Ride sharing Market Size by Service Type, Vehicle Type, Business Model, Platform and Region - Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2032

Overview

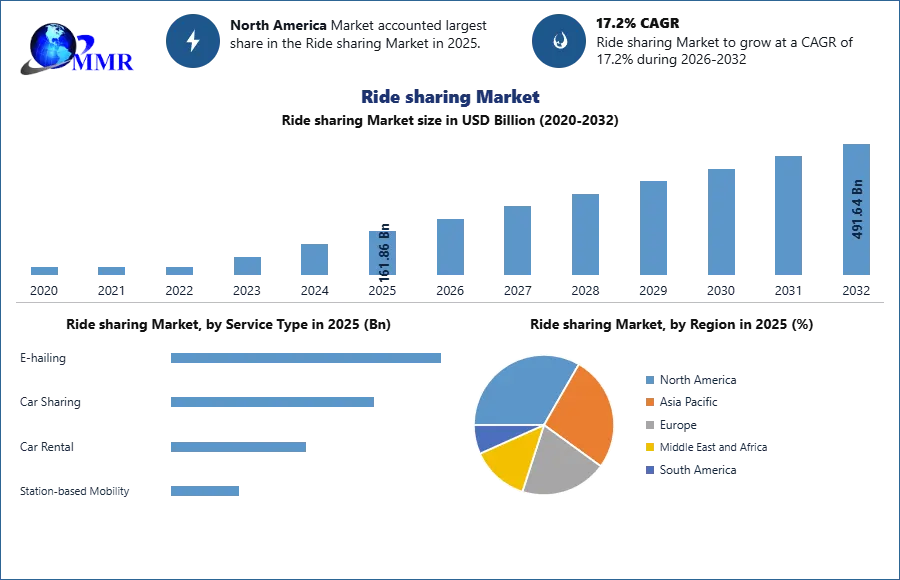

Ride Sharing Market size was valued at USD 161.86 Billion in 2025 and the total revenue is expected to grow at CAGR 17.2 % through 2026 to 2032, reaching nearly USD 161.86 Billion.

The MMR report provides a comprehensive examination of ride-sharing economics and market dynamics, covering pricing models and cost-structure (2020–2025), regional price comparisons, driver incentives, and revenue streams; consumer behavior and regional preferences; technological innovations (AI/ML, digital payments, EVs, AVs, IoT, blockchain); market penetration and adoption forecasts; urban vs. rural segmentation; and the global regulatory and compliance landscape all supported by data, case studies, and actionable recommendations.

Ridesharing is an alternative mode of transportation in which more than one person shares the use of a vehicle, such as a van or automobile, to complete a trip. Prior to the pandemic, ride-sharing services were the most popular because they provided a convenient and cost-effective way of personal mobility through the use of a transportation network infrastructure. Ride sharing services have several advantages, including quick booking choices, minimal carbon footprints, economical door-to-door ride services, and no parking hassles. Reduced demand for public transportation due to the danger of infection during the Covid-19 epidemic is supporting the rise of select ride sharing services.

The introduction of big data analytics, IoT, and AI enables smart mobility alternatives and the expansion of cab booking services. With the passage of time and demand, mobility service providers (MSPs) developed many kinds of ride sharing services such as e-hailing, private vs. corporate vehicle sharing, carpooling, automobile leasing, and so on. Users may select from a wide range of choices based on their demands, distance travelled, and personal comfort. However, as a result of the pandemic, the ride-hailing sector has become one of the most hit industries in the automobile industry.

All online and offline booking channels that link passengers and drivers are included in the Ride-hailing & Taxi market sector. Traditional taxi services that may be hired over the phone, Transportation Network Companies (TNCs) that offer trips in private automobiles, and Ride Pooling services are all included. When a passenger wants a ride, he or she is paired with a driver. TNCs include Uber and Lyft, which match customers with drivers and charge a fee for this service, as well as firms like Moia and Via, which offer Ride Pooling by combining passenger itineraries. Taxi firms that provide journeys via an app (for example, Free Now) are also included in this group.

To know about the Research Methodology :- Request Free Sample Report

Ride Sharing Market Dynamics

Increasing Internet and Smartphone Penetration: The fast acceptance of smart devices such as smartphones and smart wearables, as well as the increased usage of internet data, has generated several chances for Ride Sharing services all over the world, hence magnifying the global ride sharing market growth. The essential need for using ride-hailing services is internet access. Users must utilise the internet to download ride-providing programmes on their cellphones in order to obtain ride information and navigation. Internet access is required for V2V communication, navigation, and telematics to work properly. Furthermore, the smartphone applications give numerous security measures such as the driver's identity, number, and image, vehicle number, route tracing data, and records of previous trips.

