularly in countries such as China, Japan, and South Korea.

4. What is the projected market size & growth rate of the Hydrogen Buses Market?

Ans. The Hydrogen Buses Market was valued at USD 1.9 billion in 2024, and total global Hydrogen Buses Market revenue is expected to grow at a CAGR of 47% from 2025 to 2032, reaching nearly USD 41.43 billion. Stringent government regulations on vehicle emissions.

5. What segments are covered in the Hydrogen Buses Market report?

Ans. The segments covered in the Hydrogen Buses Market report are Type, Range, Applications, and Region.