PDMS Market Size by Type, Form, End-Use Industry, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

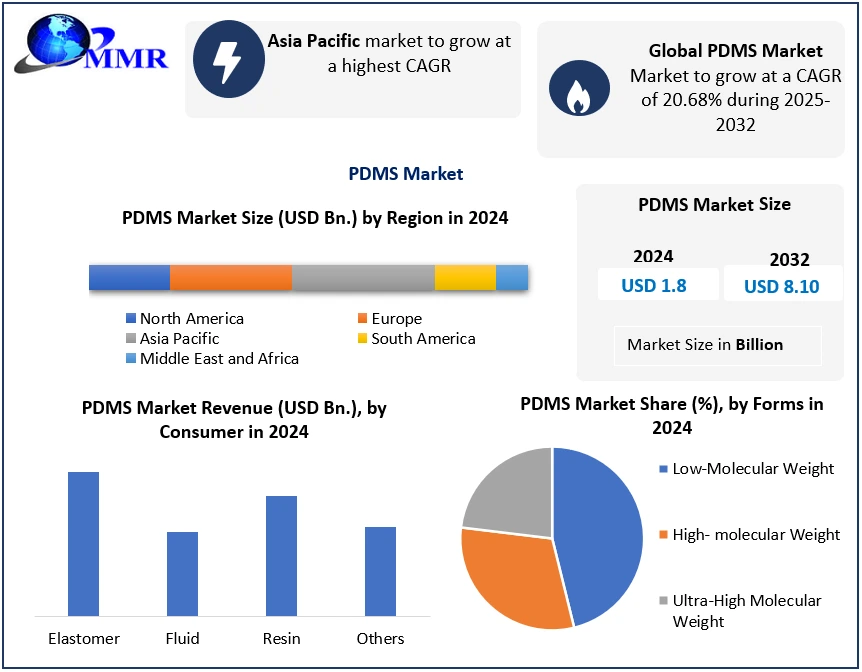

The Global PDMS Market size was valued at USD 1.8 Bn. in 2024, and the total Global PDMS Market revenue is expected to grow by 20.68% from 2024 to 2032, reaching nearly USD 8.10 Bn.

PDMS Market Overview:

The Polydimethylsiloxane (PDMS) market centers around a flexible, soft silicone polymer known for its outstanding heat resistance, water repellency, and biocompatibility. PDMS maintains thermal stability across a wide temperature range—from -40°F to 300°F—making it one of the few silicone-based materials suitable for extreme conditions. These properties enable its use in various high-performance applications, particularly where durability and safety are critical.

The PDMS Market serves diverse sectors, including medical devices, electronics, automotive, and coatings. In the healthcare industry, PDMS is widely used in implants, catheters, contact lenses, and wound care products due to its excellent biocompatibility and non-toxic nature. In electronics and electric vehicles (EVs), PDMS plays a crucial role in thermal management systems, flexible circuits, and insulation materials, addressing the demand for reliable, heat-resistant components.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Demand across the PDMS Market is currently led by the healthcare sector, which accounts for approximately 35% of total consumption. Electronics follow closely at 28%, and EV applications represent around 22% of the market, particularly driven by the need for advanced thermal solutions in battery systems. Additionally, the cosmetics sector—where PDMS is used as dimethicone—and the green energy sector are emerging as fast-growing market segments with increasing relevance.

In terms of supply chain dynamics, the PDMS Market is dominated by major chemical manufacturers. Key players include Dow Inc. (U.S.), Shin-Etsu Chemical (Japan), and Wacker Chemie (Germany), with additional contributions from Elkem ASA (Norway), Momentive (U.S.), and KCC Corporation (South Korea). The largest PDMS manufacturing capacities are concentrated in the Asia-Pacific region, particularly in China and Japan, making the region a pivotal hub for global supply and demand.

Looking ahead, the PDMS Market is expected to experience sustained growth, driven by increasing demand for high-performance materials in medical devices, flexible electronics, and electric vehicles. With its unique combination of biocompatibility, heat resistance, and versatility, PDMS will continue to be a critical material in a wide range of advanced industrial and consumer applications.

