1. Halal Cosmetics Market: Market Introduction

1.1. Executive Summary

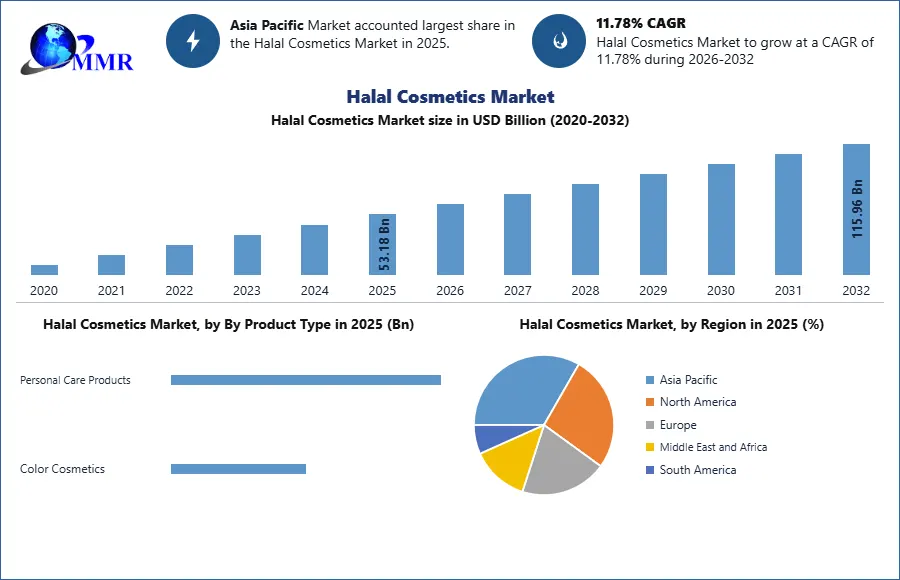

1.2. Market Size (2025) & Forecast (2026-2032),

1.3. Market Size (USD Million) and (Volume in Tons) and Market Share (%) - By Segments, Regions and Country

2. Competitive Landscape

2.1. MMR Competition Matrix

2.2. Competitive Analysis of Key Players

2.3. Key Players Benchmarking

2.3.1 Company Name

2.3.2 Headquarters

2.3.3 Product Portfolio

2.3.4 Total Revenue (2025)

2.3.5 Profit Margin (%)

2.3.6 Market Share (%) by Region (2025)

2.3.7 Sustainability Certifications

2.3.8 Product Innovation Capability

2.3.9 Distribution Reach

2.3.10 R&D Investment (%)

2.3.11 Customer Loyalty & Retention Rate (%)

2.3.12 Raw Material Sourcing Strategy

2.3.13 After-Sales Service & Customer Support

2.3.14 Pricing Flexibility & Promotions

2.3.15 Global Presence

2.4. Market Structure

2.4.1 Market Leaders

2.4.2 Market Followers

2.4.3 Emerging Players

2.5. Mergers and Acquisitions Details

2.6 Kano Model Analysis Of Competitors

2.7. Halal Cosmetics Industry Innovation Landscape:

2.7.1 Brand Tier Trends: Product Portfolio and Certification Strategies Across Skincare, Hair Care, Makeup, Fragrances, and Personal Care (Premium vs. Masstige vs. Mass vs. Indie Halal Brands)

2.7.2 Packaging Tracker: Product Format, Dispensing Systems, and Sustainability Across Liquid, Cream, Gel, Stick, and Powder Halal Cosmetic Products

2.7.3 Evolution of Halal Cosmetic Packaging and Product Formats: Convenience, Precision Application, Hygiene, and Reusability Across Liquid, Cream, Gel, Stick, and Powder Formats

2.7.4 Material Evolution in Halal Cosmetic Packaging: Glass → PET/HDPE → Bioplastics → Bamboo Across Premium, Masstige, and Mass Halal Cosmetic Brands

2.7.5 Post-M&A Innovation Integration: Product Portfolio Expansion Across Product Type, Ingredient Type, and Distribution Channel Strategies

2.8. Halal Cosmetics Market Share Analysis in 2025

2.8.1 Market Share by Brand Tier (Premium, Masstige, Mass) Across Product Types, Product Formats, and Target Audience Segments

