Global Tin Market Product Type, Application, End Use Industry, Region – Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

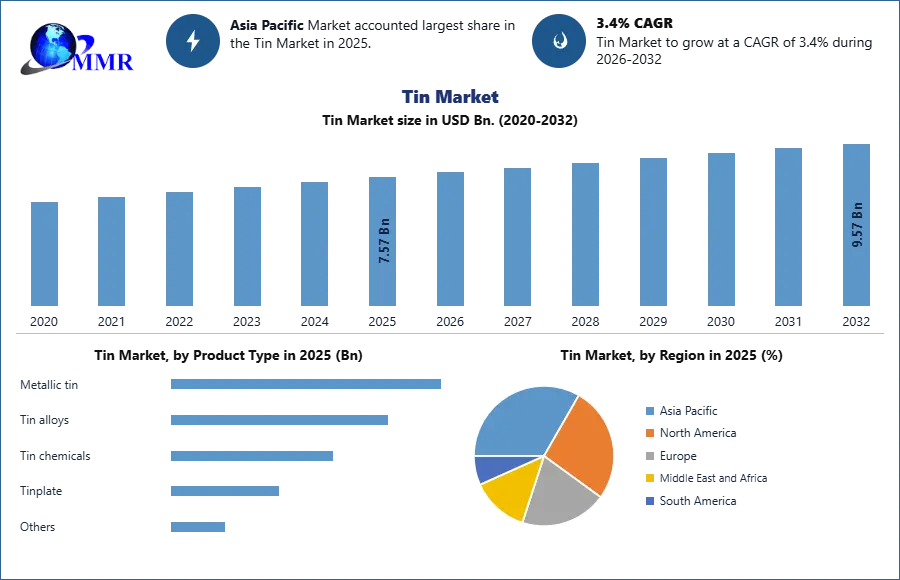

The Tin Market size was valued at USD 7.57 billion 2025 and the total Tin revenue is expected to grow at a CAGR of 3.4% from 2026 to 2032, reaching nearly USD 9.57 billion in 2032

Tin Market Overview:

The tin market has a phase of strategic significance, largely due to increasing vulnerabilities across the global supply chain and the growing importance of tin in clean energy technologies. Over the past three years, 71% of all supply disruptions have stemmed from Myanmar and Indonesia—two countries that collectively contribute nearly 35–40% of global tin ore production. These frequent interruptions have placed substantial pressure on the availability of raw materials and have caused London Metal Exchange (LME) tin prices to surge beyond USD 36,000–38,000 per ton. This volatility has intensified concerns about long-term supply security, prompting major economies, including the United States, the United Kingdom, and Australia. Such designations are accelerating investment into recycling infrastructure, advanced traceability systems, and diversified sourcing strategies aimed at reducing dependence on geopolitically sensitive regions.

The demand environment for tin continues to strengthen due to its indispensable role in the global shift toward electrification and renewable energy technologies. Beyond energy systems, tin chemicals used in PVC stabilisation, catalytic processes, speciality coatings, and polymer enhancements are expanding at a steady annual rate reflecting broad-based growth across the construction, packaging, and chemical processing sectors.

To know about the Research Methodology :- Request Free Sample Report

Tin Market Dynamics

Technological Advancements, Industrial Expansion, and Material Innovation Drive the Tin Market Growth

The Tin Market is experiencing robust growth driven by sustainability imperatives, technological advancements, and expanding industrial applications across electronics, energy storage, chemicals, and manufacturing. Tin’s dominant role in the global soldering industry—representing over 50% of total tin consumption continues to anchor demand as electronics production accelerates worldwide. The expansion of consumer electronics, semiconductor miniaturization, and advanced PCB manufacturing are reinforcing tin’s position as an indispensable material, strengthening key demand clusters such as lead-free solder, high-purity tin alloys, and industrial-grade tin chemicals. As digitalization deepens across sectors, the Tin Market remains closely tied to global electronics manufacturing trends.

The Tin Market is supported by rapid growth in automotive and transportation technologies, particularly the global shift toward electric vehicles (EVs). Tin-based alloys are increasingly used in EV battery packs, power electronics, thermal management systems, and precision soldering applications due to their conductivity, strength, and compatibility with high-temperature operations. As global EV production is projected to exceed 40 million units annually by 2032, tin usage in EV components is expected to rise significantly, positioning the Tin Market for sustained long-term expansion.

Industrial expansion in packaging and construction also contributes to steady growth within the Tin Market. Tinplate remains a critical material for food cans, aerosol containers, chemicals, and pharmaceuticals, especially in developing economies experiencing rapid urbanization. Tin stabilizers, catalysts, and tin-based chemicals used in PVC production, coatings, and glass processing further support steady industrial demand. These applications ensure that the Tin Market maintains a resilient demand base across essential manufacturing sectors.

