Depth Filters Market– Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

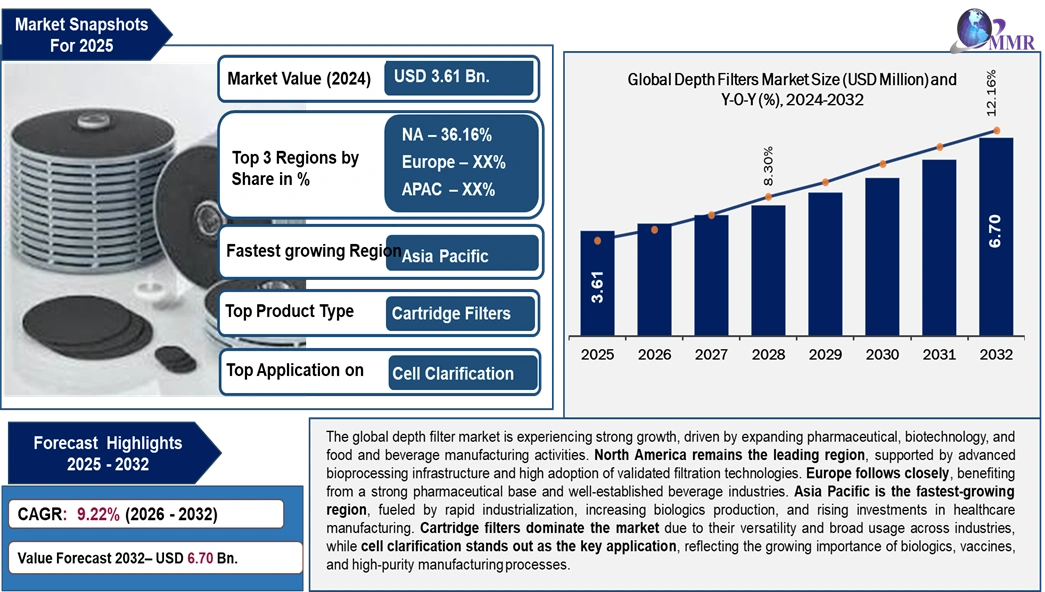

The Depth Filters Market is expected to grow from USD 3.61 Billion in 2025 to USD 6.71 Billion by 2032, reflecting a CAGR of 9.22%. This growth is fueled by the rising adoption of depth filtration in biopharmaceutical manufacturing and clarification processes within food & beverage production.

Depth Filters Market Overview

Depth filters are made from materials such as cellulose, diatomaceous earth, or polypropylene, featuring a complex pore structure that captures particles throughout the entire filter matrix, providing efficient filtration. The increasing demand for efficient filtration in industries such as biopharmaceuticals, food processing, water treatment, and biotechnology boosts the Depth Filters Market.

Key Highlights

• Leading Region: North America holds the largest market share at 36.16%, followed by Europe (31.54%) and Asia Pacific (24.15%), with Asia being the fastest-growing region.

• Fastest Growing Region: The Asia Pacific region is growing rapidly, driven by pharmaceutical capacity expansion, increasing biologics production, and rising investments in healthcare manufacturing.

• Top Product: Cartridge filters dominate the market due to their versatility and use in high-performance, regulated environments, with an Average Selling Price (ASP) of USD 365.

• Key Application: Cell clarification leads the market, reflecting the growing importance of biologics, vaccines, and high-purity manufacturing processes, particularly in the pharmaceutical and biotechnology sectors.

• Product Pricing: Filter modules command the highest ASP of USD 625 in 2025, driven by their large filtration area and suitability for commercial-scale pharmaceutical and biotechnology manufacturing.

To Know About The Research Methodology:- Request Free Sample Report

Depth Filters Market Trends

Structural Shift Toward Single-Use & Disposable Depth Filtration Systems

Multi-product, flexible manufacturing: Biopharmaceutical manufacturers are increasingly adopting multi-product, flexible manufacturing facilities. This shift enables manufacturers to adjust more easily to changes in demand and production requirements.

Cost reduction: The elimination of CIP/SIP (Cleaning in Place/Steam in Place) processes helps reduce validation costs, water consumption, downtime, and contamination risk, all of which are critical in biologics manufacturing.

Rapid scale-up and tech transfer: Disposable depth filters enable faster scale-up, technology transfer, and batch changeover, significantly enhancing production flexibility.

