Heavy Construction Vehicles Market Market Market– Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

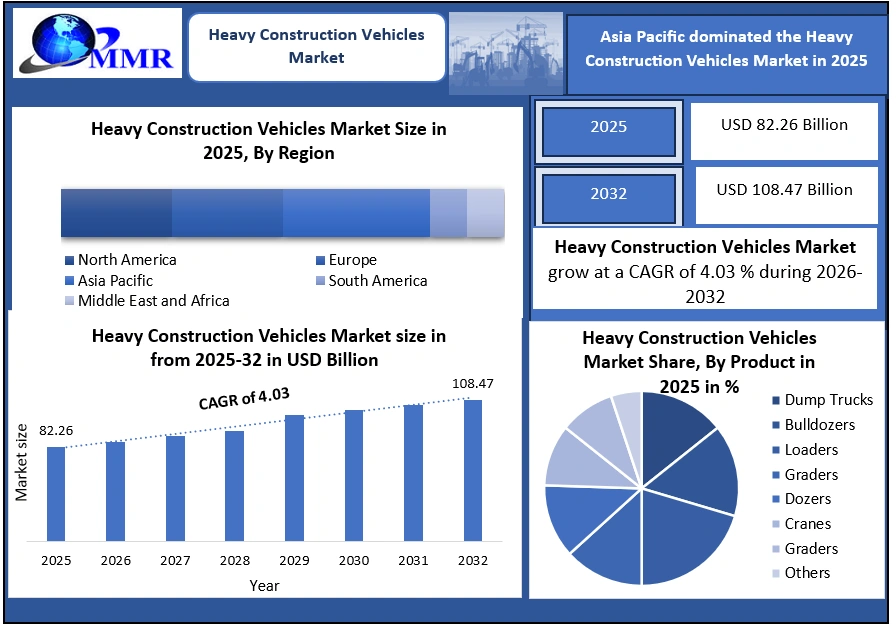

The Heavy Construction Vehicles Market size was valued at USD 82.26 Billion in 2025 and the total Heavy Construction Vehicles revenue is expected to grow at a CAGR of 4.03% from 2026 to 2032, reaching nearly USD 108.47 Billion by 2032.

Heavy Construction Vehicles Market Overview

Heavy construction vehicles form the operational backbone of global infrastructure development, enabling large-scale earthmoving, material handling, mining, and road construction activities. In 2015, global demand for heavy construction vehicles was largely concentrated in developed economies and commodity-driven markets. By 2024, demand shifted decisively toward Asia-Pacific, driven by national highway programs, smart city development, renewable energy infrastructure, and mining investments.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Globally, over 1.95 billion heavy construction vehicles were sold in 2025, with Asia-Pacific accounted for nearly xx % of total unit demand, followed by North America (nearly 25%) and Europe (xx%). China remains the largest manufacturing and consumption hub, while India has emerged as the fastest-growing large market due to aggressive public infrastructure spending.

Market Key Highlights:

• Global heavy construction vehicle demand grew at a CAGR of nearly xx% between 2020 and 2024

• Asia-Pacific accounted for xx% of the global market value in 2025

• Construction applications represented 62.9% of total vehicle utilisation, in 2025.

• Diesel-powered vehicles dominated with xx% share in 2025, though electric variants are growing at 14%+ CAGR

• In 2025, Autonomous and telematics-enabled equipment reduced operating costs by 15–20% for fleet owners.

Heavy Construction Vehicles Market Dynamics

Penetration, Adoption, and Utilization Trends and Drivers

Between 2020 and 2024, the penetration rate of heavy construction vehicles increased steadily in emerging economies due to infrastructure expansion and contractor fleet formalisation. Adoption of rental and leasing models increased sharply, especially among mid-sized contractors. Rental penetration rose from 32% in 2020 to nearly 44% in 2025, improving equipment utilisation and lowering capex barriers.

Global infrastructure spending is a key driver propelling the heavy construction vehicles market. For instance, the U.S. government allocated over USD 350 billion in 2024 to enhance highways, transportation, and energy infrastructure, directly stimulating demand for advanced construction equipment. Similarly, the UK and other developed economies are channelling substantial investments toward energy and transportation projects, highlighting a clear governmental push that fosters market growth.

