Parcel Delivery Market Size by Delivery Mode, Destination, Customer Type, Delivery Type, Industry Product, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2032

Overview

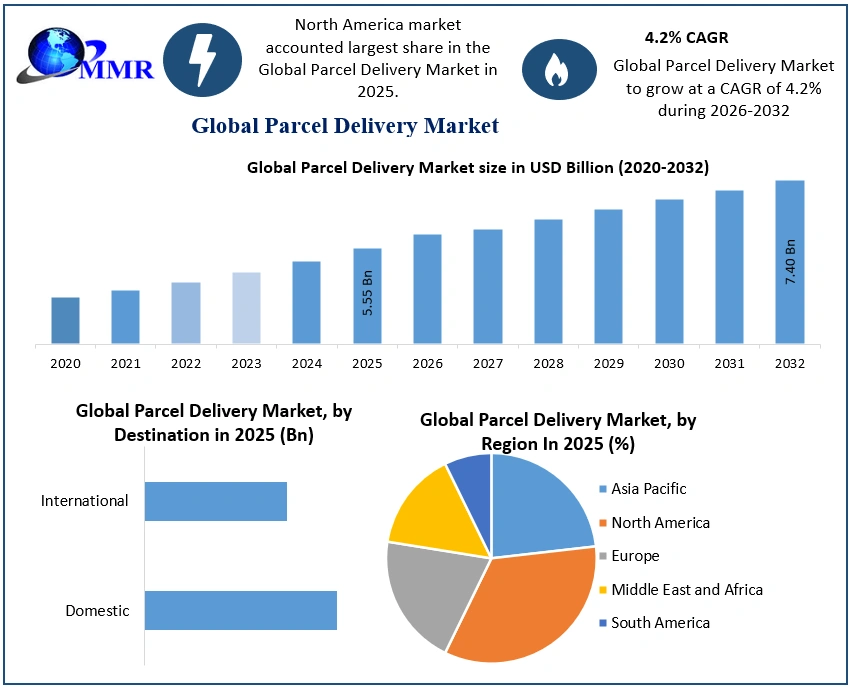

The Parcel Delivery Market size was valued at USD 5.55 Billion in 2025 and the total Parcel Delivery revenue is expected to grow at a CAGR of 4.2% from 2025 to 2032, reaching nearly USD 7.40 Billion by 2032.

Parcel Delivery Market Overview:

A package is described as products or objects wrapped in paper, sealed in an envelope, or placed in a box, and parcel delivery is the process of transporting a parcel to a certain location by road, rail, or air. The parcel delivery market has been driven by increased internet penetration and the rise of the e-commerce industry. The global parcel delivery market is expected to grow throughout the forecast period with CAGR of approximately 4.2%, as internet penetration and client purchasing preferences change.

To know about the Research Methodology :- Request Free Sample Report

Parcel Delivery Market Dynamics:

One of the primary drivers fuelling the expansion of the parcel delivery industry is the rising e-commerce sector, as well as the growing cross-border trade. The acceptance of international trade and B2C shipments has increased as cross-border trade routes have developed, particularly in emerging economies. Furthermore, the growing demand of consumers for purchasing online through various e-commerce platforms is boosting the market growth. To distribute their products across national and international borders, e-commerce stores work with courier service providers.

Moreover, technological improvements, such as the use of digital technology with crowd-sourced delivery models, are also boosting the market's prospects. These technologies help service providers improve their overall operating efficiency and efficiently meet the needs of their clients. Other factors such as fast urbanization, expanding consumer expenditure capacity, and considerable industrial sector expansion are expected to propel the market even higher during the forecast period.

With half of Asia-Pacific internet buyers making cross-border transactions, merchants are focusing their efforts on gaining a thorough understanding of procedures such as duty collection, customs clearance, and other minefields. Customers' expectations of what they can have are rising, and technology is expanding their options for how those items are delivered. However, previous research has shown that customers are not only becoming more demanding, but they are also becoming more cost-conscious, with a low willingness to pay for increased convenience. Autonomous delivery vehicles (ADVs) will be the dominating technology in last-mile delivery in the medium future, having the ability to both save time and money for customers.