PDMS Market Dynamics:

Expanding applications in healthcare and medical devices to drive the PDMS Market Growth

The global polydimethylsiloxane (PDMS) market is rapidly increasing with robust growth primarily from its growth in healthcare and medical devices. PDMS is a silicone-based polymer that is biocompatible, chemically inert and flexible, making it a very versatile and useful material in applications, such as (but not limited to) biomedical implants, wound dressings, catheters, and drug delivery systems. The electronics industry is also a major player in the growth of the PDMS market by using PDMS in things like semiconductor manufacture and battery insulation in most electric vehicle (EV) batteries and flexible displays in smartphones & wearables. The demand for "sustainably sourced" and "bio-based" silicone has also seen an increased demand in cosmetics, personal care, and renewable energy sectors in the PDMS market. In addition to these features, the blockbuster rise of microfluidics in in-vitro and on-site diagnostics after COVID, especially now that PDMS has become a preferred material for lab-on-a-chip devices, has only added to PDMS's attractiveness and breadth of uses: it is cheap, completely inert, able to be completely sterilized, and economically durable.

Fluctuating prices of raw materials to restrain the PDMS Market

Although the PDMS market has expanded, there are numerous challenges. Price volatility of raw materials, like silicon metal and methanol, can affect production pricing and profit margins. Regulatory requirements, such as those from the FDA for medical-grade PDMS and REACH in Europe, increase compliance costs and delay product approvals. Competition from alternative materials, for example, thermoplastic elastomers (TPEs), threatens to enter cost-sensitive markets. Moreover, geopolitical issues that create supply chain issues have altered the availability of silicone. Additionally, historical scepticism regarding silicone safety (e.g., breast implant controversies) continues to impact consumer and regulatory perceptions of silicone, especially in medical applications.

EVs, Smart Devices, and Sustainable Innovation to Create PDMS Market Opportunities

The rise of electric vehicles (EVs) is a major opportunity for both manufacturers and developers of PDMS because it is essential for battery sealing, thermal management, and gaskets. The increasing use of smart wearables and IoT devices is also driving innovation in terms of flexible, stretchable, PDMS-based sensors. There are also developing markets (especially Asia-Pacific) that are industrializing rapidly in the pharmaceuticals, electronics, and automotive sectors will create demands for PDMS. New developments in bio-compatible and self-healing silicones are opening up different possibilities in medical implants and industrial coatings. Additionally, with the push for green chemistry, many producers are developing PDMS variants and alternatives with a lower impact on the environment.

High Purity Costs, Regulatory Hurdles, and Competitive Pressures to Create PDMS Market Challenges

The cost of high-purity PDMS continues to prevent acceptance in small to medium enterprises. Also, the trading of counterfeit and low-grade silicone in a number of emerging markets threatens brand reputation. Technology and science evolve quickly and not only create tension for manufacturers to reformulate, but also require manufacturers to continually allocate resources into product R&D to match or differentiate from competitors. Lastly, regional limitations in many areas restrict how a product can be marketed worldwide, as companies are required to create new or alter a product formulation to meet compliance for every region.

PDMS Market Segment Analysis:

The PDMS Market is segmented by Type, Form, and End-Use Industry.

Based on the Type, the PDMS market is segmented into low-molecular-weight, high-molecular-weight, and Ultra-High molecular-weight. The low-molecular-weight segment is expected to hold the largest market share of xx% by 2032. Laboratory bath fluids, heat transfer fluids, dielectric fluids, low viscosity damping fluids, low viscosity hydraulic fluids, and other applications use low-molecular-weight PDMS. The market for PDMS is estimated to rise due to the high growth rate of the building and construction, as well as the automotive industries, in developing nations in Asia Pacific, South America, the Middle East, and Africa.

Based on the Form, the PDMS market is segmented into Elastomer, Fluid, Resin, and Others. Elastomer segment is expected to grow rapidly at a CAGR of xx% during the forecast period 2025-2032. Personal care items, medical devices, microfluidic devices, and other industrial applications all use PDMS elastomers. It is the most popular form of PDMS due to its elasticity, transparency, durability, and long shelf life. The demand for PDMS elastomers is estimated to rise as the healthcare, personal care, cosmetics, and other industries increase. As a result, the PDMS market is expected to be driven by rising elastomer demand over the forecast period.