2.8.2 Market Share by Product Type (Skincare, Hair Care, Makeup, Fragrances, Personal Care)

2.8.3 Market Share by Product Format (Liquid, Cream, Gel, Stick, Powder)

2.8.4 Market Share of Leading Halal Cosmetic Brands and Regional Dominance Across Distribution Channels

2.8.5 Market Share of Global Beauty Companies vs Dedicated Halal Brands Across Ingredient Types and Target Consumer Segments

2.8.6 Strategic alliances focused on halal-certified natural, organic, and synthetic ingredient sourcing and formulation development

2.8.7 Licensing agreements and technology partnerships supporting innovation across product formats and halal-certified cosmetic formulations

2.9. Brand Positioning and Perception Matrix

2.9.1 Price versus performance mapping across skincare, hair care, makeup, fragrance, and grooming categories

2.9.2 Natural and organic ingredient positioning versus synthetic ingredient performance benchmarking

2.9.3 Accessibility-driven mass halal brands versus premium halal skincare and fragrance specialists

2.9.4 Certification credibility, ingredient transparency, and product safety benchmarking across target consumer groups

2.9.5 Cultural sensitivity, modest beauty positioning, and gender-inclusive grooming trends

2.9.6 Ingredient type transparency and halal certification influence on brand trust

2.9.7 Brand switching behavior and loyalty dynamics across distribution channels and target audiences

2.10. Innovation and Product Launch Intensity

2.10.1 New halal-certified SKU launch frequency across skincare, hair care, makeup, fragrances, and Personal Care

2.10.2 Innovation in product formats including liquid serums, cream-based skincare, gel-based hair care, stick cosmetics, and powder makeup

2.10.3 Natural, organic, and plant-derived ingredient innovation across halal cosmetic product lines

2.10.4 Speed-to-market comparison under halal certification and regulatory approval requirements

2.10.5 Innovation-led revenue contribution and margin expansion across product type and ingredient segments

2.11 Channel Control and Route-to-Market Power

2.11.1 Direct-to-consumer penetration across halal cosmetic brands targeting women, men, children consumers

2.11.2 Retail shelf presence across convenience stores, specialty stores, and supermarkets/hypermarkets

2.11.3 E-commerce marketplace dependency and social commerce penetration across halal cosmetic brands

2.11.4 Urban versus rural distribution reach across offline retail and online channels

2.11.5 Direct sales networks and community-based distribution strategies within halal consumer ecosystems

3. Halal Cosmetics Market Dynamics

3.1. Halal Cosmetics Market Trends

3.2. Halal Cosmetics Market Dynamics

3.2.1 Drivers

3.2.2 Restraints

3.2.3 Opportunities

3.2.4 Challenges

3.3. PORTER’s Five Forces Analysis

3.4. PESTLE Analysis

3.5. Key Opinion Leader Analysis

3.6. Government Schemes in Halal Cosmetics Market

4. Pricing and Profitability Analysis (2025)

4.1 Price Analysis by Product Type (2020–2025)

4.2 Cost Structure Analysis (Halal-certified raw materials, audits, documentation, packaging, branding, testing)

4.3 Margin Analysis by Channel and Region (D2C vs retail vs pharmacy vs marketplace)

4.4 Impact of Raw Material Price Volatility (certified surfactants/emulsifiers, actives, packaging components)

4.5 Private Label vs Branded Price Competitiveness (mass essentials vs premium clinically-positioned halal skincare)

5. Innovation and Product Development Trends (2025)

5.1 Advancement in High-Performance and Clinically-Backed Ingredients (niacinamide, ceramides, peptides, retinoids, AHAs/BHAs—halal-compliant sourcing)

5.2 Emergence of Hybrid Cosmetics Combining Skincare and Aesthetic Benefits (tinted SPF, serum foundations, lip oils with actives)

5.3 Acceleration of Personalized Beauty through AI and Data-Driven Formulation (skin analysis, routine engines within certified ingredient libraries)

5.4 Integration of Augmented Reality and Connected Devices in Product Experience (AR try-on, shade matching, smart skincare tools)

