Global Mining Chemicals Market by Mineral Type, Product Type, Application, and Region - Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2030

Overview

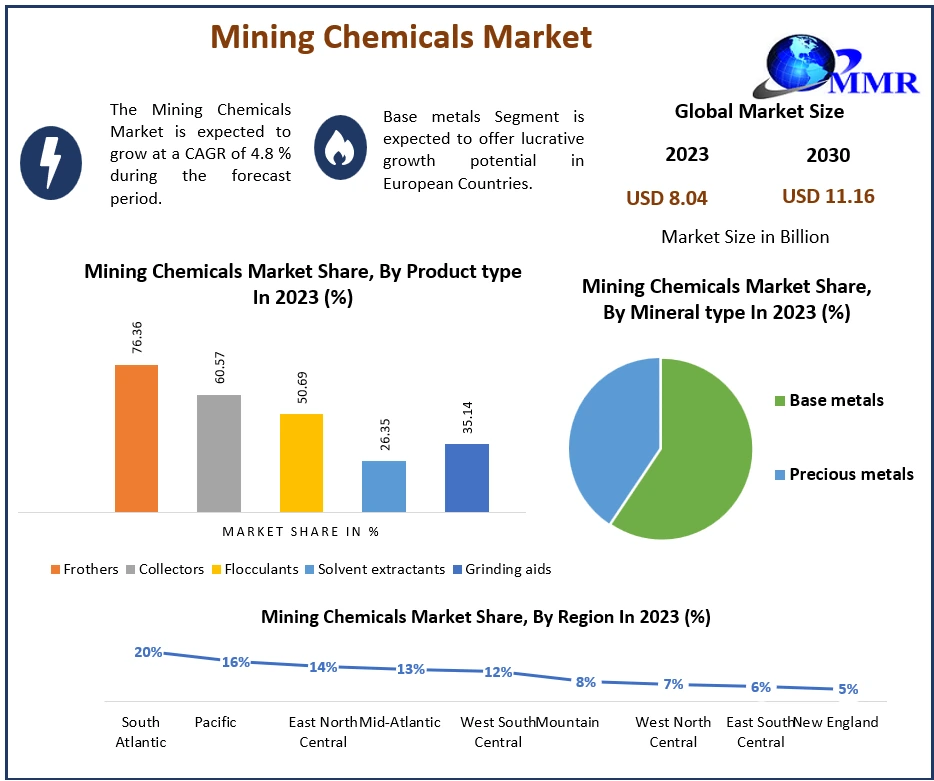

The Mining Chemicals Market size was valued at USD 8.04 Billion in 2023 and the total Mining Chemicals revenue is expected to grow at a CAGR of 4.8 % from 2024 to 2030, reaching nearly USD 11.16 Billion by 2030.

Mining chemicals is range of chemicals used in the mining process to improve productivity and efficiency while ensuring environmental safety. These chemicals aid in the extraction of minerals and metals from ores, enhance the recovery of valuable minerals, and assist in the processing and refining stages. The current mining chemicals market is driven by several factors, including the growing demand for minerals and metals across various industries such as construction, automotive, and electronics, driving increased mining activities globally. Additionally, advancements in technology have led to the development of innovative chemicals that offer enhanced efficiency in extracting minerals and metals, boosting the mining chemicals market's growth.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Recent developments in the mining chemicals sector involve key players introducing environmentally sustainable and efficient solutions. For instance, companies have been focusing on developing eco-friendly chemicals that minimize the environmental impact of mining activities while ensuring high mineral recovery rates. Additionally, innovations in reagents and additives are aimed at improving flotation processes, allowing better extraction of valuable minerals and reducing energy consumption in processing. These developments align with the industry's pursuit of greener and more sustainable mining practices, driven by stringent environmental regulations and a growing emphasis on corporate social responsibility. As mining companies aim for more efficient, cost-effective, and environmentally conscious practices, the focus on the development and adoption of advanced mining chemicals continues to shape the mining chemicals market landscape.

Mining Chemicals Market Dynamics:

Increasing use of chemicals in mineral processing and need for specialty chemicals in mining processes boosting the growth of Mining Chemicals Market

Rising Technological advancements boosting the market growth. For example bioleaching, revolutionize mineral extraction by utilizing microorganisms to extract metals from ores. BacTech Environmental Corporation's application of bioleaching in recovering metals from mine tailings significantly enhances extraction efficiency while reducing environmental impact. The surging demand for precious metals like gold and silver propels the need for effective extraction processes, leading to the utilization of specialty chemicals such as cyanide due to its exceptional efficiency in dissolving gold from ores.

