Satellite Payloads Market – Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2030

Overview

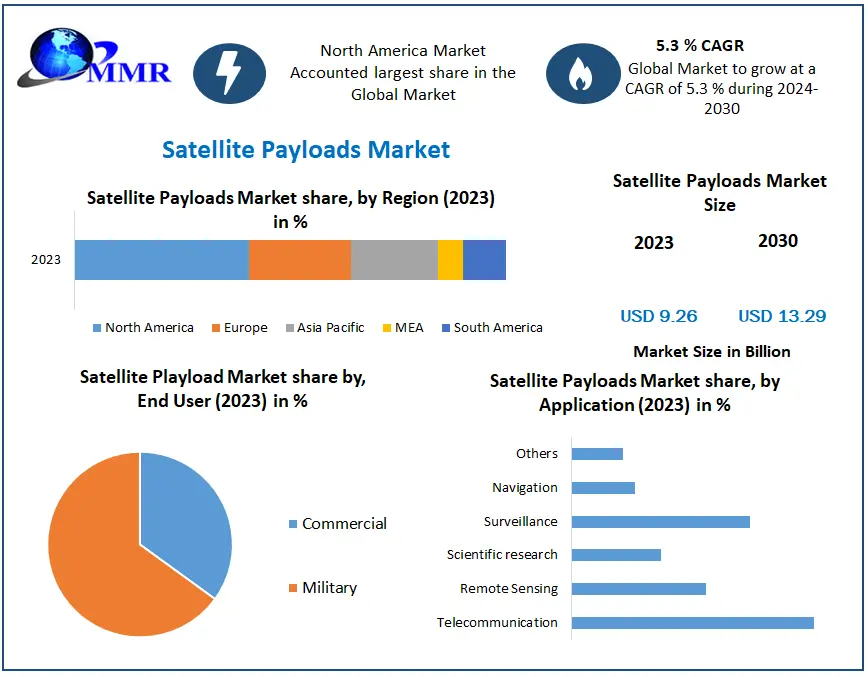

Satellite Payloads Market was valued at USD 9.26 Bn in 2023 and is expected to reach USD 13.29 Bn by 2030, at a CAGR of 5.3 % during the forecast period.

Satellite Payloads Market Overview

Satellite payload is defined as modules carried on satellites with the ability to perform certain functionalities. The satellite consists of the payload and the bus. Satellite bus is used to carry subsystems and payloads, whereas a payload is developed to perform specific functions such as communications, imaging, and navigation while in orbit. Satellite payload includes equipment such as transponders, repeaters, antennas, spectrometers, and cameras among others. Earth Observation and remote sensing applications use cameras, radar, and other sensing equipment for collecting relevant data. To enable the delivery of satellite communication services, the payload includes antennas, receivers, and transmitters, based both in space and on the ground, for transmission and storage of the data needed.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Increasing adoption of small satellites for Earth observation, telecommunication, and imaging drives the growth of the Satellite Payloads Market. Small satellites are increasingly being used by government, defense & intelligence, and commercial organizations to enable launch of low-cost and efficient payload. The greater need for Earth observation for delivery of high-resolution imagery for civil engineering & construction, agriculture & forestry, and transportation industries further accelerates the demand for satellite payload.

Satellite Payloads Market Dynamics

Satellite Payloads Market Trend

Key development in software satellites to catalyze the Satellite Payloads Market growth

Satellites with software-defined capability, which is configured through commands from ground stations, have an Al-based payload and an operating processor. The satellite have beam-forming antennas, route processors, and demodulation capabilities that are software-defined. These satellites are capable of updating and reconfiguring themselves as needed. By allowing operators to adjust the beams as needed, next-generation software satellites are able to offer improved connectivity for inflight broadband users. Extremely high speed, improved capacity flexibility, redundancy, and backward compatibility supports satellites for future mobility applications, which is expected to boost the Satellite Payloads Market growth. Software-defined satellites and software-defined network solutions have been announced by the growing number of legacy organizations and startups.

For instance, in November 2023, Lockheed Martin announced plans to prepare the first 5G MIL Payload to orbit. The first regenerative non-terrestrial network 5G satellite base station completed the final demo before the space mission. Lockheed Martin SmartSat software, which defines the satellite architecture, is reprogrammable in orbit. Such developments in software-defined satellites fuel the Satellite Payloads Market growth across the globe.

Growth in constellation projects to boost Satellite Payloads Market growth

A satellite constellation is a system of identical or similar-type artificial objects that serve the same goal and are controlled by the same entity. These groups transmit information to ground stations across the globe and are sometimes internally connected. They are complementary and serve as a system. Satellites in swarms rotate through comparable orbits with orbital planes to provide continuous and virtually uninterrupted global coverage this factor significantly boosts the Satellite Payloads Market growth.

In November 2023, the U.K. intended to establish a new constellation of small satellites aimed at improving research on climate change and disaster monitoring with Spain and Portugal. Four Portuguese spacecraft and one built by a U.K. company called Open Cosmos form the first phase of the constellation. U.K.'s Space Agency contributed USD 3.8 million toward developing this satellite. Sixteen satellites with EO and telecommunications payloads included in the Atlantic Constellation when it is done.