Biopharmaceutical & Biotechnology Applications boost the Demand Engine

Biopharmaceutical & Biotechnology Applications boost the Demand Engine

Demand Shift: Increasing focus on cell clarification, blood separation, and biologics processing, moving away from traditional industrial filtration.

Strategic Importance: Depth filters are yield-critical in biologics workflows; failures lead to batch rejection, yield loss, and regulatory non-compliance.

Depth Filters Market Dynamics

Increasing Filtration Efficiency Requirements

Rising demand for high-efficiency filters: Industries are increasingly adopting high-efficiency filters with 2× higher dirt-holding capacity compared to conventional filters. This improvement ensures better removal of contaminants, boosting production efficiency and reducing operational costs across various sectors.

Increasing focus on reducing pressure drops: There is a growing emphasis on developing filters that achieve 50% lower pressure drops. This minimizes energy consumption, improves flow rates, and ensures enhanced system efficiency without compromising filtration performance, contributing to cost-effective operations.

Operational Efficiency Comparison of Depth Filters Product Types

| Metric | Cartridge Filters | Capsule Filters | Filter Modules |

| Throughput | Moderate | High | Very High |

| Yield Stability | Medium | High | Very High |

| Downtime | High | Low | Very Low |

Depth Filter Market Restraints

| Restraints | Factors limit growth | Impact on the market | Insight |

| High-Cost Sensitivity in Food & Beverage and Industrial Applications | Food & beverage and industrial users operate under tight margin structures and remain price-driven in procurement decisions | Preference for traditional filter sheets and low-cost media | While F&B contributes significant volumes, its pricing sensitivity restricts value expansion and delays technology upgrades. |

| Application-Specific Qualification Requirements & Limited Standardization | Depth filter performance is highly process-specific, influenced by fluid chemistry, particulate load, and process conditions | Longer sales and conversion cyclesHigher pre-sales technical effort and customer onboarding costs | The absence of universal filtration standards increases switching barriers but slows new customer acquisition and rapid scaling. |

Depth Filters Market Segmentation Analysis

Based on Product type, the market is segmented into Cartridge Filters, Capsule Filters, Filter Modules, and Filter Sheets. Cartridge Filters dominated the Depth Filter Market with 34.70% share in 2025, driven by their efficiency and versatility in industrial applications.

By Material, the market is categorized into Diatomaceous Earth, Activated Carbon, Cellulose and Perlite. Cellulose held the Depth Filters Market share 41.70% in 2025 due to its cost-effectiveness, high dirt-holding capacity, and suitability for various filtration applications.

By Material, the market is categorized into Diatomaceous Earth, Activated Carbon, Cellulose and Perlite. Cellulose held the Depth Filters Market share 41.70% in 2025 due to its cost-effectiveness, high dirt-holding capacity, and suitability for various filtration applications.

Depth Filters Market Regional Analysis

North America dominates the Depth Filters Market in 2024, with a 34.33% share, driven by advanced filtration technologies, economic growth, and regulatory support. Europe follows closely, benefiting from a strong pharmaceutical base and well-established beverage industries. Asia Pacific is the fastest-growing region, driven by rapid industrialization, increasing biologics production, and rising investments in healthcare manufacturing.

Depth Filters Market Competitive Landscape

Parker Hannifin Corporation agreed to acquire Filtration Group Corporation for USD 9.25 billion, enhancing its global filtration portfolio. Donaldson Company, Inc. acquired Isolere Bio in 2023 to expand its Life Sciences segment with advanced biopharmaceutical purification technologies. Ahlstrom acquired ErtelAlsop in 2024, entering the depth filtration segment and strengthening its position in life sciences filtration. Pentair’s 2025 acquisition of Hydra-Stop for USD 290 million bolsters its Commercial & Infrastructure Water portfolio, while its 2024 purchase of G&F Manufacturing for USD 108 million strengthens its Pool segment and expands its presence in the southeastern U.S. market.