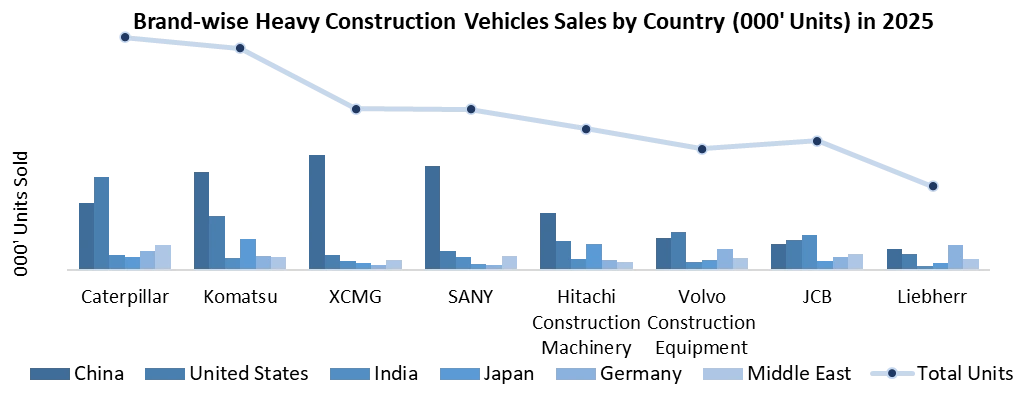

The graph displays the brand-wise heavy construction vehicles sales by country in 2025 (measured in thousands of units). It highlights the sales distribution of leading brands like Caterpillar, Komatsu, XCMG, and others across various regions, with China showing the highest sales volume.

The graph displays the brand-wise heavy construction vehicles sales by country in 2025 (measured in thousands of units). It highlights the sales distribution of leading brands like Caterpillar, Komatsu, XCMG, and others across various regions, with China showing the highest sales volume.

Market Challenges and Opportunities

• Challenges: Sales decline in certain months due to project delays, funding issues, and urban-rural demand divides impact short-term growth.

• Opportunities: Growing focus on semi-urban and tier-2 cities, rising government infrastructure projects post-elections, and competitive pricing with stable inventory create favorable conditions for sales growth.

• Unorganized Sector: Small and mid-sized contractors contribute to demand fluctuations, indicating potential market formalization and digital adoption opportunities.

Heavy Construction Vehicles Market: Segment Analysis

The Construction & Infrastructure sector dominated the Heavy Construction Vehicles market with a commanding xx% global market share in 2025, followed by significant demand from Mining and Material Handling industries, driving growth.

Loaders dominated the global Heavy Construction Vehicles Market, accounting for a market value of USD xx billion in 2025, supported by their high utilization rate in material handling, mining operations, and urban infrastructure projects. The segment is projected to grow at a CAGR of xx% (2026–2032), with Asia-Pacific holding nearly xxx % market share, driven by China, India, and Southeast Asia.

Heavy Construction Vehicles Market: Regional Analysis

• Asia-Pacific: Dominated the largest market share in 2025 and fastest-growing market with 520,000 units sold in 2025; China (xx%), India (22%), Japan, Indonesia, and Vietnam are key contributors

• North America: Mature yet technology-driven market; xx units sold, with high rental penetration (48%)

• Europe: Strong regulatory-driven demand; electric and hybrid penetration already >9%

• Middle East & Africa: Infrastructure-led growth; adoption rate growing at >7% CAGR (2025-2032)

• South America: Mining and energy projects driving demand in Brazil, Chile, and Peru

Competitive Landscape Analysis

The market is highly competitive with several key global and regional players shaping the industry landscape:

| Company | 5-Year Growth Rate (%) | 2025 Market Share | Key Strategic Moves & Market Impact |

| JCB India Ltd | -xx.x % | AA | Market leader; expanding telematics and aftersales services. |

| Action Construction Equipment (ACE) | -0.5% | xx% | Scaling production; innovation in crane and loader segments. |

| Ajax Engineering Ltd | +0.43% | 7.22% | Niche player focusing on concrete and metro projects. |

| Escorts Kubota Ltd | -xx.x % | xx% | Focused on backhoe loaders; poised for demand recovery. |

| Caterpillar India Pvt Ltd | -0.31% | xx% | Leader in autonomous haul trucks; expanding digital solutions. |

Between 2020 and 2024, leading players achieved 4–7% average annual revenue growth, driven by aftermarket services, digital platforms, and geographic expansion. Organised OEMs are steadily gaining share from the unorganized and regional manufacturers due to financing access, emission compliance, and technology differentiation.

