Chewing Gum Market - Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

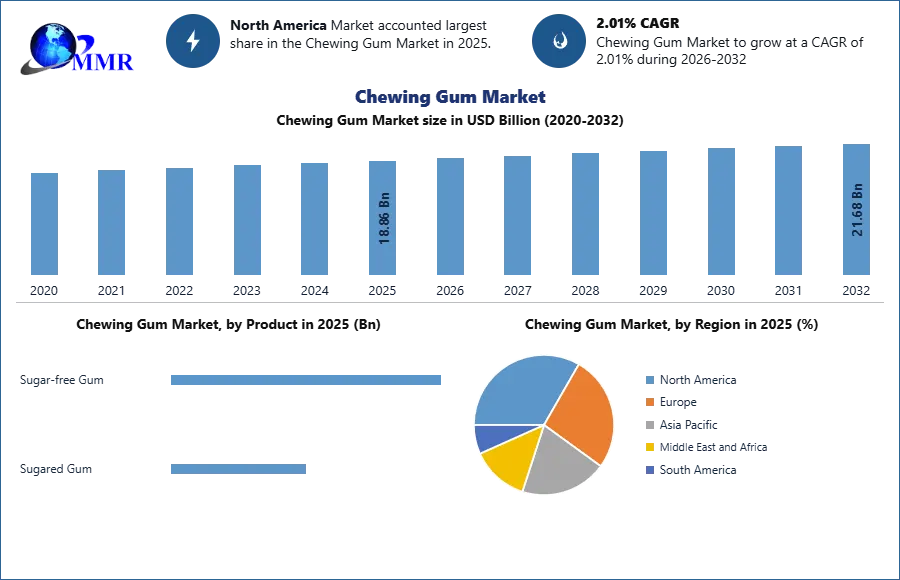

The Chewing Gum Market size was valued at USD 18.86 Billion in 2025 and the total Chewing Gum revenue is expected to grow at a CAGR of 2.01% from 2026 to 2032, reaching nearly USD 21.68 Billion in 2032.

The Chewing Gum operates the broader confectionery and fast-moving consumer goods (FMCG) industry, shaped by behavioral consumption patterns, socio-cultural influences, and innovation-driven product development. The Chewing Gum market is fundamentally driven by the psychological and sensory appeal of chewing, which is associated with refreshment, stress relief, habit-forming behavior, and social acceptance. Chewing gum functions as both a recreational product and a utilitarian item, creating dual demand from pleasure-seeking consumers and seeking functional benefits such as oral hygiene, energy enhancement, smoking cessation, or nutritional supplementation.

The Chewing Gum consumer behavior, where preference formation is influenced by taste, convenience, health perceptions, price sensitivity, and brand loyalty. The shift toward sugar-free and functional gums reflects the health belief model, where consumers choose products that align with preventive health behaviors. Additionally, the rise of natural, clean-label, and biodegradable gums aligns with theories of sustainable consumption and ethical purchasing, driven by environmental consciousness.

To know about the Research Methodology:-Request Free Sample Report

Chewing Gum Market Dynamics:

The global chewing gum market is undergoing a significant transformation driven by shifting consumer preferences, lifestyle changes, and continuous innovation across formulation, flavor, and functionality. One of the foremost developments shaping market dynamics is the rapid rise of sugar-free and functional chewing gums. With increasing global awareness about oral hygiene, dental health, and low-calorie intake, sugar-free chewing gum now accounts for nearly 58–60% of the total market share, up from 48% ten years ago. Consumers are choosing xylitol- and sorbitol-based formulations due to their proven dental benefits, including reduced cavity risks and enhanced salivary flow. Parallel to this shift, the market is witnessing unprecedented growth in functional gum categories such as nicotine gum, vitamin-infused gum, probiotic gum, energy gum, and CBD gum. These specialized products are supported by demand from health-conscious consumers, urban professionals, and individuals seeking convenient wellness formats. Such trends highlight the evolution of chewing gum from a traditional confectionery item to a multifunctional, on-the-go wellness product.