Based on the End-Use Industry, the PDMS Market is segmented into Industrial Process, Building & Construction, Household & Personal Care, Electrical & Electronics, Transportation, Healthcare, and Others. The Healthcare Industry segment is expected to grow rapidly at a CAGR of xx% during the forecast period 2025-2032. Polydimethylsiloxane (PDMS), commonly known as dimethylpolysiloxane or dimethicone, is a kind of polydimethylsiloxane. The silicon-based organic polymer PDMS is the most widely utilised. PDMS is commonly utilised in the healthcare industry for various biological and medical applications, including microfluidics, implants, catheters, punctual plugs, valves, orthopaedics, and micro gaskets, among others. It also acts as a barrier to liquids like water, blood, and urine, while allowing gaseous elements and molecules like nitrogen, oxygen, hydrogen, and carbon dioxide to pass through.

PDMS is also utilised in rubber items, such as sanitary gaskets, that are suited for repeated use in biological research since it is optically clear, non-toxic, and non-flammable, and it fits the standards of FDA CFR 177.2600. Polydimethylsiloxane also passes the USP Class VI implantation and acute systemic toxicity testing standards.

Moreover, countries like China, India, Germany, and the United States, among others, enjoy significant market leadership positions in the healthcare sector. Various countries are investing in mobile healthcare facilities as a result of demographic shifts and digitalization, which is providing a platform for the development of the healthcare sector in various countries.

PDMS Market Regional Insights:

The Asia Pacific region is expected to dominate the PDMS Market during the forecast period 2025-2032. The Asia Pacific region is expected to hold the largest market share of xx% by 2032. Because of rising consumer spending and income levels, the construction, automotive, personal care & consumer products, and electronic & electrical industries in the region are expected to see increased demand for PDMS. In the construction business, PDMS is extensively utilised as adhesives, sealants, and coatings. In domestic and personal items, PDMS is a necessary raw ingredient.

The objective of the report is to present a comprehensive analysis of the Global PDMS Market to the stakeholders in the industry. The past and current status of the industry, with the forecasted market size and trends, are presented in the report, with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that include market leaders, followers, and new entrants.

PORTER, PESTEL analysis with the potential impact of micro-economic factors of the market has been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analysed, which will give a clear futuristic view of the industry to the decision-makers.

The reports also help in understanding the Global PDMS Market dynamics and structure by analyzing the market segments and projecting the Global PDMS Market size. Clear representation of competitive analysis of key players by Distribution Channel, price, financial position, product portfolio, growth strategies, and regional presence in the PDMS Market makes the report an investor’s guide.

PDMS Market Competitive Landscape:

The PDMS market represents a global market that is very competitive, with several large companies using various strategies to solidify their position. Dow Inc. (United States) and Shin-Etsu Chemical (Japan) are doing well in the higher end of the market on the growth trajectory of being technology leaders in medical-grade PDMS and electronics-grade PDMS for EV battery insulation and bendable OLEDs. Wacker Chemie (Germany) is developing a sustainable PDMS niche for the more specialized markets in cosmetics and renewable energy.

Elkem ASA (Norway) and Momentive (United States) seem to be targeting industrial grade and pricing strategy in markets with high competition and on price formulating in developing markets. In China (e.g. Bluestar Silicones, now owned by Sinochem) the manufacturers are scaling production of commodity PDMS markets, and gaining the ability to create price competition in PDMS.

Differentiating in these growing commodity and specialty PDMS markets seems to be becoming R&D investments in enhancing applications, and this development indicates that the biggest players are spending on average of between 8-12% of revenues on R&D while managing their supply chain or logistical concerns and responding to each region's regulatory standards and evolving legislative ecosystem. This competitive state of PDMS indicates a greater segmentation in the global PDMS market, where companies are required to allocate their spending to R&D on tailored applications.

PDMS Market Key Developments:

• February 2025 – Dow Inc. (U.S.) introduced SILASTIC™ AI-9000, a next-generation medical-grade PDMS utilizing AI-based curing optimization for implantable devices. SILASTIC™ AI-9000 will help organizations decrease their production time by 30% and increase biocompatibility for safety in long-term applications.

• March 2025 – Shin-Etsu Chemical (Japan) introduced KE-2095 Ultra-Pure PDMS, designed for semiconductor and electric vehicle battery insulation; this formulation limited ionic contamination to <0.1 ppb (as characterized by the electronics industry), as required by the strict helium demand for new products.

• April 2025 – Wacker Chemie (Germany) introduced ELASTOSIL® Eco, the first carbon-neutral PDMS for cosmetics and renewable energy applications. This material was uniquely made using 100% renewable silicones (followed by biodegradable additives) across every manufacturing process.

