Rolling Stock Market– Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

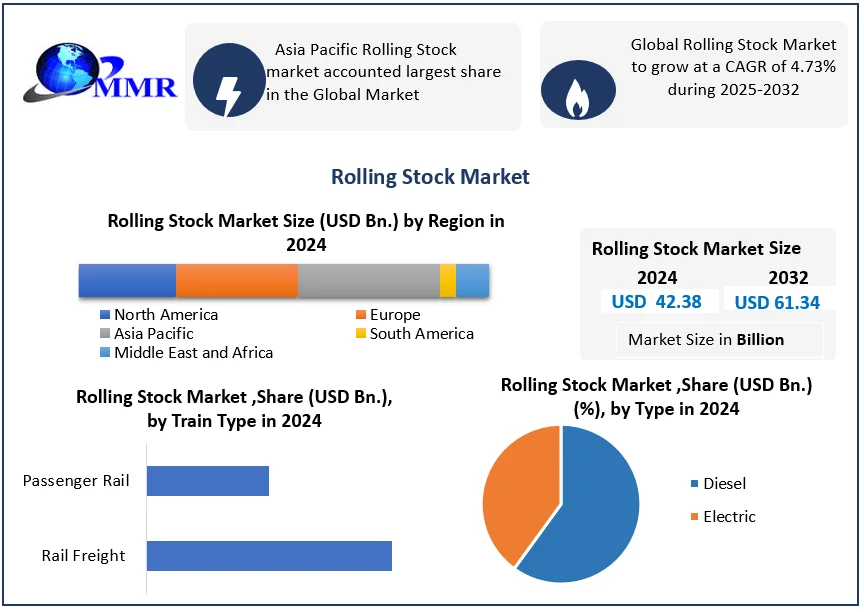

Global Rolling Stock Market size was valued at USD 42.38 Bn. in 2024, and the total Rolling Stock Market revenue is expected to grow by 4.73% from 2025 to 2032, reaching nearly USD 61.34 Bn.

Global Rolling Stock Market Overview

The Rolling Stock Market includes the production, distribution, and servicing of rail trains, i.e., locomotives, passenger coaches, freight wagons, and metro/transit units, as described in this report.

The Global Rolling Stock Market is driven by urbanization, government expenditures on rail infrastructure, and a move towards sustainable transport. The report identifies demand-supply drivers, with rising orders for energy-efficient, high-speed trains, specifically in Asia-Pacific and Europe, while supply chain issues and raw materials prices affect production schedules.

In 2024, the Asia-Pacific region was the top performer, mainly because of metro network growth in China and India. In comparison, Europe and North America are moving more slowly, focusing on upgrading old trains and investing in freight rail.

Key companies in the market include CRRC Corporation (China), Alstom (France), Siemens Mobility (Germany), and Wabtec Corporation (U.S.). These companies are known for their strong strategies and innovations. The report also shows a shift in demand from freight to passenger transport, although freight still needs more investment and growth.

Looking ahead from 2025 to 2032, market growth driven by metro expansion, replacing old trains, and the rise of autonomous and connected train technologies. This report helps readers understand market trends, major players, and future opportunities. To know about the Research Methodology:-Request Free Sample Report

To know about the Research Methodology:-Request Free Sample Report

Global Rolling Stock Market Dynamics

Revolution in Rail Electrification & Automation to Drive Global Rolling Stock Market Growth

The rail industry is changing with battery-electric, hydrogen-powered, and autonomous trains getting traction. Alstom's Coradia iLint (a hydrogen train) and Siemens' Mireo Plus B (a battery-electric train) are setting new standards, and CRRC's autonomous metro systems are growing significantly in Asia. Governments are increasing the pressure for zero-emission rail networks, where the EU will not allow any new diesel trains after 2035. All this momentum is driving a higher demand for next-gen rolling stock, and it is forecasted that global rail electrification investments will grow at a CAGR of 8% through 2025.

Urbanization & High-Speed Rail Expansion to Drive Global Rolling Stock Market Growth

In the Asia-Pacific region, China and India lead with the most aggressive growth plans in regard to metro and high-speed rail (HSR) networks. China intends to double its HSR network by 2035. India's government thrashed out existing projects before launching the Vande Bharat Express and fast-paced metro projects. Europe is modernizing its aged fleets. Germany and France together have committed €7B+ in new trains. The United States is investing in Amtrak upgrades and its California HSR system.

Global Rolling Stock Market Segment Analysis

Based on type, the diesel segment dominated the Rolling Stock market. This is mainly due to the ability of diesel locomotives to operate well in areas with limited electrification or perform freight responsibilities in regions that are maximizing heavy haul weight in long hauls. Almost all rail freight in North America is still provided by diesel rolling stock as it provides the highest level of torque, is the most reliable in designated outlying areas, and the upfront cost to purchase is significantly less than electric. It should not be a shock that industries like mining, agriculture, and intermodal logistics predominantly rely on diesel rolling stock to proceed through their operations without reliance on overhead electrification.