As more private companies and governments invest in satellite constellations for telecommunications, earth observation, weather monitoring or other uses, the demand for innovative sensors is growing. These sensors need to be used for the capture and transmission of vital information back to Earth in real time. This makes it easier for organizations and bodies to make informed decisions and this factor significantly boost the Satellite Payloads Market growth.

For instance, in August 2023, the world's leading constellation operators are planning a significant increase in the number of second-generation satellites that join LEO orbit, moving toward more powerful spacecraft at lower Earth orbits. After four years of launching more than 4,000 Starlinks, SpaceX is the largest constellation in terms of satellite count and mass.

Increased government investment in defense, security, and commercial applications to fuel Satellite Payloads Market growth

The demand for satellite equipment is fueled by the increasing importance of space-based assets for defense and security purposes. These payloads are used for monitoring, intelligence gathering, and early warning systems. For defense and safety purposes, satellites play a key role in the surveillance and gathering of information, which significantly boost the Satellite Payloads Market growth.

For example, in April 2023, in order to increase awareness of the space domain, the U.S. Space Force invested in-ground and subspace-based sensors and surveillance systems as well as data from businesses interested in tracking satellites. To improve the detection, tracking, and identification of objects orbiting the Earth, the military branch's budget for fiscal year 2024 includes USD 584 million for space-tracking activities, such as the development of optical telescopes and surveillance satellites.

The Space Force has asked for funding to support the development of Deep Space Advanced Radar Capability, a planned radar system that detect enemy threats in geostationary orbit. The budget request for FY 2024 also includes enhancements to the ground-based Electro-Optical Deep Space Surveillance System to detect previously undetectable space threats and collect intelligence to support actionable space domain awareness. Satellite payloads are capable of tracking ballistic missile launches, as well as providing early warning systems, are also recording investments by governments. As they allow for quick responses to missile threats and the protection of territories and populations, these payloads are essential for national security, which is expected to boost the Satellite Payloads Market growth.

Slowdown of malfunctioning of the sensor to limit Satellite Payloads Market growth

The success of a space mission is directly affected by the malfunctioning of payloads. Sensor data are vital for accuracy and reliability to make the right decisions during a mission. Sensor failure results in insufficient data collection, measurement errors, and a more severe decision-making process. In such situations, leaked information frustrates the mission objectives and thwarts scientific discoveries or the mission's planned operational objectives, which limits the Satellite Payloads Market growth. Space-based sensors are exposed to extremely harsh conditions, including intense radiation, vacuum, and temperature fluctuations. These environmental conditions lead to sensor degradation, premature wear, and even complete failure, which is expected to hamper the satellite payloads market growth. Ensuring the reliability and durability of satellite sensors is an important task for both space agencies and manufacturers. The results are disastrous, including data loss, mission failure, and waste of precious resources if sensors fail on a space mission.

In April 2023, a Japanese company specializing in developing robotic spacecraft and other technology attempted to land a rover and a lander on the surface of the moon. The failure was caused by a discrepancy between the altitude information from the lander's sensors and its actual position.

Satellite Payloads Market Segment Analysis

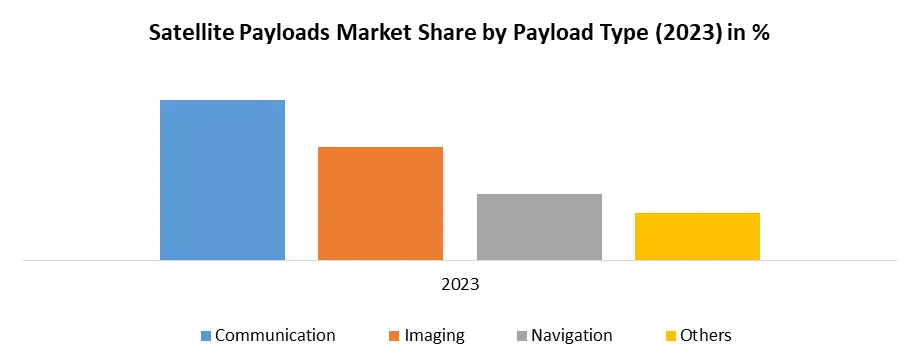

Based on Payload Type, the market is segmented into Communication, Imaging, Navigation, and Others. The communication segment dominated the market in 2023 and is expected to hold the largest Satellite Payloads Market share over the forecast period. Laser communications are better as light wavelengths are packed much more tightly than sound waves, and they transmit more information per second with a stronger signal. So laser communications and laser sensing are important in mortar defense and other crucial aerospace applications. Increasing adoption of laser-based communication payloads in commercial and defense applications. In August 2020, Airbus was contracted by Arabsat to build BADR-8, its new generation telecommunications satellite. BADR-8 replace and increase Arabsat's capacity and augment its core business at the BADR hotspot 26°E. BADR-8 include the innovative Airbus-developed TELEO optical communications payload demonstrator.