• May 2025 – Momentive (U.S.) expanded its IMPRESS™ series for self-healing coatings of PDMS for industrial wearables. The ability for the PDMS to automatically repair the micro-tears sustained in adverse conditions (e.g., oil & gas, aerospace) is a significant engineering breakthrough.

PDMS Market Key Trends

| Category | Key Trend | Example | Market Impact |

| AI & Advanced Manufacturing | AI-driven curing and quality optimization for high-precision PDMS | Dow Inc.’s SILASTIC AI-9000 (Feb 2025) with AI-curing for medical implants | Reduces production defects by 25%; accelerates adoption in implantable devices. |

| Sustainability & Bio-Based PDMS | Shift toward carbon-neutral and renewable silicones | Wacker Chemie’s ELASTOSIL Eco (Apr 2025), made with 100% renewable feedstocks | Meets ESG goals in cosmetics and green energy sectors. |

| Ultra-Pure PDMS for Electronics | Demand for contamination-free silicones in chips/EVs | Shin-Etsu’s KE-2095 Ultra-Pure PDMS (Mar 2025) (<0.1 ppb ionic impurities) | Critical for next-gen semiconductors and EV battery insulation. |

| Cost-Competitive Commoditization | Localized, low-cost PDMS for emerging markets | Bluestar Silicones’ Bluesil PharmaFlow (Jun 2025) for mass-market pharma packaging | Pressures on global players’ margins in Asia. |

| Self-Healing & Smart Materials | PDMS with autonomous repair for harsh environments | Momentive’s IMPRESS Self-Healing Coatings (May 2025) for industrial wearables | Extends product lifespan in oil/gas and aerospace applications. |

PDMS Market Scope: Inquiry Before Buying

| PDMS Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 1.8 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 20.68% | Market Size in 2032: | USD 8.10 Bn. |

| Segments Covered: | by Type | Low-Molecular Weight High-Molecular Weight Ultra-High Molecular Weight |

|

| by Form | Elastomer Fluid Resin Others |

||

| by End-Use Industry | Industrial Process Building & Construction Household & Personal Care Electrical & Electronics Transportation Healthcare Others |

||

PDMS Market, by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, ASEAN, Indonesia, Philippines, Malaysia, Vietnam, Thailand, ASEAN, Rest of Asia Pacific)

Middle East & Africa (South Africa, GCC, Nigeria, Rest of ME&A)

South America (Brazil, Argentina, Rest of South America)

PDMS Market, Key Players

North America

1. DowDuPont Inc. (USA)

2. Avantor, Inc. (USA)

3. Momentive (USA)

4. Sigma Aldrich Corp. (USA)

Europe

1. Wacker Chemie AG (Germany)

2. Elkem ASA (Norway)

3. CHT Group (Germany)

4. Alfa Aesar (UK)

Asia-Pacific

1. Shin-Etsu Chemical Co., Ltd. (Japan)

2. KCC Corporation (South Korea)

3. Dongyue Group Limited (China)

4. Zhonghao Chenguang Research Institute (China)

5. Bluestar Silicones (China, acquired by Sinochem)

6. Hubei Xin Sihai Chemical Co. (China)

7. Jinan Haohua Industry Co., Ltd. (China)

8. TCI Tokyo Chemical Industry Co. (Japan)

Frequently Asked Questions:

1. Which region has the largest share in the Global PDMS Market?

Ans: The Asia Pacific region held the highest share in 2024.

2. What is the growth rate of the Global PDMS Market?

Ans: The Global PDMS Market is growing at a CAGR of 20.68% during the forecasting period 2025-2032

3. What is the scope of the Global PDMS Market report?

Ans: Global PDMS Market report helps with the PESTEL, Porter's, COVID-19 Impact analysis, Recommendations for Investors & Leaders, and market estimation of the forecast period.

4. Who are the key players in the Global PDMS Market?

Ans: The important key players in the Global PDMS Market are – Dow DuPont Inc., Shin-Etsu Chemical Co., Ltd., Wacker Chemie AG, Avantor, Inc., Elkem ASA, KCC Corporation, Dongyue Group Limited, Alfa Aesar, CHT Group, Zhonghao Chenguang Research Institute of Chemical Industry, Bluestar Silicones, Hubei Xin Sihai Chemical Co., Momentive, Sigma Aldrich Corp., Jinan Haohua Industry Co., Ltd., TCI Tokyo Chemical Industry Co.

5. What is the study period of the PDMS Market?

Ans: The Global PDMS Market is studied from 2025 to 2032.