Business Jet Market – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning / Landscape Review & Global Market Size Forecast to 2032

Overview

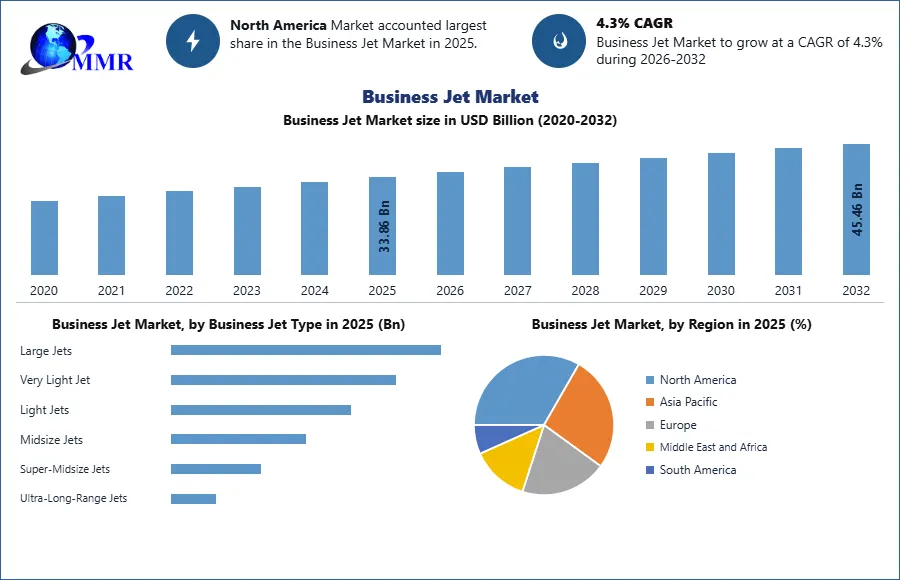

The Business Jet Market size was valued at USD 33.86 Billion in 2025 and the total Business Jet revenue is expected to grow at a CAGR of 4.3% from 2026 to 2032, reaching nearly USD 45.46Billion.

Business Jet Market Overview:

The Business Jet Market is a dynamic sector driven by economic conditions, technological advancements, and shifting consumer demands. Demand for business jets fluctuates with economic cycles, closely tied to corporate profitability and global business activity. During periods of economic growth, companies are more inclined to invest in private air travel to facilitate business operations and expansion. Rising income levels among high-net-worth individuals contribute to increased demand for luxury transportation options. Technological innovations play a significant role in shaping the Business Jet market landscape, with manufacturers constantly striving to enhance aircraft performance, safety, and comfort.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Advancements in aircraft design, engine efficiency, and avionics technology have led to the development of more fuel-efficient and eco-friendly aircraft. Manufacturers are focusing on integrating state-of-the-art amenities, such as advanced entertainment systems and connectivity features, to meet the evolving needs of business jet passengers. While the business jet industry faces challenges such as economic uncertainty and regulatory constraints, growth opportunities exist, particularly in emerging markets in Asia-Pacific, Latin America, and the Middle East. Business Jet Market is embracing sustainability initiatives, with ongoing research and development efforts aimed at reducing emissions and mitigating environmental impact. Overall, the business jet market remains resilient, with prospects for continued evolution driven by innovation and changing market dynamics.

Business Jet Market Dynamics:

Development of airport infrastructure boosts the Business Jet Market growth

The development of airport infrastructure driving the growth of the Business Jet Market. Enhanced airport facilities cater specifically to the needs of private and corporate aviation, thus encouraging more businesses and individuals to invest in business jets. Improved runway and taxiway systems accommodate a diverse range of business jet sizes, including larger aircraft, allowing for more efficient take-offs and landings. This enhances accessibility to a wider range of airports, including those previously inaccessible to larger commercial aircraft, thus increasing the flexibility and convenience of private air travel. Also, upgraded terminal facilities provide dedicated services and amenities for business jet passengers, such as VIP lounges, expedited security procedures, and premium handling services. These enhancements elevate the overall travel experience, attracting more high-net-worth individuals and corporate clients to choose private aviation over commercial alternatives. Significant, investment in air traffic control infrastructure and technology improves airspace management, reducing congestion and delays for business jet operators. Enhanced navigation systems and communication networks enhance safety and efficiency, facilitating smoother operations and encouraging greater utilization of Business Jets for executive travel. The development of airport infrastructure creates an environment conducive to the growth of the business jet market by improving accessibility, convenience, and efficiency, thereby attracting more users and driving demand for private aviation services.

