Cell Isolation/Cell Separation Market Size by Product, Technique, Cell Type, Cell Source, End user, Region – Revenue Pool Analysis, Margin Structure Assessment, Capital Flow Trends, Competitive Benchmarking & Forecast to 2032

Overview

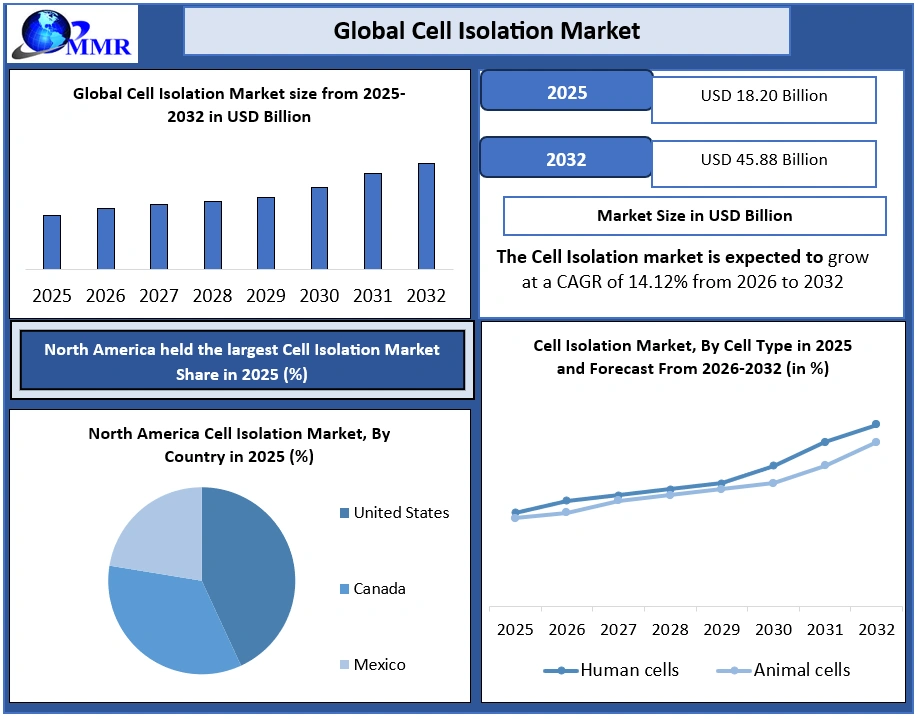

The global Cell Isolation Market was valued at USD 18.20 Billion in 2025 and is projected to reach USD 45.88 Billion by 2032, growing at a CAGR of 14.12% during 2026–2032. Market growth is driven by increasing demand for high-purity and high-viability cell separation in cell and gene therapy manufacturing, expansion of CAR-T and stem cell pipelines, rapid adoption of single-cell analysis workflows, and rising regulatory emphasis on GMP-compliant, automated cell processing solutions.

Cell Isolation Market Overview

Cell isolation refers to the separation of specific cell populations from heterogeneous biological samples for downstream analysis or therapeutic use. The Cell Isolation Market encompasses technologies capable of delivering 90–99% target cell purity and high post-isolation viability across applications such as cell therapy manufacturing, immunology, oncology, and stem cell research.

To Know About The Research Methodology :- Request Free Sample Report

Advanced cell isolation platforms process approximately 10⁶–10⁹ cells per run, achieve recovery rates exceeding 85%, and reduce processing time by 30–40% compared to manual protocols. Adoption is led by magnetic-activated cell sorting (MACS), fluorescence-activated cell sorting (FACS), automated closed systems, and clinical-grade isolation kits, supported by more than 1,200 active CAR-T clinical trials globally as of 2025 and rising demand for GMP-compliant cell processing workflows.

Key Insights

• Automated cell isolation systems enable processing of approximately 500–1,200 samples per week, reduce manual error rates by nearly 35%, and enhance protocol standardization across multi-site cell therapy manufacturing facilities in 2025.

• Expanding CAR-T and stem cell therapy pipelines require isolation platforms supporting 24–48-hour turnaround times, consistent performance across more than 20 process steps, and compliance with ISO 13485 and FDA 21 CFR Part 11 standards.

• Magnetic beads, isolation kits, and antibodies exhibit replacement cycles of 1–3 days per laboratory, enabling continuous workflows and delivering 15–25% operational cost optimization in high-throughput cell separation environments.

• Centrifugation remains integral to more than 80% of pre-processing workflows in 2025, supporting parallel sample handling and compatibility with downstream FACS, MACS, and microfluidic isolation platforms.