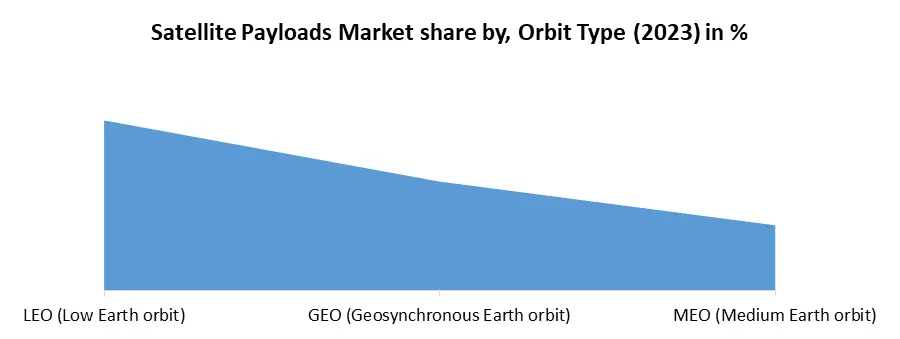

Based on Orbit Type, the market is segmented into LEO (Low Earth orbit), GEO (Geosynchronous Earth orbit), and MEO (Medium Earth orbit). LEO segment dominated the market in 2023 and is expected to hold the largest Satellite Payloads Market share over the forecast period. LEO orbit is near to the Earth's surface and satellites circle the planet less time to provide continuous surveillance over area. The increasing launch of communication, imaging, navigation, and other satellites in LEO by various key market players is expected to boost segmental growth in Satellite Payloads Market over the forecast period.

Satellite Payloads Market Regional Analysis

North America dominated the market in 2023 and is expected to holds the largest Satellite Payloads Market shares over the forecast period. The growth is attributed to the increasing demand for satellite payloads for various applications and technological advancements in digital payloads carried out by SpaceX, NASA, and others. The US was the highest spender on space programs, with an approximate investment of USD 62 billion in 2022.

The US accounted for more than half of the global spending of USD 54.6 billion in 2021 on spaceflight activities. Out of the total investment, half of the amount is invested in civil spaceflight activities such as NASA and supporting commercial space, and the other half went to defense programs in the Air Force, Space Force, and other parts of the Department of Defense, which is expected to boost the Satellite Payloads Market growth.

In March 2022, the US Space Force passed a critical design review of a satellite communication payload developed by Boeing. In 2020, The Boeing Company and Northrop Grumman Corporation won separate contracts worth USD 191 million and USD 253 million, respectively, to design payloads for the Protected Tactical Satcom (PTS) program of the US Space Force, a planned network of jam-resistant geostationary satellites for military classified and unclassified communications. Growing expenditure on space programs and a rising number of satellite launches for military and commercial applications drive the growth of the market across the region.

Satellite Payloads Market Scope: Inquire before buying

| Global Satellite Payloads Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | US $ 9.26 Bn. |

| Forecast Period 2024 to 2030 CAGR: | 5.3% | Market Size in 2030: | US $ 13.29 Bn. |

| Segments Covered: | by Payload Type | Communication Imaging Navigation Others |

|

| by Orbit Type | LEO (Low Earth orbit) GEO (Geosynchronous Earth orbit) MEO (Medium Earth orbit) |

||

| by Frequency Band | S-band L-band C-band X-band VHF & UHF band Others |

||

| by Application | Telecommunication Remote Sensing Scientific research Surveillance Navigation Others |

||

| by End User | Commercial Military |

||

Satellite Payloads Market, by Region:

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Leading Satellite Payloads keyplayers include:

1. Lockheed Martin Corporation (U.S.)

2. Honeywell International Inc. (U.S.)

3. The Boeing Company (U.S.)

4. Thales S.A. (France)

5. Raytheon Technologies (U.S.)

6. Airbus Defence and Space (Germany)

7. L3 Harris Corporation (U.S.)

8. Mitsubishi Electric Corporation (Japan)

9. ISRO (India)

10. General Dynamics Mission Systems, Inc. (U.S.)

11. Space Exploration Technologies Corporation (U.S.)

12. MDA Corporation (U.K.)

13. Northrop Grumman Corporation (U.S.)

14. Viasat, Inc. (Carlsbad, CA)

15. Lucix Corporation (USA)

Frequently asked Questions:

1] What segments are covered in the Global Satellite Payloads Market report?

Ans. The segments covered in the Satellite Payloads Market report are based on payload type, orbit type, frequency band, application, and End-user.

2] Which region is expected to hold the highest share of the Global Satellite Payloads Market?

Ans. The North America region is expected to hold the highest share of the Satellite Payloads Market.

3] What is the market size of the Global Satellite Payloads Market by 2030?

Ans. The market size of the Satellite Payloads Market by 2030 is expected to reach USD 13.29 Bn.

4] What was the market size of the Global Satellite Payloads Market in 2023?

Ans. The market size of the Satellite Payloads Market in 2023 was valued at USD 9.26 Bn.

5] Key players in the Satellite Payloads Market.

Ans. Lockheed Martin Corporation (U.S.), Honeywell International Inc. (U.S.), The Boeing Company (U.S.), Thales S.A. (France), Raytheon Technologies, etc.