Growing exploration activities in untapped regions propel the demand for mining chemicals. Companies like Clariant offer exploration solutions involving frothers and collectors, aiding mineral identification and extraction. Stringent regulations prompt mining companies to adopt eco-friendly chemical alternatives. For instance, the shift from mercury-based gold extraction methods to gravity separation and cyanidation reduces environmental risks. Innovations in grinding aids and frothers, such as BASF's Rheomax technology, enhance mineral recovery, boosting grinding efficiency and throughput in mineral processing plants.

The increased demand for rare earth elements crucial in high-tech industries necessitates specialized chemical usage for efficient extraction. The expansion of mining operations in emerging economies, like Brazil's iron ore mining expansion, drives the need for chemicals like flocculants and depressants to segregate hematite from silica. In response to water scarcity concerns, chemicals aiding in water conservation gain prominence, reducing water usage in processing plants. Mining companies' pursuit of custom chemical formulations tailored to specific mineral types, exemplified by Dow's specialty collectors for complex ores, enhances extraction efficiency and selectivity. As economies grow, the escalated demand for metals and minerals stimulates mining activities, consequently increasing the utilization of chemicals like flotation reagents and grinding aids to augment extraction processes.

High expenses tied to specialized chemicals such as flocculants strain mining profitability, impacting the bottom line and operational sustainability.

The Mining Chemicals Market grapples with numerous constraints impacting its growth and operational dynamics. Stringent environmental regulations curtail the utilization of specific mining chemicals due to their detrimental ecological impact. Notably, cyanide, widely used in gold extraction, faces stringent global regulations, compelling mining entities to explore and adopt safer alternatives to ensure compliance. Additionally, the exorbitant costs associated with specialized mining chemicals, such as flocculants utilized in wastewater treatment, significantly inflate operational expenses, casting a shadow on the overall profitability of mining endeavors.

Supply chain disruptions, exemplified by the COVID-19 pandemic, trigger critical shortages of essential mining chemicals, disrupting mining operations globally. For instance, the scarcity of sulfuric acid, a crucial component in mineral processing, significantly hampers mining activities across various sectors. Health risks to mining workers posed by certain chemicals, such as mercury utilized in gold extraction, raise concerns due to their toxic nature, jeopardizing the well-being of laborers involved in mining processes. The sluggish pace of innovation in developing eco-friendly alternatives further complicates the adoption of safer chemicals in mining operations, hampering the shift away from traditional but more hazardous substances. Regulatory approval processes for new chemicals, demanding rigorous testing and assessment, create substantial delays in their integration into mining operations, hindering the industry's progression towards safer alternatives. Additionally, the volatility in raw material prices, evident in fluctuations in sulfuric acid prices, disrupts accessibility and affordability for mining companies reliant on such chemicals, impacting their operations and costs.

The intricacy of integrating new chemicals into existing mining processes poses significant operational challenges. The introduction of novel chemicals necessitates extensive process reevaluation, potentially leading to disruptions in ongoing operations. Furthermore, chemicals that demand substantial water usage, particularly those involved in processes like froth flotation, amplify water stress in mining regions already facing water scarcity. The industry's resistance to embracing new chemicals and processes, rooted in established practices, impedes the swift transition to greener mining practices, obstructing the industry's evolution toward safer alternatives and sustainable practices.

Mining Chemicals Market Segment Analysis:

Based on Type, the precious metals segment dominated the market in 2023. Precious metals are elements that are considered rare and chemically inert. They’re not abundant in nature, and therefore they have high economic value. Precious are used commonly in jewelry, industrial processes, or very often as investment vehicles. The four primary precious metals are gold, silver, platinum, and palladium. Depending on the application, there are common alloying elements that can be mixed with the main precious metals to improve the properties of the final product.

Based on Application, The Mining Chemical Market data has been bifurcated by product largely into mineral processing, explosives & drilling, water & wastewater treatment and others. The water & wastewater segment dominated the market in 2023. Water & wastewater treatment is crucial to abide by the regulations regarding the use of water and its environmental impact. Water treatment systems are used in several mineral processing plants such as gold, copper, and others. The treatment of water used for processing leads to minimized corrosion & equipment blockage, improved water quality & flow, scaling, and lower chemical costs& dosages. The demand for water treatment in the mining industry is witnessed to grow considerably owing to rising concerns regarding the release of pollutants to natural water sources and the highly acidic nature of the mining water.

Mining Chemicals Market Regional Insights:

Asia Pacific Dominance in the Mining Chemicals Market

Asia Pacific region dominated the Mining Chemicals Market with a revenue share with 36.3% in 2023. This high share is attributed to growing mineral processing activities in countries including India, China, and others which are projected to promote the utilization of the product in the region over the forecast period. China accounts for the largest market share in Asia Pacific as China is the largest producer of coal, gold, and other earth minerals. China has a large number of mines, which are going through improvements such as setting up new sewage treatment plants and the development of sewage and wastewater treatment plants.