Carbon Emissions Regulations: Globally, the rate of automotive emissions has been steadily rising over the years. The car sector contributes significantly to global greenhouse gas emissions. Additional efforts are being made by the government, private groups, and automobile manufacturers to reduce growing CO2 emissions. Various organisations, including Canada's International Institute for Sustainable Development, India's Ministry of Environment and Climate Change, and the European Union's Paris Agreement on Climate Change, have set ambitious targets and norms, including expanding forest cover to reduce carbon footprints in the coming years. As a result, these norms are expected to encourage the adoption of these types of sharing services rather than private automobile ownership.Increase in cost of vehicle ownership

Finance, fuel, maintenance, registration/taxes, and maintenance & repair, as well as depreciation, all contribute to the cost of owning a vehicle. The expense of automobile ownership rises year after year. Fuel prices and maintenance expenses have risen dramatically in recent years, and the similar trend is expected to continue. As cities become increasingly congested with people and automobiles, owning a car has become more of a liability than an asset. Because the millennial generation is uninterested in having a car, the rate of automobile ownership among those aged 18 to 35 has fallen over time. Other factors contributing to the fall in automobile ownership include poor public transit connection in major cities and the growing tendency of online shopping, among others. Ride-hailing service businesses may benefit from these demographics because the new tech-savvy generation is one of the largest users of these services.

Rising Micromobility Demand to Drive Market Growth: Micro-mobility is defined as the capacity to travel short distances with vehicles that only seat one or two persons. Light vehicles such as mopeds, motorcycles, scooters, and longboards are included in this category. Shared micro-mobility is a sensible choice for city commuters looking for a fast journey without the hassle of public transit. The concept of micro-mobility has a significant influence on how to utilise scooters and bikes and generate money from them. As traffic congestion worsens, particularly in major cities, there is a huge opportunity for micro-mobility to help alleviate these issues. The Volkswagen Group, for example, is promoting micro-mobility as part of its electric mobility strategy. The company has introduced Cityskater and Streetmate electric scooters in Geneva. Daimler and BMW together are offering scooters on rent in more than 6 cities in Europe.

Different nations' transportation policy and opposition to traditional transportation services: The operation of app-based mobility services is not controlled by a legal authority in many countries. As a result, their operations are not defined or regulated by the government. Taxi services must have their own permits and registration. Because many app-based taxi firms do not own vehicles, this makes it difficult for them to function. Regulators around the world have proposed or adopted requirements for the collection, use, transfer, security, storage, and other processing of personally identifiable information and other data relating to individuals, and the number, enforcement, fines, and other penalties associated with these laws is growing.

The European Union's General Data Protection Legislation (GDPR), which went into effect in May 2018, is an example of such a regulation. The California Customer Privacy Act (CCPA), which goes into effect in January 2020, also governs consumer data collecting in the ride-sharing industry. Stringent vehicle registration and licence rules make it impossible for an app-based taxi fleet that provides ride-sharing services. This has hampered the expansion of ride-hailing services in numerous nations and areas

Ride Sharing Market Segment Analysis

Based on Service Type, in 2025, the Ride Sharing Market is segmented into E-hailing, Car Sharing, Car Rental, and Station-based Mobility. E-hailing dominates the market, driven by the widespread use of ride-hailing apps, real-time tracking, and seamless digital payment integration. Car Sharing is witnessing strong growth as consumers and businesses increasingly adopt shared mobility to reduce ownership costs and carbon emissions. The Car Rental segment benefits from rising tourism, business travel, and the integration of app-based booking platforms offering flexible short-term rentals. Station-based Mobility holds a niche but expanding share, supported by urban smart mobility projects and government-backed initiatives to improve last-mile connectivity in metropolitan areas.

Based on Business Model, in 2025, the Ride Sharing Market is segmented into Business-to-Consumer (B2C), Business-to-Business (B2B), and Peer-to-Peer (P2P). The B2C segment holds the largest share, driven by dominant players like Uber, Lyft, and Didi offering convenient app-based ride-hailing services directly to consumers. B2B is growing steadily, supported by corporate mobility solutions, employee transportation programs, and partnerships with enterprises seeking sustainable and cost-efficient commuting options. The P2P segment is gaining traction with the rise of community-based carpooling and shared vehicle platforms that promote affordability, sustainability, and reduced traffic congestion.

Ride Sharing Market Regional Insights:

In 2025, the North American market was worth USD 35.02 billion. Because of the rapid growth of electric vehicles in nations such as Canada, the United States, and Mexico, the area dominates the global market. In addition, transportation service companies are rapidly adopting technologically enhanced features. Uber's presence in Canada is quickly increasing.

For example, Lyft was the first firm to announce the debut of green mode, which provides electric car ridesharing to its consumers, last year. Furthermore, the corporation announced this discovery in the context of the 'Green City Initiative,' which aims to reduce the usage of fossil fuels. As a result of these changes, the market in this region is gaining momentum.

Developing countries in Asia Pacific are likely to have tremendous expansion, mainly in urban transportation. Furthermore, growing and developed nations like India, China, Indonesia, and Japan are expected to have significant expansion in Asia Pacific, mostly in urban transportation.