Despite the rather large technological leap that is required, incumbent CEP players are still well-positioned to control the bulk of parcel volumes (75 to 80 percent of the 2025 volume) in deferred, in B2B, and—to a lesser extent—in same-day delivery. The capital-intensive nature of sorting and full-scale logistics networks, the almost-mandatory nationwide service offer, significant economies of scale, and the required access to the customer are immense barriers to entry for new players and will help traditional players hold on to dominance in the core. However, several extremely large retailers may join traditional last-mile delivery (that is, deferred delivery) in certain high-density locations to obtain control of the consumer touchpoint and to build synergies with their same-day networks.

Significant cost savings will result in a multibillion-euro redistribution of value in both the core and new parts of the industry. Cost-effective autonomous technology has the potential to save $20 billion to $25 billion per year in industrialized economies. The size of the value redistribution is enormous, far outstripping the aggregate profit pool of CEP participants in industrialised countries today. Furthermore, rather than the growing same-day and instant markets, the lion's share of value redistribution ($15 billion to $20 billion) in the last-mile ecosystem is likely to occur in today's core market. The value will most likely be shared among CEP participants, autonomous-vehicles developers, and others.

CV players will likely play a bigger role in last-mile delivery in the future because they are not only well-positioned to operate autonomous delivery fleets (fleet management), but they can also use their routing expertise. Because they will continue to compete from a position of strength in the core business, CEP players are well-positioned to dominate the fundamental steps—capacity management, tour optimization and planning, and sorting. Physical management of the parcels also grants CEP participants access to and control over the data connected with them, which is a critical input for process excellence.

Parcel Delivery Market Technological Improvement Trends:

The Delivery sector has gone through various innovation stages as a result of the world's expanding digitization, including the adoption of GPS and RFID technologies to track cars and goods. While the USPS continues to be concerned about the widespread use of electronic mail, courier businesses continue to benefit from rising online retail sales: Physical things are increasingly being purchased online by both consumers and businesses, and these items must be delivered. Furthermore, parcel processing devices capable of sorting 20,000 shipments in an hour have increased the industry's efficiency. The level of monitoring Internet-connected courier fleet trucks has also improved thanks to satellite computer systems.

Parcel Delivery Market Technological Roadmap:

The first wave of technology is projected to alter last-mile delivery, including electric vehicles (EVs) and the rising availability of unattended delivery technologies. These technologies are market-ready and scalable, and each one contributes to cost-effectiveness, customer ease, or regulatory compliance. As cities tighten their pollution regulations, it's only natural that EV deployment in last-mile delivery will be one of the first technologies to gain traction.

Large, semiautonomous delivery vehicles that follow parcel-delivery employees are predicted to be the next trend followed by parcel-delivery companies in three to five years. By reducing the time required to drive and park vans, this first step toward full automation is expected to benefit delivery personnel and enhance production. ADVs will also represent the third wave of widespread tech-enabled parcel delivery in five to ten years when they will likely not need to be accompanied by human delivery employees at all.

Robots are planned to deliver products directly to clients' front doors by 2032. This technology adds significant value to the customer experience by allowing robots to handle the "final ten yards" of delivery. Pilots for robot delivery are currently underway. However, because this technology is currently expensive, these alternatives are unlikely to be widely adopted.

B2B Segment is leading the market:

The B2B (Business-to-Business) segment is dominating the Parcel Delivery market and is anticipated to remain so for the forecast period of . The parcel delivery market is expected to grow as B2B parcel drop numbers per recipient and special delivery requirements increase. The B2C category is being driven by the rise of e-commerce and online grocery stores; B2C parcel delivery is predicted to increase at 7% Y-O-Y in. Government rules, gasoline prices, and transportation are the biggest roadblocks to the B2C segment's growth and are also considered key challenges for prominent players in the market.

Parcel Delivery Market Regional Insights:

UPS is leading the U.S. parcel market:

North America dominates the market with a total service share of 45%. Mail that is too heavy for regular letter delivery is delivered by parcel service companies. According to International Post Corporation, United Parcel Service is the largest and most often utilized package delivery firm in the United States. UPS is expected to produce around $84.6 billion in sales in 2025. Express services, which are accessible both domestically and internationally, provide speedier mail delivery. Priority Mail Express is the accelerated domestic mail delivery service provided by the US Postal Service in the United States. Above mentioned factors related to major players in the market are considered to drive the parcel delivery market.