Conversely, electric rolling stock is rapidly growing, particularly in the passenger rail and urban transit space, because of government incentives, a decrease in operational costs, and zero direct emissions. Yet, diesel rolling stock is still the dominant force in freight and regional rail operations, providing market leadership for now and the mid-term. Electric rolling stock may gain traction as infrastructure is enabled, but diesel will continue to play an essential role in heavy-haul, non-electrified rail networks.

Based on Train Type, the rail freight industry dominates the market, having the largest share of the market because of its vital mode of transport for bulk cargo from ship to supply chain logistics. Freight has always been a staple mode of transport in the mining, agricultural, and manufacturing sectors due to the vehicle's ability to economically haul significant amounts of loads over vast distances. Because of the high torque and reliability of diesel locomotives, the rail freight segment still dominates, especially in regions with lesser electrified rail systems, the sustainable movement is now instigating renewed innovation with hybrid and hydrogen fuel cell freight trains, which will enable this segment to continue to support working industries while being more environmentally conscious.

The passenger rail segment is now also experiencing quicker adoption rates with the rise of urbanization, government investments into high-speed rail, and as demand for eco-friendly public transit grows. Urban cities have started to build and expand electric multiple units (EMUs) and metro systems across all continents to help attract and provide transport from vehicular traffic, to create a reduction in congestion and carbon output. Even though it holds a lesser share of the market, the passenger rail segment has a sharper growth curve, supported by current smart city initiatives to embrace the opportunities presented by mobility solutions that can be put in place to fit the changing public transport initiatives across the globe.

Rolling Stock Market Regional Analysis

The Rolling Stock Market is segmented into various regions such as North America, Europe, the Middle East & Africa, South America, and the Asia Pacific. The Asia Pacific region is dominating the global market and is estimated to maintain dominance over the forecast period, owing to the adoption of rail transportation for passengers and goods. Also, the regional market growth can be attributed to the increasing investments in electric trains and metro trains in countries such as India, Taiwan, China, and other countries.

The Middle East & Africa region is expected to be fast-growing over the forecast period. The mining and oil & gas industries are increasing applications for the transportation of goods is leading to the growth of the rolling stock market globally. The regional market is also driven by the increasing use of rolling stock owing to their high torque power and enhanced safety. The report also helps in understanding Rolling Stock Market dynamics, structure by analysing the market segments, and projects the Rolling Stock Market size. Clear representation of competitive analysis of key players by Application, price, financial position, Product portfolio, growth strategies, and regional presence in the Rolling Stock Market makes the report an investor’s guide.

Global Rolling Stock Market Competitive Landscape

The Global Rolling Stock Market is competitive, with CRRC Corporation (China) being the world's largest producer, utilizing economies of scale, state financing, and assertive pricing to win contracts in Asia, Africa, and Latin America. Alstom (France) and Siemens Mobility (Germany) are top companies in high-end rail technologies—Alstom with its hydrogen fuel cell-powered Coradia iLint and Siemens with AI-based Railigent predictive maintenance systems. Wabtec (U.S.) continues to be North America's freight rail leader, being the first to develop battery-diesel hybrid locomotives and digital freight.

Hitachi Rail (Japan/UK) leads in high-speed rail (HS2, Shinkansen) and driverless metro systems, while Stadler Rail (Switzerland) takes a dominant share in regional trains, tramways, and bespoke solutions for low-density routes. Hyundai Rotem (Korea) is increasing its presence in metropolitan transit and high-speed rail through government support. Moreover, Titagarh Rail Systems (India) and CAF (Spain) are also coming up as prominent regional players, bidding for metro and light rail orders in expanding markets. The competitive scenario gets an added push by joint ventures, localization efforts, and R&D in automation and alternative propulsion, as makers compete to gain a grip in an increasingly innovation-based business.

Global Rolling Stock Market Key Developments

In April 2024, Alstom rolled out the first of six hydrogen-fuel-powered Coradia iLint trains into service in Lombardy, representing the rolling stock sector's first fully hydrogen-fuel-powered commercial route (Brescia-Edolo). This project further facilitates Europe's movement to zero-emission rail and competes with hydrogen companies such as Siemens, competing in the clean energy sphere. This project sets a new standard in sustainable passenger rolling stock for the world.