5.5 Expansion of Biotechnological Solutions for Sustainable Ingredient Sourcing (fermentation-derived, bio-based actives to reduce animal-origin risk)

5.6 Rise of Waterless and Minimalist Formulations for Environmental Efficiency (sticks, balms, powders; short INCI “halal + clean” positioning)

6. Consumer Insights and Behavioral Analysis (2025)

6.1 Evolving Beauty and Personal Care Routines Across Demographics (routine-based skincare adoption in Muslim-majority + diaspora markets)

6.2 Gender-Based Usage Patterns and Unisex Product Adoption Trends (men’s grooming, beard/scalp care; unisex personal care growth)

6.3 Increasing Demand for Natural, Vegan, Cruelty-Free, and Ethical Brands (values-stacking: halal + ethical + clean)

6.4 Consumer Perception of Brand Value, Pricing, and Ingredient Transparency (logo trust, certifier recognition, ingredient origin clarity)

6.5 Digital Behavior: Role of Influencers, Reviews, and User-Generated Content (halal beauty creators, routine education, UGC trust signals)

6.6 Channel Preferences and Omnichannel Buying Behavior (discover online-buy offline; D2C in diaspora; pharmacy trust channels)

6.7 Regional and Cultural Influences on Cosmetic Choices (GCC premiumization; SEA certification sensitivity; EU/NA clean-halal niche)

7. Packaging Dynamics and Sustainability Trends in Halal Cosmetics

7.1 Role of Packaging in Consumer Purchase Decisions and Brand Differentiation (certification visibility, authenticity cues)

7.2 Shift Toward Sustainable, Recyclable, and Refillable Packaging Solutions (mono-materials, refills, reduced secondary packs)

7.3 Innovation in Design, Dispensing Systems, and Material Science (airless pumps, droppers for actives, stick formats)

7.4 Smart and Connected Packaging: Authentication, Tracking, and Engagement (QR-based certificate verification, batch traceability)

7.5 Regional Regulatory Compliance for Cosmetic Packaging Materials (EU packaging waste/EPR, material migration compliance)

7.6 Packaging Preferences by Product Type and Consumer Segment (premium skincare packs vs mass personal care formats)

8. Supply Chain and Sourcing Strategy

8.1 End-to-End Supply Chain Overview: From Raw Materials to Distribution (identity preservation, segregation, validated cleaning)

8.2 Global Sourcing Strategies for Key Ingredients and Packaging Components (dual sourcing, certified supplier networks)

8.3 Manufacturing and Private Label Production Hubs by Region (SEA and GCC halal-centric hubs; EU compliance-grade CMOs)

8.4 Supplier Selection, Risk Management, and Strategic Partnerships (audit readiness, certificate validity, strategic certifier ties)

8.5 Traceability, Ethical Sourcing, and Compliance with Sustainability Mandates (batch documentation, ESG-linked sourcing)

8.6 Supply Chain Optimization through Digitization, AI, and Inventory Automation (certificate tracking, COA automation, QC digitization)

9. Global Trade and Import–Export Analysis in 2025

9.1 Global Trade Flows of Halal Cosmetics: Key Importing and Exporting Countries (GCC import demand, SEA export ecosystems, EU/NA diaspora flows)

9.2 Cross-Border E-Commerce and Direct-to-Consumer International Sales (marketplace-led expansion, compliance/labeling constraints)

9.3 Trade Dependencies for Raw Materials, Packaging Components, and Actives (specialty surfactants, emulsifiers, pumps/applicators)

9.4 Impact of Tariffs, Free Trade Agreements, and Customs Regulations (customs delays, labeling audits, FTA advantages)

9.5 Export Opportunities in Emerging Markets and High-Growth Regions (GCC premium, SEA mass/masstige, EU/NA clean-halal niches)

10. Usage Landscape and Comparative Adoption

10.1 Adoption Trends Across Product Categories (skincare, personal care lead; makeup accelerating with certified shade expansion)

10.2 Regional and Cultural Variations in Cosmetics Usage (modest makeup looks, alcohol-free fragrance preferences)

10.3 Usage Frequency and Product Layering Behaviors by Age Group (multi-step skincare, SPF routines, reapplication behavior gaps)