Material innovation is emerging as a transformative driver within the Tin Market, particularly in renewable energy and high-performance technologies. Tin-based anodes for lithium-ion and sodium-ion batteries have demonstrated 3–4 times higher theoretical capacity than conventional graphite, drawing significant interest from next-generation battery developers. Additionally, tin-based halide perovskites represent a promising pathway for lead-free solar cells, supporting global clean energy goals. These innovations highlight tin’s growing role in advanced materials research and energy technology development.

Sustainability and responsible sourcing requirements are reshaping demand patterns in the Tin Market. With recycled tin accounting for approximately 30% of global supply, circularity is becoming a critical pillar of future market growth. ESG-driven procurement standards, conflict-free mineral sourcing initiatives, and international regulatory frameworks are compelling manufacturers to adopt transparent, ethically sourced tin. As global industries transition toward low-impact materials, sustainable and recycled tin is expected to gain increasing market share, reinforcing the long-term competitiveness of the Tin Market.

Energy Storage Technologies, Lead-Free Solder, Advanced Materials, and Circular Economy Trends Create High-Value Opportunities in the Tin Market

The Tin Market is entering a phase of significant opportunity expansion driven by the increasing adoption of tin-based materials in energy storage technologies. Tin’s emerging role in high-capacity lithium-ion, sodium-ion, and solid-state battery anodes presents one of the strongest long-term opportunities. Tin-based anode formulations, which offer enhanced conductivity and greater charge capacity, align with global trends in EV adoption, grid-scale storage, and next-generation energy solutions. These advancements position the Tin Market as a critical enabler of future battery innovation.

Lead-free solder represents another high-growth opportunity in the Tin Market, supported by global environmental regulations such as RoHS and WEEE. As the electronics industry transitions to safer, lead-free materials, refined tin and specialized tin alloys have become essential for solder manufacturing. With lead-free solder accounting for over 80% of global solder production, the Tin Market benefits directly from increasing electronics output, 5G infrastructure expansion, semiconductor advancement, and the proliferation of connected devices across industries.

The Tin Market benefits from expanding demand for tinplate and chemical-grade tin products. Growing consumption of packaged food, beverages, pharmaceuticals, and industrial goods in emerging economies continues to drive the use of tin-coated steel. Tin chemicals—used in PVC stabilization, polymer catalysis, coatings, and optical glass—provide additional value-added opportunities as industrial output increases across Asia-Pacific, Africa, and Latin America.

Circular economy initiatives are generating considerable opportunities across the Tin Market, with recycled tin already contributing a significant portion of global supply. Advances in electronic waste recovery, solder recycling, and urban mining technologies are improving extraction efficiency and reducing reliance on primary tin mining. These developments position recycled tin as a strategic growth segment, supported by global sustainability policies and rising corporate commitments to low-carbon materials.

Smart manufacturing represents another high-potential opportunity for the Tin Market. AI-enabled smelting processes, digital ore-grade monitoring, automated sorting technologies, and blockchain-based traceability systems are transforming tin production and refining operations. These technologies reduce operational losses, improve metal purity, enhance ESG compliance, and strengthen supply chain transparency. As global industries increasingly prioritize efficiency, sustainability, and ethical sourcing, digital transformation is expected to create long-term competitive advantages within the Tin Market.

Tin Market Segment Analysis:

Based on Product Type, the Tin Market is segmented into Metallic Tin, Tin Alloys, Tin Chemicals, Tinplate, and Others. The Metallic Tin segment dominated the market in 2025, accounting for over 55% of total market revenue, driven by its extensive use in solder production, plating, and high-purity industrial applications. Metallic tin remains the primary feedstock for electronics-grade solder, which consumes of metallic tin annually. Its superior malleability, corrosion resistance, and electrical conductivity continue to strengthen its demand across semiconductor assembly, automotive electronics, and renewable energy systems.

Tin Alloys, including lead-free solders, bearing alloys, and speciality metal blends, are gaining strong traction due to the global shift toward RoHS-compliant lead-free soldering materials. Tin alloys accounted for approximately 22% of total tin usage in 2025, with demand rising sharply across EVs, 5G components, and industrial machinery. Tin Chemicals' steady growth is supported by rising use of PVC stabilisers, catalysts, and glass coatings in the construction and packaging industries.

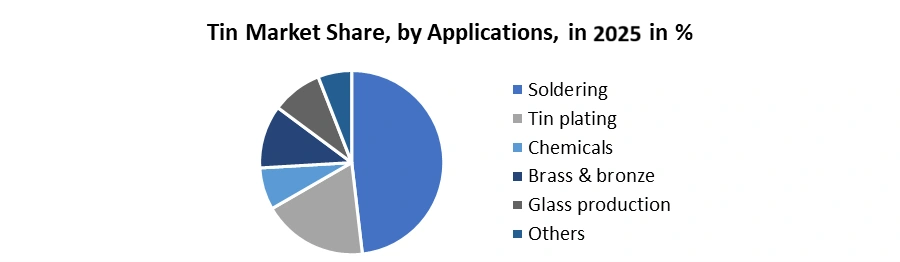

Based on Application, the Tin Market is segmented into Soldering, Tin Plating, Chemicals, Brass & Bronze, Glass Production, and Others. The Soldering segment dominated the market in 2025 contributing over 50–51% of global tin consumption, as tin-based solder remains indispensable in electronic circuit assembly, PCB manufacturing, EV power electronics, and solar ribbon bonding. With global electronics production exceeding $3 trillion in annual output, solder-grade tin demand, positioning soldering as the largest and fastest-growing application segment.