• North American laboratories operate more than 60 dedicated cell processing facilities, achieve over 98% protocol adherence in 2025, and lead adoption of closed-system, digitally tracked cell isolation solutions for clinical and translational research.

Cell Isolation Market Dynamics

Automation and Single-Cell Workflows to boosts Cell Isolation Market

Automation has emerged as a defining trend in the Cell Isolation Market, driven by the need for high-throughput, reproducible, and scalable cell separation. By 2025, research and clinical laboratories are increasingly replacing manual protocols with automated systems to improve consistency and reduce operator-dependent variability. These platforms are tightly integrated with single-cell analysis, flow cytometry, genomics, and proteomics workflows, supporting precision medicine applications.

• Single-cell isolation workflows process approximately 10³–10⁶ cells per run in 2025

• Closed-system platforms reduce contamination risk by 30–40%

• Automation improves batch-to-batch reproducibility by more than 25%

• Adoption is strongest in cell therapy manufacturing and translational research environments

Rising Cell and Gene Therapy Activity to Drive Cell Isolation Market

Cell isolation is a critical upstream step in manufacturing CAR-T, TCR-T, stem cell, and immune cell therapies, requiring high purity, viability, and scalability. With increasing clinical activity, developers demand reliable isolation technologies that meet GMP and regulatory standards, driving the Cell Isolation Market.

• Over 1,000 active cell therapy clinical trials globally

• Isolation protocols achieve 95% cell purity and more than90% viability

• Processing volumes range from 10⁶ to 10⁹ cells per batch

• Strong demand for CD3, CD4, CD8, CD19, and CD34 cell isolation

• Automation improves manufacturing throughput by 30–50%

Technical Complexity and High Implementation Costs

The cell isolation market faces restraints due to technical complexity, high capital investment, and skilled labor requirements. Advanced isolation platforms such as FACS, automated magnetic systems, and microfluidics-based technologies require extensive optimization and trained personnel, limiting adoption in smaller laboratories.

• Specialized training requirements of 6–12 months

• Multi-step workflows increase variability risk by 15–20%

• High maintenance and validation burden for GMP systems

• Protocol customization required for different cell types

• Increased operational costs in high-throughput settings

Insights on the Cell Isolation Market

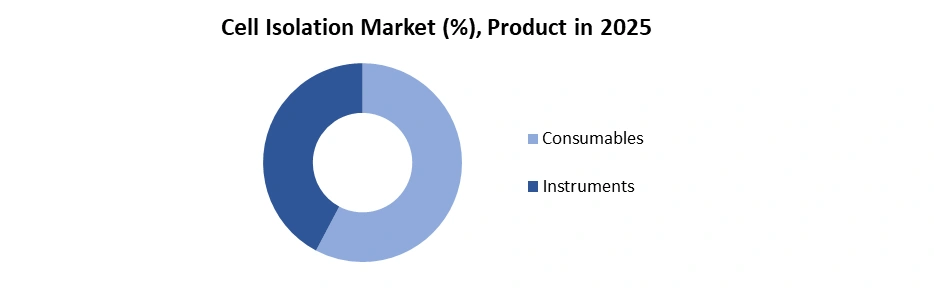

By Product, segmented into the Consumables (Reagents & isolation kits, Magnetic beads/microbeads, Antibodies and Others) and Instruments (Centrifuges, Filtration systems and Others).

Consumables dominate the cell isolation market due to their high repeat usage, workflow dependency, and protocol-specific consumption across research and clinical laboratories. Reagents, isolation kits, magnetic beads/microbeads, and antibodies are used in every isolation run, unlike instruments, which are one-time capital investments. Magnetic bead-based consumables deliver more than 95% cell purity, more than 90% viability, and support processing of 10⁵ to 10⁹ cells per batch, making them essential for cell therapy manufacturing, immunology research, and stem cell applications.