In May 2024, Siemens Mobility introduced Mireo Plus B battery trains into service in Bavaria, launching into operation a 120 km route between Augsburg and Füssen after the battery trains had successfully undergone a pilot trial. The trials show that transitioning to battery-electric solutions for rolling stock is resulting in a paradigm shift in the market, independently demonstrating seamless operation with interim charging. Deployment competes with Alstom's hydrogen trains and indicates Siemens is competing with Alstom's hydrogen trains and exhibiting leadership in zero-emission regional rail.

In December 2025, after an eighteen-month implementation period, Wabtec has now brought their 120 million USD mining authorities automation project involving the Collahuasi copper mine in Chile, involving autonomous ore trains operating in increased mine altitude (4,500 meters).

In January 2025, Hitachi began testing driverless Ginza Line (Tokyo) at 20cm obstacle detection. Hitachi's test is signaling to the world that the rolling stock market is taking steps towards the autonomous future; Japan is now competing with Europe to develop the next generation of metro systems.

Global Rolling Stock Market Key Trends

1. Green Transition The hydrogen and battery train revolution is picking up speed with Alstom’s Coradia iLint (Europe) and CRRC’s hydrogen trams (Asia) spearheading commercialization efforts. By 2025, there will be over 300 zero-emission trains that will be operational as regulations on diesel become more stringent (the EU’s 2035 mandate) and green subsidies become more readily available.

2. Digitalization & Automation Smart trains are transforming rail networks, through Siemens’ AI-enabled Railigent to reduce failures, and Hitachi's driverless metros to enhance efficiency, cutting downtime by 30%. Global Rolling Stock Market Key Highlights

Global market analysis and forecast, in terms of value.

Comprehensive study and analysis of market drivers, restraints, and opportunities influencing the growth of the Global Rolling Stock Market. Global market segmentation on the basis of type, source, end-user, and region (country-wise) has been provided. Global market strategic analysis with respect to individual growth trends, future prospects, along with the contribution of various sub-market stakeholders, has been considered under the scope of study. Global market analysis and forecast for five major regions, namely North America, Europe, Asia Pacific, the Middle East & Africa (MEA), and Latin America, along with country-wise segmentation.

Profiles of key industry players, their strategic perspective, market positioning, and analysis of core competencies are further profiled. Competitive developments, investments, strategic expansion, and the competitive landscape of the key players operating in the Global Market are also profiled.

Rolling Stock Industry Ecosystem

Global Rolling Stock Market Scope: Inquire before buying

| Global Rolling Stock Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 42.38 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 4.73% | Market Size in 2032: | USD 61.34Bn. |

| Segments Covered: | by Product | Locomotive Rapid Transit Vehicle Wagon Other Product |

|

| by Type | Diesel Electric |

||

| by Train Type | Rail Freight Passenger Rail |

||

Rolling Stock Market, by Region

North America (United States, Canada and Mexico)

Europe (United Kingdom, France, Germany, Italy, Spain, Sweden, Russia, Rest of Europe)

Asia Pacific (China, Japan, South Korea, India, Australia, Malaysia, Thailand, Vietnam, Indonesia, Philippines, Rest of APAC)

Middle East and Africa (South Africa, GCC, Nigeria, Egypt, Turkey, Rest of MEA)

South America (Brazil, Argentina, Colombia, Chile, Peru, Rest of South America)

Rolling Stock Market, Key Players

1. North America

Wabtec (USA)

The Greenbrier Companies (USA)

Hitachi Rail Systems (North America)

2. Europe

Alstom Transport (France)

Siemens Mobility (Germany)

Stadler Rail AG (Switzerland)

CAF (Construcciones y Auxiliar de Ferrocarriles) (Spain)

3. Asia Pacific

CRRC Corporation Limited (China)

Hyundai Rotem (South Korea)

Kawasaki Heavy Industries (Japan)

TMH (Transmashholding) (Russia)

Frequently Asked Questions:

1. Which region has the largest share in the Global Rolling Stock Market?

Ans: The Asia Pacific region holds the highest share in 2024.

2. What is the growth rate of the Global Rolling Stock Market?

Ans: The Global market is growing at a CAGR of 4.73% during the forecasting period 2024-2030.

3. What segments are covered in the Global Rolling Stock market?

Ans: The Rolling Stock Market is segmented into product, type, train type, and region.

4. Who are the key players in the Global Rolling Stock market?

Ans: The important key players in the global market are – CRRC Corporation Limited, Bombardier Transportation, Alstom Transport, GE Transportation, Trinity Rail Group, LLC, Siemens Mobility, Stadler Rail AG, Hitachi Rail Systems, The Greenbrier Co, Hyundai Rotem., CJSC Transmashholding, Kawasaki Heavy Industries Ltd., Stadler Rail AG, TRANSMASHHOLDING

5. What is the study period of this market?

Ans: The Global Rolling Stock Market is studied from 2024 to 2032.