10.4 Influence of Climate, Lifestyle, and Income on Product Adoption (hot/humid lightweight gels; dry climates barrier repair)

10.5 Consumer Loyalty, Repurchase Rates, and Multi-Brand Usage Habits (high repurchase essentials; multi-brand makeup usage)

11. Visual Market Mapping and Customer Targeting

11.1 Brand Tier Positioning and Product Format Mapping (certification strength vs price tier vs format innovation)

11.2 Adoption Trends by Brand Tier (mass essentials; masstige routine skincare; premium clinical halal + fragrance)

11.3 Clean Beauty and Indie Brand Penetration Across Key Markets (D2C-led, influencer-driven education markets)

11.4 Customer Segmentation by Brand Category and Price Sensitivity (faith-driven strict halal; ethical-stack buyers; sensitive-skin safety seekers)

11.5 Opportunity Mapping by Region, Demographics, and Application Format (whitespace: derm-grade halal acne/rosacea, inclusive shade halal makeup)

11.6 Product Category Focus: Skincare vs. Color Cosmetics Brand Distribution (skincare trust-led dominance; makeup growth via performance + inclusivity)

11.7 Emerging Format Preferences (droppers, sticks, hybrid skincare-makeup; refillables) by Tier and Region

12. Halal Ingredient Integrity and Traceability Systems

12.1 Halal supply chain verification mechanisms from raw material sourcing to finished product distribution

12.2 Ingredient traceability systems and batch-level certification tracking

12.3 Contamination prevention and segregation protocols in manufacturing facilities

12.4 Halal compliance auditing processes and third-party verification frameworks

12.5 Blockchain and digital traceability tools for halal ingredient verification

13. Halal Consumer Trust and Certification Perception

13.1 Consumer trust differences across major halal certification authorities

13.2 Impact of certification logos and labeling clarity on purchasing decisions

13.3 Brand credibility challenges in regions with fragmented halal standards

13.4 Influence of religious authority endorsements and community trust networks

13.5 Consumer awareness levels regarding halal cosmetic compliance requirements

14. Halal Beauty Brand Ecosystem and Market Entry Barriers

14.1 Market entry barriers for new halal cosmetic brands including certification costs and compliance timelines

14.2 Competitive positioning of global beauty brands versus dedicated halal brands

14.3 Distribution challenges for halal-certified brands in non-Muslim majority markets

14.4 Brand building strategies focusing on religious compliance and ethical positioning

14.5 Investment and venture funding trends in halal beauty startups

15. Halal Cosmetic R&D and Ingredient Substitution Challenges

15.1 Research challenges in replacing non-halal ingredients with certified alternatives

15.2 Development of plant-based emulsifiers, alcohol substitutes, and bio-derived actives

15.3 Performance benchmarking between halal-compliant and conventional

15.4 formulations

15.5 Stability, preservation, and shelf-life challenges in halal cosmetic formulations

15.6 Collaboration between cosmetic laboratories and halal certification bodies

16 Halal Beauty Retail Ecosystem and Specialty Marketplaces

16.1 Role of halal beauty specialty stores and niche retail networks

16.2 Growth of halal-certified sections within mainstream beauty retailers

16.3 Expansion of Muslim-focused beauty e-commerce platforms

16.4 Retail partnerships with pharmacies, modest fashion outlets, and wellness stores

16.5 Cross-category bundling with halal personal care and wellness products

17 Halal Tourism and Travel Retail Influence

17.1 Impact of halal tourism growth on cosmetic demand in airports and duty-free channels

17.2 Travel-friendly halal cosmetic formats and certification visibility in travel retail

17.3 Tourism-driven cosmetic purchasing behavior in GCC and Southeast Asia

17.4 Hotel, spa, and wellness center partnerships promoting halal beauty products

18. Regulatory and Certification Landscape

18.1 Global and Regional Regulatory Bodies (FDA, EU, ASEAN, GCC, JAKIM, BPJPH/MUI, MUIS, etc.)

18.2 Ingredient Restrictions and Compliance (porcine derivatives, non-halal animal glycerin/stearates, carmine/E120, alcohol origin, parabens, sulfates, PFAS)