Recent Developments by Major Players

| Development Area | Key Highlights | Impact / Data |

| Electrification & Sustainability | Komatsu electric excavators & Zoomlion hybrid trucks | Up to 30% energy savings, emissions cut; Govt incentives boost 20% YoY adoption |

| Automation & AI | Autonomous haul trucks (Caterpillar), CASE telematics | Productivity ↑ by 15-20%, safety incidents ↓ by 10% |

| Product Innovation | Caterpillar 330 UHD demolition excavator launch | Precision & safety improved; 10% faster operation |

Strategic Impact and Future Opportunities

OEM strategies increasingly focus on:

• Electrification and automation to meet regulatory and ESG mandates

• Localized manufacturing to reduce cost and improve delivery timelines

• Digital fleet management platforms for contractors and rental operators

The organized sector controls 72% of global sales, while unorganized and regional manufacturers remain influential in price-sensitive markets such as South Asia, Africa, and parts of South America.

Heavy Construction Vehicles Market Scope: Inquire before buying

| Global Heavy Construction Vehicles Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 82.26 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 4.5% | Market Size in 2032: | USD 108.47 Bn. |

| Segments Covered: | by Type | Dump Trucks Bulldozers Loaders Graders Dozers Cranes Graders Others |

|

| byPower source | Diesel Electric Hybrid |

||

| by Application | Excavation & Mining Lifting & Material Handling Earthmoving Tunneling Transportation Others |

||

| by Sales Channel | OEM Direct Sales Dealerships & Distributors Aftermarket Sales |

||

| by Industry | Oil & Gas Construction & Infrastructure Manufacturing Mining Agriculture Transportation & Logistic Others |

||

Heavy Construction Vehicles Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Heavy Construction Vehicles Key Players

1. Caterpillar Inc.

2. Komatsu Ltd.

3. XCMG Group

4. SANY Group

5. Deere & Company (John Deere)

6. Volvo Construction Equipment

7. Hitachi Construction Machinery

8. Liebherr Group

9. Sandvik AB

10. JCB

11. Doosan Bobcat / Develon

12. CNH Industrial (CASE Construction)

13. Kobelco Construction Machinery

14. Hyundai Construction Equipment

15. Zoomlion Heavy Industry

16. Astec Industries, Inc.

17. Bauer Group

18. Bell Equipment Ltd.

19. Hidromek Co. Ltd.

20. Tata Hitachi Construction Machinery

21. BEML Ltd.

22. Action Construction Equipment (ACE)

23. LiuGong

24. Schwing Stetter

25. Putzmeister

26. Coninfra Machinery Pvt. Ltd.

27. Bobcat Company

28. CNH Industrial (New Holland)

29. Taiyuan Heavy Industry

30. Atlas Copco

31. Others

FAQ

1. What is the size of the global heavy construction vehicles market in 2025?

Ans: The global heavy construction vehicles market was valued at USD 82.26 billion in 2025 and is projected to grow steadily with a CAGR of 4.03% through 2032.

2. Which region holds the largest share in the heavy construction vehicles market?

Ans: Asia-Pacific is the largest market region, led by China and India, driven by rapid infrastructure development and rising demand.

3. What are the main types of heavy construction vehicles?

Ans: The primary types include loaders, dump trucks, bulldozers, graders, and cranes, with loaders having the highest market utilization.

4. What technological trends are shaping the heavy construction vehicles market?

Ans: Key trends include automation, autonomous vehicles, telematics, and electrification, enhancing efficiency and sustainability.

5. Who are the leading companies in the heavy construction vehicles market?

Ans: Top players are Caterpillar Inc., Komatsu Ltd., JCB, Volvo Construction Equipment, and Hitachi Construction Machinery, focusing on innovation and market growth.