For Example, Globally, the United States boasts the highest airport density, with approximately one airport for every 60,000 individuals. The sheer number of airports in the US, exceeding 5000, is unmatched anywhere else in the world. In contrast, India's airport density is significantly lower, with only one airport for every 4.6 million people. Remarkably, this density is even lower than that of China, despite China's larger population.

Airports in major countries:

| Sr No. | Country | No. of Airports | Population (Mn) | Population covered per Airport |

| 1 | USA | 5146 | 300 | 60,000 |

| 2 | Brazil | 734 | 190 | 2,61,000 |

| 3 | Russia | 596 | 140 | 2,38,000 |

| 4 | China | 413 | 1330 | 32,25,000 |

| 5 | India | 251 | 1160 | 46,48,000 |

| 6 | Germany | 218 | 80 | 3,76,000 |

| 7 | UK | 198 | 60 | 8,11,000 |

| 8 | Japan | 144 | 12 | 8,86,000 |

Regulatory Restrictions Limit the Business Jet Market Growth

Regulatory restrictions in the Business Jet Market encompass a range of mandates and policies that govern various aspects of aircraft operation, safety, and environmental impact. These regulations significantly impact the industry by influencing aircraft design, operational procedures, and Business Jet Market dynamics. Stringent safety regulations enforced by aviation authorities worldwide require business jet manufacturers to adhere to rigorous standards in aircraft design, manufacturing, and maintenance. Compliance with these standards often entails significant investments in research, development, and certification processes, increasing the cost and time required to bring new aircraft models to market. Also, airspace regulations and restrictions imposed by civil aviation authorities and air traffic control agencies dictate where and when business jets fly.

Airspace congestion, route limitations, and airport slot allocations affect flight efficiency and scheduling flexibility, potentially increasing operating costs and reducing the attractiveness of business jet travel compared to alternative modes of transportation. Environmental regulations aimed at reducing aircraft emissions and noise pollution pose challenges for business jet manufacturers and operators. Compliance with emissions standards, noise abatement procedures, and airport noise curfews necessitate the adoption of new technologies or operational practices, impacting aircraft performance, operating costs, and market competitiveness.

| Regulatory Restriction | Description |

| Safety Regulations | Mandates set by aviation authorities regarding aircraft design, manufacturing standards, and maintenance procedures to ensure the safety of passengers and crew. |

| Airspace Restrictions | Regulations imposed by civil aviation authorities and air traffic control agencies dictate where and when business jets fly, impacting flight efficiency and scheduling. |

| Environmental Standards | Regulations aimed at reducing aircraft emissions and noise pollution, require compliance with emissions standards, noise abatement procedures, and airport noise curfews. |

| Certification Processes | Requirements for obtaining certification from aviation authorities for new aircraft models involve extensive testing, documentation, and demonstration of compliance. |

| Operational Procedures | Guidelines governing operational practices such as flight crew qualifications, training requirements, and aircraft inspection schedules to ensure safe and efficient operations. |

| Airport Regulations | Policies established by airport authorities concerning runway access, parking facilities, ground handling services, and noise mitigation measures affecting business jet operations. |

| Taxation and Fees | Taxes, duties, and fees imposed by governments on aircraft purchases, operations, and fuel consumption, influence the cost of ownership and operation of business jets. |

| Security Measures | Regulations addressing security concerns related to terrorism, hijacking, and unauthorized access to aircraft, requiring compliance with screening protocols and security standards. |

| Import/Export Restrictions | Regulations governing the import/export of business jets across international borders, including customs duties, import tariffs, and export control restrictions. |

Product Innovation in the Jet creates lucrative growth opportunities for the Business Jet Market growth

Product innovation in the business jet market fosters lucrative growth opportunities by driving demand for advanced, efficient, and technologically sophisticated aircraft. Manufacturers investing in research and development to enhance aircraft performance, comfort, safety, and environmental sustainability gain a competitive edge and capture market share. Technological advancements in aircraft design, propulsion systems, avionics, and materials enable the development of next-generation business jets with improved fuel efficiency, longer-range capabilities, and reduced environmental impact. Integration of cutting-edge technologies such as fly-by-wire flight controls, advanced cockpit displays, and autonomous systems enhances flight safety, operational efficiency, and pilot situational awareness, appealing to discerning buyers seeking state-of-the-art aircraft.