Furthermore, factors such as an increased desire to save gasoline by giving a ride to colleagues and commuters travelling the same route, as well as an increase in the daily commute to urban workplaces, are likely to boost the Asia Pacific market. The region's rapid population expansion and expanding urbanisation have increased the demand for transportation. The majority of the region's nations are focusing on smart personal mobility to cut travel time and congestion.

Because per capita income in most of these nations is lower than in Western countries, Asia Pacific has a much lower number of automobiles per 1,000 people. As a result, ride sharing provides consumers with the illusion of having a car at a far cheaper cost than really owning one. As a result, people prefer ride-hailing services to personal automobiles. Furthermore, factors such as an increase in the daily commute to urban workplaces and an increasing desire to conserve gasoline by offering a ride to commuters and coworkers travelling the same route are expected to drive the Asia Pacific ride sharing industry.

Recent Industry Developments (2025–2026)

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 05 February 2026 | Uber Technologies Inc. | Uber announced a strategic hardware integration with major EV manufacturers to standardize on-board ride-sharing interfaces for global fleets. | This development significantly lowers operational barriers for drivers switching to electric vehicles across North American and European markets. |

| 29 December 2025 | Lyft and Uber | Both companies partnered with Baidu to initiate large-scale driverless taxi trials in London scheduled for early 2026. | The collaboration marks the first direct cross-continental competition between U.S. and Chinese autonomous vehicle technologies in a major European hub. |

| 14 July 2025 | Lyft Inc. | Lyft successfully completed the acquisition of FREENOW GmbH for a total consideration of approximately $197 million. | This acquisition allows Lyft to expand its geographic footprint into the European market, establishing a massive multi-mobility platform presence outside North America. |

| 22 June 2025 | Uber Technologies Inc. | Uber and Waymo launched autonomous ride-hailing services in Atlanta, covering a 65-square-mile service area. | The launch accelerates the commercialization of Level 4 autonomy within the standard ride-sharing app ecosystem for metropolitan users. |

| 18 May 2025 | Grab Holdings Ltd. | Grab secured a $2.5 billion strategic investment led by Microsoft and Toyota to enhance its cloud-based dispatching AI. | The funding strengthens Grab's market dominance in Southeast Asia by integrating advanced predictive analytics for better vehicle supply management. |

| 12 May 2025 | Uber Technologies Inc. | Uber entered into a definitive agreement with Pony.ai to integrate robotaxi services directly onto the Uber ride-sharing platform. | The partnership creates a hybrid fleet model, bridging the gap between human-driven rides and fully autonomous shared mobility solutions. |

Report Scope:

The Ride Sharing Market research report includes product categorization, product application, development trend, product technology, competitive landscape, industrial chain structure, industry overview, national policy and planning analysis of the industry, and the most recent dynamic analysis, among other things. The study discusses the global market's drivers, opportunities, and limitations.

It discusses the influence of various drivers, trends, and constraints on market demand during the forecast period. The research also outlines market potential on a global scale. The research includes the production time, base distribution, technical characteristics, research and development trends, technology sources, and raw material sources of significant Ride Sharing Market firms in terms of production bases and technologies.

The more precise research also contains the key application areas of market and consumption, significant regions and consumption, major producers, distributors, raw material suppliers, equipment providers, and their contact information, as well as an analysis of the industry chain relationship. This report's study also contains product specifications, manufacturing processes, cost structure, and data information organised by area, technology, and application.

Ride Sharing Market Scope: Inquire before buying

| Ride sharing Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 161.86 USD Billion |

| Forecast Period 2026-2032 CAGR: | 17.2% | Market Size in 2032: | 491.64 USD Billion |

| Segments Covered: | by Service Type | E-hailing Car Sharing Car Rental Station-based Mobility |

|

| by Vehicle Type | Electric Vehicle ICE Vehicle CNG/LPG Vehicle Micro-mobility Vehicle |

||

| by Business Model | Business-to-Consumer (B2C) Business-to-Business (B2B) Peer-to-Peer (P2P) |

||

| by Platform | Web-based App-based Web & App Based |

||

Ride Sharing Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Key Players / Competitors Profiles Covered in Brief in Global Ride Sharing Market Report in Strategic Perspective:

- Uber Technologies Inc.

- Lyft, Inc.

- DiDi Global Inc.

- Grab

- ANI Technologies Pvt. Ltd. (Ola)

- Bolt Technology OÜ

- Gett

- BlaBlaCar (Comuto SA)

- Cabify España S.L.U.

- Careem Networks FZ LLC

- Splend

- GoTo Group (Gojek)

- Yandex Go

- inDrive

- Wheely

- Scoop Technologies

- Rapido Transportation

- Curb Mobility LLC

- Kakao Mobility

- Zimride

- car2go Group GmbH (SHARE NOW)

- Maxim

- Ryde Group Ltd.

- Heetch

- Beat Mobility SA