18.3 Labeling, Claims, and Safety Standards (halal-certified vs halal-compliant claims, traceability documentation, safety testing)

18.4 Certification Schemes: Organic, Vegan, Cruelty-Free, Halal, Clean Beauty, etc.

18.5 Packaging and Environmental Compliance (EPR, recyclability labeling, material safety, segregation controls for halal assurance)

19. Global Halal Cosmetics Market: Size and Forecast By Segmentation (By Value in USD Million & Volume in Tons) (2025-2032)

19.1. Global Halal Cosmetics Market Size and Forecast, By Product Type

19.1.1 Personal Care Products

19.1.2 Skin Care

19.1.3 Hair Care

19.1.4 Fragrances

19.1.5 Others

19.1.6 Color Cosmetics

19.1.7 Face

19.1.8 Eyes

19.1.9 Lips

19.1.10 Nails

19.2. Global Halal Cosmetics Market Size and Forecast, By Product Format

19.2.1 Liquid

19.2.2 Cream

19.2.3 Gel

19.2.4 Stick

19.2.5 Powder

19.3. Global Halal Cosmetics Market Size and Forecast, By Ingredient Type

19.3.1 Natural Ingredients

19.3.2 Organic Ingredients

19.3.3 Synthetic Ingredients

19.4. Global Halal Cosmetics Market Size and Forecast, By Target Audience

19.4.1 Women

19.4.2 Men

19.4.3 Children

19.5. Global Halal Cosmetics Market Size and Forecast, By Distribution Channel

19.5.1 Online (Non-Store-Based)

19.5.2 Offline (Store-Based)

19.5.3 Convenience Stores

19.5.4 Specialty Stores

19.5.5 Supermarkets/Hypermarkets

19.5.6 Direct Sales

19.6. Global Halal Cosmetics Market Size and Forecast, By Region

19.6.1 North America

19.6.2 United States

19.6.3 Canada

19.6.4 Mexico

19.6.5 Europe

19.6.6 United Kingdom

19.6.7 France

19.6.8 Germany

19.6.9 Poland

19.6.10 Belgium

19.6.11 Netherlands

19.6.12 Italy

19.6.13 Spain

19.6.14 Sweden

19.6.15 Russia

19.6.16 Rest of Europe

19.6.17 Asia Pacific

19.6.18 China

19.6.19 Japan

19.6.20 South Korea

19.6.21 India

19.6.22 Australia

19.6.23 Malaysia

19.6.24 Thailand

19.6.25 Vietnam

19.6.26 Indonesia

19.6.27 Philippines

19.6.28 Rest of Asia Pacific

19.6.29 Middle East and Africa

19.6.30 South Africa

19.6.31 GCC

19.6.32 Nigeria

19.6.33 Egypt

19.6.34 Turkey

19.6.35 Rest of ME&A

19.6.36 South America

19.6.37 Brazil

19.6.38 Argentina

19.6.39 Colombia

19.6.40 Chile

19.6.41 Rest Of South America

20. Company Profile: Key Players

20.1Iba Cosmetics

20.1.1 Overview

20.1.2 Business Portfolio

20.1.3 Financial Overview

20.1.4 SWOT Analysis

20.1.5 Strategic Analysis

20.1.6 Recent Developments

20.2.Wardah (PT Paragon Technology and Innovation)

20.3.Inika Organic

20.4.Amara Cosmetics

20.5.HAYA Beauty

20.6.Sampure Minerals

20.7.TY Cosmetic

20.8.Clara International Beauty Group

20.9.Talent Cosmetics (South Korea)

20.10.Kao Corporation

20.11.Rixin Cosmetics

20.12.Claudia Nour

20.13.Mersi Cosmetics

20.14.Safi Cosmetics

20.15.Inglot Cosmetics

20.16.Ivy Beauty

20.17.786 Cosmetics

20.18.Maya Cosmetics

20.20.So.LEK Cosmetics

20.20.Tuesday in Love

20.21 SimplySiti

20.22 Martha Tilaar Group

20.23 Saba Personal Care

20.23.1 Others

21. Key Findings

22 Strategic Outlook & Future Opportunities

23. Global Halal Cosmetics Market: Research Methodology

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report