The major factor influencing the chewing gum market is the boom in flavor innovation and clean-label product development. Manufacturers are investing in new flavor combinations, long-lasting flavor technologies, and multi-layer gum formats to enhance consumer experience and strengthen brand differentiation. Fruit, mint, cooling-effect, and hybrid flavors dominate new global launches, driven by the preferences of younger demographics. Clean-label gum, which avoids artificial sweeteners such as aspartame and synthetic plasticizers, is gaining substantial traction in developed markets such as the United States, Germany, France, Japan, and the Nordic region, where natural ingredients are increasingly valued. These natural gums are contributing to the growth of eco-friendly chewing gum alternatives, with the biodegradable gum segment, presenting new opportunities for sustainability-driven manufacturers.

Production trends the competitive landscape of the global chewing gum market. Annual global production ranges between 1.7 and 1.9 million tonnes, dominated by multinational giants such as Mars Wrigley, Mondelez International, Perfetti Van Melle, Lotte Confectionery, and Ferrero. These companies collectively hold 55–60% of global market share, supported by advanced manufacturing capabilities, extensive product portfolios, international distribution networks, and long-established brand recognition. The United States leads production with an estimated 580,000–600,000 tonnes annually, particularly in sugar-free and functional gum categories. China, producing around 320,000–350,000 tonnes, is a major global exporter and a key supplier for Asia-Pacific markets. Turkey, Mexico, and select European countries remain important production hubs due to their cost-efficient manufacturing bases and strategic export capabilities.

Price dynamics play a critical role in shaping profitability and market competitiveness. In 2024, average global prices ranged between USD 3.2 and 5.5 per kg for standard chewing gum, USD 4.5–7.2 per kg for sugar-free gum, and USD 11–18 per kg for functional gum variants. Premium natural gum products, including plant-based gum bases, fetch USD 12–16 per kg due to higher production costs and niche demand. Raw material price fluctuations—particularly in natural sweeteners and mint oils—have affected production economics. Xylitol prices increased by 6–8% in late 2024, primarily due to limited birchwood supply in Finland and China. Similarly, mint oil prices showed volatility after lower-than-expected crop yields in India, which supplies nearly 80% of the world’s mint oils. These fluctuations have encouraged manufacturers to adopt cost-optimization strategies, alternative sweetener blends, and more efficient packaging solutions.

Evolving consumer behavior is among the core drivers reshaping demand patterns. Young consumers, particularly teens and young adults, represent 45–48% of global gum consumption, preferring innovative flavors, sensory cooling effects, and interactive product formats. With growing concern over sugar content and oral hygiene, a substantial portion of consumers in urban markets now opt for sugar-free gum after meals, supported by dental associations worldwide. The rise of “on-the-go freshness” lifestyles has also boosted demand for pocket-sized packs and mini-format gums, which have grown 18–20% year-on-year. Meanwhile, smoking reduction trends have propelled the rapid growth of nicotine gum, expanding at 10–12% CAGR, supported by smoking cessation programs and increasing health awareness. The trend toward mindful snacking is pushing consumers away from high-calorie sweets toward healthier chewing alternatives, reinforcing long-term growth prospects for the chewing gum industry.

Global trade patterns underscore the increasing demand for value-added gum products across international Chewing Gum market. Turkey emerged as the world’s largest exporter in 2024–2025, with export revenues of USD 475–520 million, followed by the United States with USD 420–460 million, China with USD 310–335 million, and the Netherlands, which recorded USD 190–210 million. Countries in Southeast Asia, Africa, and Latin America are becoming rapidly expanding import markets due to growing urban populations, Western-style retail formats, and rising demand for affordable yet high-quality confectionery products. Functional gums—particularly nicotine, vitamin, and energy variants are becoming the fastest-growing export segment, presenting strong opportunities for manufacturers investing in R&D and technological innovation.

Chewing Gum Market Segment Analysis:

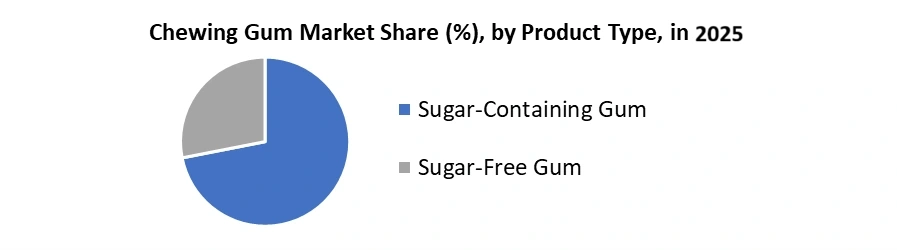

Sugar-free gum remained the dominant and fastest-growing segment in 2024, accounting for more than 55–60% of the global market. Its leadership was supported by strong consumer preference for oral-care benefits, lower calories, and dentist-endorsed ingredients such as xylitol. The segment benefited from lifestyle shifts toward preventive health, sugar reduction, and functional products. Innovations such as long-lasting flavours, whitening agents, vitamin-infused gums, and natural sweeteners further strengthened its appeal. Sugar-free gum also gained traction through supermarkets, pharmacies, and online platforms. With rising health consciousness, this segment consistently outperformed traditional sugar-containing variants.

Sugar-containing gum dominated the traditional and legacy segment of the chewing gum market in 2024. Its demand driven due to strong penetration in developing countries, affordable pricing, and a wide variety of sweet flavours targeted at children and younger consumers. The segment continued to hold relevance due to impulse purchases at convenience stores and cultural preferences for sugary products. However, its growth had slowed significantly as global consumers became more aware of the negative health effects linked to sugar intake and dental decay. Increasing oral-health awareness campaigns, rising regulatory pressure on sugar consumption, and the growing popularity of healthier snacking habits further reduced demand. The sugar-containing gum-maintained importance in regions such as Asia, Latin America, and the Middle East, it increasingly lost share to healthier alternatives.

Chewing Gum Market Regional Analysis:

North America is the dominant market with a 33–35% share in 2024, supported by high per capita consumption and strong demand for sugar-free and functional gum products. Europe, accounting for 27–29%, shows stable growth, driven by premium and natural gum offerings. The Asia-Pacific region, with a 26–28% market share, is forecast to be the fastest-growing region, supported by rising disposable incomes, rapid urbanization, and increasing consumer interest in flavored and sugar-free chewing gum. Markets such as India, China, Indonesia, and Vietnam display strong upward trends, while Japan and South Korea lead in consumption of wellness-oriented mouth-freshening gums. Latin America and the Middle East & Africa contribute modest shares, rapid expansion of modern retail and increasing exposure to Western confectionery trends are creating new sales opportunities.

Competitive Landscape:

The chewing gum market characterized by strong consolidation, with a few global players dominating share through extensive distribution networks, brand loyalty, and continuous product innovation. Key companies such as Mars Wrigley, Mondelez International, Perfetti Van Melle, Lotte Confectionery, and Cloetta held leadership positions. These firms competed through flavour innovation, sugar-free formulations, long-lasting taste technologies, and functional gum offerings such as oral-care and nicotine-replacement gums. Regional players in Asia and Latin America expanded their presence through affordable price points and localized flavours. Sustainability, clean-label ingredients, and natural gum bases increasingly shaped competitive strategies.

Scope of the Global Chewing Gum Market: Inquire before buying

| Chewing Gum Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 18.86 USD Billion |

| Forecast Period 2026-2032 CAGR: | 2.01% | Market Size in 2032: | 21.68 USD Billion |

| Segments Covered: | by Product | Sugar-free Gum Sugared Gum |

|

| by Format | Stick Gum Pellet/Tablet Gum Center-Filled Gum Liquid-Filled Gum Others |

||

| by Distribution Channel | Supermarkets / Hypermarkets Convenience Stores Specialty Stores Pharmacies / Drugstores (especially for functional and smoking-cessation gum) Online / E-commerce |

||

Global Chewing Gum Market, by Region

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

North America (United States, Canada and Mexico)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players / Competitors Profiles Covered in Brief in Global Chewing Gum Market Report in Strategic Perspective:

- Mars, Incorporated

- Mondelez International

- Perfetti Van Melle

- Lotte Corporation

- The Hershey Company

- Ferrero Group

- Cloetta

- Grupo Arcor

- Meiji Holdings Co., Ltd.

- GlaxoSmithKline plc

- August Storck KG

- Orion Corp.

- Bourbon Corp.

- Adam Foods

- Chicza

- True Gum

- Simply Gum

- Milliways Food Limited

- Tootsie Roll Industries

- Georganics

- Gud Gum

- Oh My Gum

- Nuud Gum

- True Co.

- Mastika