Increasing foreign investments in emerging countries of Asia Pacific, including India and China, have contributed to the growth of the mining chemicals industry in the region. India has an abundance of natural reserves of coal, titanium, diamond, bauxite, and limestone. The demand for mining chemicals in Central & South America is majorly driven by an increase in mining and mineral processing activities in countries such as Brazil, Colombia, Argentina, and Chile. The region majorly produces iron ore, copper, and ubiquitous gold. Expanding mining industry can be attributed to the large-scale foreign investments by private companies for exploration activities across the region.

Mining Chemical Industry Developments

March 2023

Solvay and Rio Tinto announced a strategic partnership, to develop new mining chemicals technology. The partnership will focus on the development of new collectors and frothers that are designed to improve the recovery of copper from ore.

April 2022:

BASF launched a new mining chemicals product, Alclar, it is a new type of collector that is designed to improve the recovery of copper from ore.

September 2021

Clariant opened a new technical facility in Brazil exclusively dedicated to developing solutions for tailings management. Clariant’s new Competence Center for Tailings Treatment will develop mining chemicals and technologies to support the industry’s efforts from the heart of Brazil’s mining hub.

Mining Chemicals Market Scope:Inquire before buying

| Global Mining Chemicals Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2023 | Forecast Period: | 2024-2030 |

| Historical Data: | 2018 to 2023 | Market Size in 2023: | US $ 8.04 Bn. |

| Forecast Period 2024 to 2030 CAGR: | 4.8% | Market Size in 2030: | US $ 11.16 Bn. |

| Segments Covered: | by Product type | Frothers Collectors Flocculants Solvent extractants Grinding aids |

|

| by Mineral type | Base metals Precious metals Non-metallic minerals Rare earth metals |

||

| by Application | Mineral processing Water & wastewater treatment Explosives & drilling Others |

||

Mining Chemicals Market, by Region:

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Mining Chemicals Market Key Players:

Major Contributors in the Mining Chemicals Industry in North America:

1. Huntsman Corporation - The Woodlands, Texas, USA

2. Chevron Phillips Chemical Company - The Woodlands, Texas, USA

3. Dow Chemical Company - Midland, Michigan, USA

4. ArrMaz - Mulberry, Florida, USA

5. PQ Corporation - Malvern, Pennsylvania, USA

6. Ashland Global Holdings - Wilmington, Delaware, USA

7. Innospec Inc. - Englewood, Colorado, USA

Leading players in the Europe Mining Chemicals Market:

1. BASF SE - Ludwigshafen, Germany

2. Cytec Industries Inc. (Solvay) - Brussels, Belgium

3. Clariant AG - Muttenz, Switzerland

4. Kemira Oyj - Helsinki, Finland

5. AkzoNobel - Amsterdam, Netherlands

6. Cheminova - Harboøre, Denmark

7. SNF Floerger - Andrézieux-Bouthéon, France

8. Nouryon - Amsterdam, Netherlands

9. Evonik Industries AG - Essen, Germany

10. ProMinent GmbH - Heidelberg, Germany

Key players driving the Asia-Pacific Mining Chemicals Market:

1. .Orica Limited - East Melbourne, Australia

2. Kao Chemicals - Tokyo, Japan

3. IXOM - Melbourne, Australia

FAQs:

1] What Major Key players in the Global Mining Chemicals Market report?

Ans. The important key players in the Global market are – BASF SE (Germany), AkzoNobel N.V. (Netherlends), Clariant AG (Switzerland), Kemira OYJ (Finland), Cytec Industries Inc. (U.S.), The Dow Chemical Company (U.S.), Orica Limited (Australia), Huntsman International LLC (U.S.), ArrMaz Products, L.P. (U.S.), and SNF Floerger (France).

2] Which region is expected to hold the highest share in the Global Mining Chemicals Market?

Ans. North America region is expected to hold the highest share in the Mining Chemicals Market.

3] What is the market size of the Global Mining Chemicals Market by 2030?

Ans. The market size of the Mining Chemicals Market by 2030 is expected to reach US$ 11.16 Billion.

4] What is the forecast period for the Global Mining Chemicals Market?

Ans. The forecast period for the Mining Chemicals Market is 2024-2030.

5] What was the market size of the Global Mining Chemicals Market in 2023?

Ans. The market size of the Mining Chemicals Market in 2023 was valued at US$ 8.04 Billion.