Parcel shipping is booming on account of the e-commerce rise:

E-commerce growth and the COVID-19 pandemic are fueling the parcel shipping market, as consumers are ordering more online. This led to a 37 percent growth in volume, with 20 billion parcels being shipped in the United States, and parcel revenue increasing by 29 percent to 171 billion U.S. dollars in.

Asia Pacific is expected to register the highest CAGR during the forecast period. Moreover, increasing penetration of E-commerce and business developments in the region are the factors driving the growth of the APAC region. Besides, rising living standards, increasing disposable income in the regions of India, Japan, China, and ASEAN countries are driving the growth pattern of the region. Moreover, as key market players are setting up their bases in the APAC region in the hope of futuristic gains, the market is surely expected to rise with the booming CAGR rate. China is leading the APAC region with the highest market share of 50% owing to booming E-commerce in the Chinese region and boosting the manufacturing sector of China.

The objective of the report is to present a comprehensive analysis of the Parcel Delivery Market to the stakeholders in the industry. The past and current status of the industry with the forecasted Market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that include Market leaders, followers, and new entrants.

PORTER, PESTEL analysis with the potential impact of micro-economic factors of the Market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the industry to the decision-makers.

The report also helps in understanding the Parcel Delivery Market dynamics, structure by analyzing the Market segments and project the Parcel Delivery Market size. Clear representation of competitive analysis of key players by Type, price, financial position, Type portfolio, growth strategies, and regional presence in the Parcel Delivery Market make the report investor’s guide.

Parcel Delivery Market Scope: Inquire before buying

| Global Parcel Delivery Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 5.55 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 4.2% | Market Size in 2032: | USD 7.40 Bn. |

| Segments Covered: | By Delivery Mode | Ground Freight Air Freight Sea Freight Rail Freight |

|

| By Destination | Domestic International |

||

| By Customer Type | B2B B2C C2C |

||

| By Delivery Type | Express Delivery Standard Courier Services Others |

||

| By Industry Product | Consumer Packaged Goods Telecom and Electronics Fashion and Apparel Food and Beverage Automotive Pharmaceutical Others |

||

Parcel Delivery Market, by region

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

North America (United States, Canada and Mexico)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Parcel Delivery Market, Key Players are:

North America

1. Bell and Howell LLC (USA)

2. Amazon.com, Inc. (USA)

3. United Parcel Service, Inc. (USA)

4. FedEx Corporation (USA)

Asia Pacific

5. Smartbox Ecommerce Solutions Pvt. Ltd. (India)

6. SF Express Co., Ltd. (China)

7. CJ Logistics Corporation (South Korea)

8. J&T Express (Indonesia)

Europe

9. Cleveron AS (Estonia)

10. KEBA AG (Austria)

11. ByBox Holdings Ltd. (United Kingdom)

12. InPost S.A. (Poland)

13. Deutsche Post DHL Group (Germany)

Middle East and Africa

14. Aramex PJSC (United Arab Emirates)

15. Oman Post (Oman)

16. Jumia Technologies AG (Nigeria)

South America

17. Empresa Brasileira de Correios e Telégrafos (Brazil)

18. Jadlog S.A. (Brazil)

FAQ’S:

1) What was the Global Parcel Delivery Market size in 2025?

Ans: The Global Parcel Delivery Market size was USD 5.55 Billion in 2025.

2) Which Business segment is dominating the Parcel Delivery Market?

Answer: B2C segment is dominating the market owing to increasing service offerings by key players to B2C clients and fast delivery offered with considerable schemes.

3) What are the key players in the Parcel Delivery Market?

Answer: Bell and Howell, Cleveron Ltd., TZ Ltd., LLC, KEBA AG, ENGY Company, Neopost Group, ByBox Holdings Ltd., InPost, Smartbox Ecommerce Solutions Pvt. Ltd., Amazon.com, Inc., Deutsche Post DHL Group, United Parcel Service Inc., FedEx Corporation, Aramex PJSC, SF Express (Group) Co. Ltd

4) Which factor acts as the driving factor for the growth of the Parcel Delivery Market?

Answer: One of the primary drivers fuelling the expansion of the parcel delivery industry is the rising e-commerce sector, as well as the growing cross-border trade.

5) What factors are restraining the growth of the Parcel Delivery Market?

Answer: Volatility of E commerce sector and increasing competition in the market are the key factors restraining the market growth.