Parker Hannifin Corporation agreed to acquire Filtration Group Corporation for USD 9.25 billion, enhancing its global filtration portfolio. Donaldson Company, Inc. acquired Isolere Bio in 2023 to expand its Life Sciences segment with advanced biopharmaceutical purification technologies. Ahlstrom acquired ErtelAlsop in 2024, entering the depth filtration segment and strengthening its position in life sciences filtration. Pentair’s 2025 acquisition of Hydra-Stop for USD 290 million bolsters its Commercial & Infrastructure Water portfolio, while its 2024 purchase of G&F Manufacturing for USD 108 million strengthens its Pool segment and expands its presence in the southeastern U.S. market.

Recent Developments for Depth Filter Manufacturers

| Date | Company | Recent Development |

| March 24, 2025 | Merck KGaA | Introduced a new line of virus-retentive depth filters for sterile bioprocessing and high-integrity clarification applications. |

| March, 2025 | Sartorius AG | Announced a collaboration with Pall Corporation to co-develop next-generation depth filtration media for biologics manufacturing workflows. |

| December, 2024 | Amazon Filters Ltd. | Launched the SupaPore TMB high-temperature vent filter for pharmaceutical and biotechnology applications requiring robust thermal performance. |

| 2024 | Pall Corporation | Launched the “Kleenpak Presto” series of high-efficiency depth filters for biologics and vaccine production with enhanced single-use technology. |

| December 11, 2024 | FILTROX | Conducted a field test with a QSR operator to evaluate frying oil filtration, introducing SuperSorb CarbonPad for enhanced oil life and reduced downtime. |

| September 4, 2024 | Eaton | Launched advanced filtration solutions at ACHEMA 2024, including SENTINEL MAXPO and BECO CARBON ACF03 activated carbon depth filter sheets. |

Depth Filters Market Scope: Inquire before buying

| Global Depth Filters Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 3.61 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 9.22% | Market Size in 2032: | USD 6.71 Bn. |

| Segments Covered: | by Product Type | Cartridge Filters Capsule Filters Filter Modules Filter Sheets |

|

| by Material | Diatomaceous Earth Activated Carbon Cellulose Perlite |

||

| by Application | Final Product Processing Cell Clarification Blood Separations Others |

||

| by End-User | Food and Beverage Industry Pharmaceuticals Biotechnology Others |

||

Depth Filters Market, by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, ASEAN, Indonesia, Philippines, Malaysia, Vietnam, Thailand, ASEAN, Rest of Asia Pacific)

Middle East & Africa (South Africa, GCC, Nigeria, Rest of ME&A)

South America (Brazil, Argentina, Rest of South America)

Depth Filters Key Players

1. Merck KGaA

2. Sartorius AG

3. Pall Corporation. (Danaher)

4. Parker Hannifin Corp

5. 3M

6. Donaldson Company, Inc.

7. MANN HUMMEL

8. Ahlstrom

9. Eaton

10. Saint-Gobain

11. Pentair

12. Filtrox AG

13. Meissner Filtration

14. Porvair Filtration Group

15. Trinity Filtration

16. Filtteck Co., Ltd.

17. Allied Filter Systems Ltd

18. Fileder Filter Systems Ltd.

19. Cobetter

20. Membrane Solutions

21. Amazon Filters Ltd.

22. Graver Technologies

23. Clariance Technique

24. Lenntech

25. Hydac International

26. Microglass, Inc.

27. GE Water & Process Technologies

28. Filtration Group Corporation

Frequently Asked Questions:

1. Which region has the largest share in the Global Depth Filters Market?

Ans: North America region held the largest Depth Filters Market share in 2025.

2. What is the growth rate of the Global Depth Filters Market?

Ans: The Global Market is expected to grow at a CAGR of 8.78 % during the forecast period 2026-2032.

3. What is the scope of the Global Depth Filters Market report?

Ans: The Global Depth Filters Market report helps with the PESTEL, Porter's Five Forces, Recommendations for Investors and leaders, and market estimation for the forecast period.

4. Who are the key players in the Global Depth Filters Market?

Ans: The important key players in the Global Depth Filters Market are Merck KGaA, Sartorius AG, Pall Corporation (Danaher), Parker Hannifin Corp,3M, Donaldson Company, Inc. and others.

5. What is the study period of this Depth Filters market?

Ans: The Global Depth Filters Market is studied from 2025 to 2032.

6. What are the growth drivers for the Depth Filters Market?

Ans: Growth drivers for the Depth Filters market include increasing demand for efficient filtration in industries like pharmaceuticals, food processing, water treatment, and biotechnology, along with advancements in filtration materials and technologies.