The Tin Plating segment, accounting for 11–12% of total demand, continues to grow steadily due to its role in food-grade packaging, corrosion-resistant coatings, and industrial containers. Tin Chemicals contributed 16%, driven by rapid construction, polymer stabilisation, and surface-treatment demand. Applications such as Brass & Bronze and Glass Production hold smaller but stable shares, collectively contributing around 10%, and speciality alloy manufacturing and float-glass processes are used in automotive and architectural sectors.

Tin Market Regional Analysis:

The Asia–Pacific (APAC) region dominated the global Tin Market, accounting for over 65% of global consumption and nearly 70% of refined tin production in 2025. China is 50% of global tin demand, fueled by its massive electronics manufacturing ecosystem, which includes the world’s largest PCB, semiconductor assembly, consumer electronics, and EV power-electronics industries. Since solder accounts for nearly 51% of global tin usage, APAC’s dominance reflects the region’s technological and manufacturing scale.

On the supply side, APAC is equally influential. China, Indonesia, Myanmar, Malaysia, and Thailand collectively control a major share of global tin ore and refined production capacity. Indonesia and Myanmar remain crucial ore suppliers to China, while Malaysia Smelting Corporation, Yunnan Tin, PT Timah, and Thaisarco anchor the region’s refining capabilities. Regulatory actions in APAC, such as Indonesia’s mining law reforms or Myanmar’s mine suspensions, immediately impact global tin supply and LME pricing, highlighting the region’s strategic control over the supply chain.

Recent Industry Developments (2025–2026)

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 15 September 2025 | PT Arsari Tambang | The company committed USD 422.71 million for a strategic acquisition of Canadian mining assets following the Indonesia-Canada Economic Partnership Agreement. | This move achieves vertical supply chain integration and reduces geographic concentration risks for Indonesian refined tin. |

| 10 November 2025 | Alphamin Resources | The operator adjusted its 2025 production target to 18,500 tons following operational suspensions at the Bisie mine due to regional unrest. | Supply tightening from the DRC contributes to a global supply deficit expected to persist through 2026. |

| 22 August 2024 | Yunnan Tin Group | Launched the Yunnan Tin & Indium Laboratory to develop high-value advanced materials for the full value chain. | Strengthens technological leadership and national strategic resource security for high-purity tin applications in 2025. |

Competitive Landscape

The Tin Market is fragmented at the smelting/refining level, with Yunnan Tin, Minsur, PT Timah, Malaysia Smelting Corporation (MSC), Thaisarco, Yunnan Chengfeng, Guangxi China Tin, Gejiu ZiLi, Jiangxi Nanshan, China-Tin Group and Hsikwang Shan Twinkling Star forming the core global refined tin supply base. EM Vinto and Metallo Chimique strengthen Bolivia and EU recycling footprints, while ArcelorMittal and The Dow Chemical Company anchor downstream steel/tinplate and chemical demand. Niche technology and alloy players such as Indium Corporation, DuPont & Do, Guangzhou HUAXI Group, MSC Group and others intensify competition in high-margin electronics, solder and specialty chemical applications.

Scope of the Global Tin Market: Inquire before buying

| Tin Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 7.57 USD Bn. |

| Forecast Period 2026-2032 CAGR: | 3.4% | Market Size in 2032: | 9.57 USD Bn. |

| Segments Covered: | by Product Type | Metallic tin Tin alloys Tin chemicals Tinplate Others |

|

| by Application | Soldering Tin plating Chemicals Brass & bronze Glass production Others |

||

| by End Use Industry | Electronics & semiconductors Automotive Packaging Construction Chemicals Energy & storage technologies Industrial machinery |

||

Tin Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players / Competitors Profiles Covered in Brief in Global Tin Market Report in Strategic Perspective:

- Yunnan Tin

- PT TIMAH Persero Tbk

- Minsur

- Malaysia Smelting Corporation Berhad

- Thailand Smelting and Refining Co. Ltd.

- Empresa Metalúrgica Vinto

- Aurubis AG

- ArcelorMittal

- Indium Corporation

- Hindustan Tin Works Ltd.

- DuPont de Nemours Inc.

- Alphamin Resources Corp.

- Metallo Belgium NV

- Silmet

- AfriTin Mining

- Kasbah Resources

- Elements 51

- ABM Metal Tech

- Bharat Tin Works

- Nikitha Containers Pvt. Ltd.

- Saksham Containers Pvt. Ltd.

- Suraj Containers Ltd.

- Swastik Tins Pvt. Ltd.

- Zenith Tins Pvt. Ltd.

- Bharat Ultimate Packaging Pvt. Ltd.