Factors Boosting the Consumables Cell Isolation Market Growth

• Consumables replaced after every isolation cycle

• Typical isolation time of 15–30 minutes

• Compatible with automation platforms, reducing labor by 42–62%

• High demand for CD3, CD4, CD8, CD19, CD34 antibodies

• Strong use in GMP and clinical-grade workflow

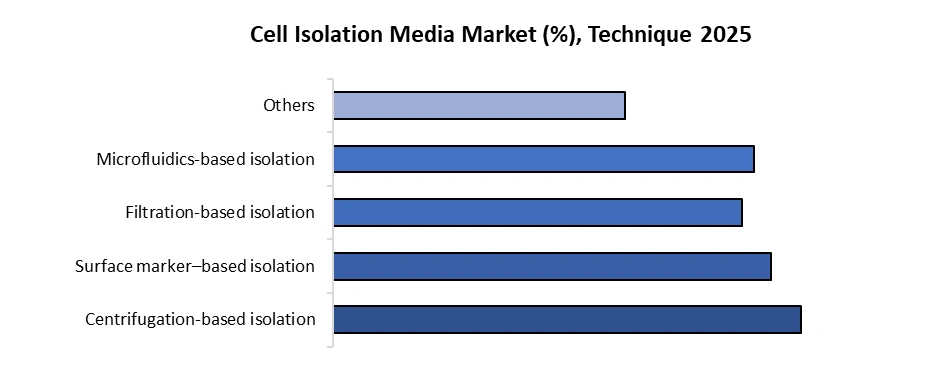

By Technique, categorized into the Centrifugation-based isolation, Fluorescence-activated cell sorting (FACS), Filtration-based isolation, Microfluidics-based isolation, and Others.

Centrifugation-based isolation dominated the Cell Isolation Market in 2025. It is cost-effectiveness, simplicity, and universal laboratory availability. It is routinely applied as a primary or pre-enrichment step in workflows involving PBMC isolation, density gradient separation, and debris removal. Standard centrifugation protocols process samples in 10–20 minutes, handling volumes up to 50–100 mL per run, making them suitable for high-throughput research environments.

Key drivers reinforcing the dominance of this segment include:

• Present in more than 90% of biological laboratories

• Requires minimal consumables

• Compatible with downstream FACS, MACS, and microfluidics

• Maintains 80–90% cell viability

• Ideal for bulk cell separation and sample preparation

Despite growing adoption of advanced methods such a FACS and microfluidics, centrifugation remains the foundational and most utilized cell isolation technique worldwide.

Cell Isolation Market Regional Analysis

North America dominated the Cell Isolation Market in 2025 and is expected to continue its dominance over the forecast period. The strong concentration of biopharmaceutical companies, advanced research institutes, and cell therapy manufacturing facilities. The region leads in the adoption of magnetic bead-based cell isolation technologies, such as positive and negative cell separation, driven by high demand for cell therapy, immuno-oncology, and single-cell research. Laboratories in the U.S. and Canada routinely achieve >95% cell purity, more than 90% viability, and 15–30-minute isolation cycles using automated platforms.

Key regional strengths include:

• Presence of 70%+ global cell therapy clinical trials

• High adoption of GMP-compliant and closed-system cell isolation

• Automation reduces hands-on time by 40–60%

• Broad use across human and mouse cell isolation workflows

• Strong integration with flow cytometry, omics, and cell expansion

Cell Isolation Market Competitive Analysis

The cell isolation market is highly competitive, driven by leading cell separation companies that offer advanced cell isolation technologies, including magnetic cell sorting and flow cytometry solutions, with a rising demand from cell therapy, stem cell research, and single-cell analysis applications worldwide.

Recent Developments

• September 6, 2023: Thermo Fisher Scientific launched the Gibco CTS Detachable Dynabeads platform, introducing an active release mechanism for cell isolation that enhances process flexibility, scalability, automation compatibility, and high cell purity for clinical and commercial cell therapy manufacturing.

• May 18, 2023: BD launched the BD FACSDiscover S8 Cell Sorter, the world’s first system combining spectral flow cytometry and real-time cell imaging, enabling high-speed, high-parameter cell isolation and sorting for advanced research and cell-based therapeutic development.

• May 30, 2024: Cytiva launched the Sefia cell therapy manufacturing platform, a modular and automated solution integrating advanced cell isolation capabilities to reduce variability, improve efficiency, and accelerate scalable CAR-T cell therapy manufacturing from clinical development to commercial production.

Cell Isolation Market Scope: Inquire before buying

| Global Cell Isolation/Cell Separation Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 18.20 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 14.12% | Market Size in 2032: | USD 45.88 Bn. |

| Segments Covered: | by Product | Consumables Reagents & isolation kits Magnetic beads / microbeads Antibodies Others Instruments Centrifuges Magnetic-activated cell separation systems (MACS) Flow cytometers / cell sorters (FACS) Filtration systems Others |

|

| by Technique | Centrifugation-based isolation Surface marker–based isolation Magnetic-activated cell sorting (MACS) Fluorescence-activated cell sorting (FACS) Filtration-based isolation Microfluidics-based isolation Others |

||

| by Cell Type | Human cells Animal cells |

||

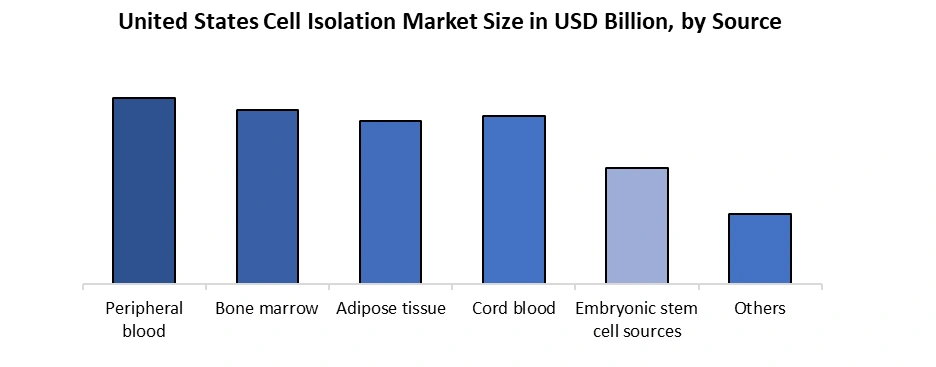

| by Cell Source | Peripheral blood Bone marrow Adipose tissue Cord blood Embryonic stem cell sources Others |

||

| by Technique | Cancer research Stem cell research Regenerative medicine & tissue engineering In-vitro diagnostics Biomolecule isolation Others |

||

| by End user | Research & academic institutes Biotechnology companies Pharmaceutical companies Hospitals & diagnostic laboratories Contract research organizations (CROs) Others |

||

Cell Isolation/Cell Separation Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Cell Isolation Key Players

1. Thermo Fisher Scientific

2. Becton, Dickinson and Company

3. Danaher Corporation

4. Miltenyi Biotech

5. STEMCELL Technologies

6. Merck KGaA

7. Bio-Rad Laboratories

8. Agilent Technologies

9. Corning Incorporated

10. Beckman Coulter

11. Cytiva

12. Terumo Corporation

13. Lonza Group

14. Qiagen

15. PerkinElmer

16. Bio-Techne

17. Takara Bio

18. 10x Genomics

19. Sony Biotechnology

20. Carl Zeiss

21. Akadeum Life Sciences

22. PluriSelect Life Science

23. InGeneron

24. Cedarlane Laboratories

25. Sphere Bio

26. Duoning Biotechnology

27. Cellares

28. Philips Healthcare

29. Sigma-Aldrich

30. Clontech Laboratories

Frequently Asked Questions (FAQ)

1. Which region was dominated the Cell Isolation Market in 2025?

Answer: North America was the dominant region for the Cell Isolation Market in 2025, supported by a high concentration of biopharma and cell therapy manufacturing facilities, strong adoption of GMP-compliant closed systems, and widespread use of automated magnetic cell isolation platforms in the U.S. and Canada.

2. What is the expected annual growth rate of the Cell Isolation Market?

Answer: The Cell Isolation Market is expected to grow at a CAGR of 14.12% from 2026 to 2032, driven by expanding CAR-T and stem cell pipelines, rising single-cell sequencing workflows, and increasing demand for standardized, automated, and digitally tracked cell processing solutions.

3. What is the main factor driving demand for automated cell isolation systems?

Answer: The key driver is the scaling of cell therapy manufacturing automated systems reduce hands-on time by 40–60%, and enable 500–1,200 samples per week, improving reproducibility and protocol standardization across multi-site operations.

4. Which technologies are most used in the Cell Isolation Market?

Answer: The major technologies include centrifugation-based isolation (used in 80%+ pre-processing workflows), magnetic-activated cell sorting (MACS), fluorescence-activated cell sorting (FACS), and microfluidics-based isolation, selected based on purity, throughput, and clinical-grade requirements.

5. Which companies are leading in the Cell Isolation Market?

Answer: Key players include Thermo Fisher Scientific, BD (Becton Dickinson), Danaher (including Cytiva), Miltenyi Biotec, STEMCELL Technologies, Merck KGaA, Bio-Rad Laboratories, Agilent Technologies, Corning, Beckman Coulter, and Lonza, supported by continuous innovation in automation, closed systems, and clinical-grade consumables.

6. How is cell and gene therapy growth influencing the Cell Isolation Market?

Answer: Rising CAR-T/TCR-T and stem cell therapy activity is significantly boosting demand for high-purity isolation of CD3, CD4, CD8, CD19, and CD34 cells. Developers increasingly require systems that support 10⁶–10⁹ cells per batch, deliver more than 95% purity and more than 90% viability, and meet ISO 13485 and FDA 21 CFR Part 11 compliance expectations.