Customization and personalization options allow customers to tailor aircraft interiors, amenities, and entertainment systems to their preferences, catering to the luxury segment of the market, where affluent individuals and corporations demand exclusive and bespoke aircraft solutions. Investments in sustainability-focused innovation, such as the development of hybrid-electric or hydrogen-powered propulsion systems and the use of sustainable aviation fuels, align with growing environmental consciousness and regulatory requirements, positioning companies as leaders in eco-friendly aviation solutions.

Business Jet Market Segment Analysis:

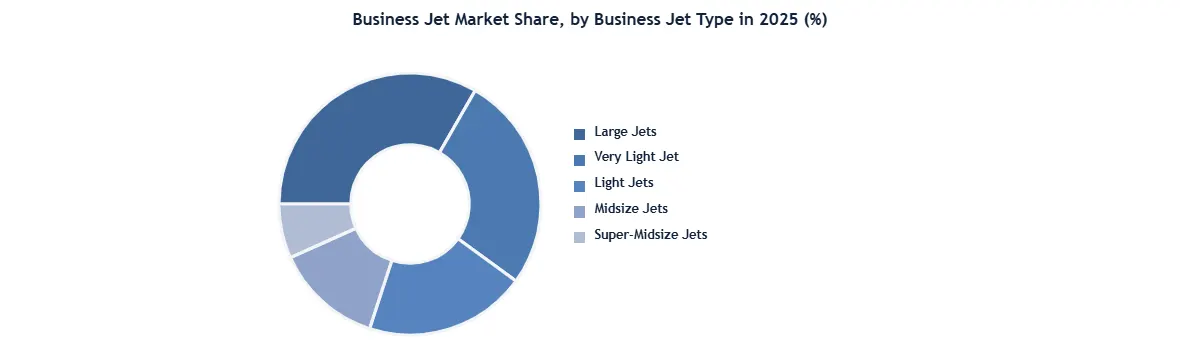

Based on Aircraft Type, the large jet segment dominated the type segment of the Business Jet Market in the year 2025. This is due to the relatively higher prices of large jets compared to light jets, despite the former's lower deliveries compared to the latter. Large jets were in high demand in 2022, as they have a large cabin space that accommodates up to 19 passengers. Large jets offer spacious cabins and extended ranges, catering to the needs of corporate clients and high-net-worth individuals who prioritize comfort and long-distance travel. These aircraft often boast advanced amenities and technological features, enhancing the overall flying experience and meeting the discerning standards of elite clientele. Also, large jets typically accommodate larger groups, facilitating corporate travel and executive retreats with ease. The advancements in technology and design have made these aircraft more fuel-efficient and environmentally friendly, aligning with sustainability initiatives increasingly important to modern businesses. The superior capabilities and amenities of large jets position them as the preferred choice in the Business Jet Market, solidifying their dominance within the type segment.

Business Jet Market Regional Analysis

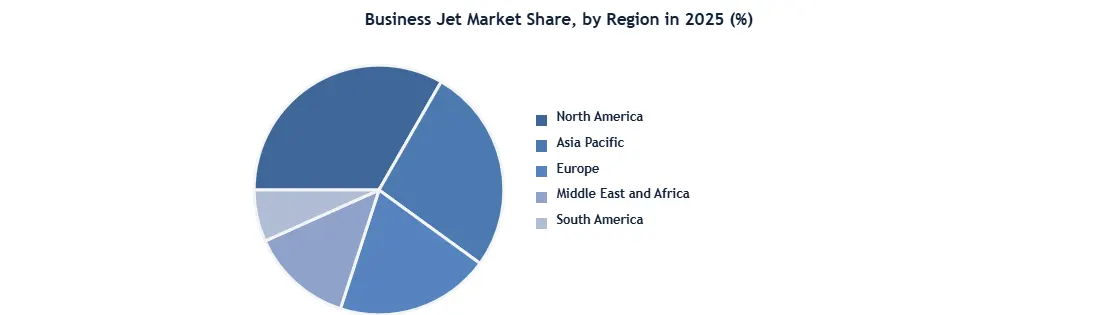

North America Dominated the Business Jet Market in the Year 2025. The region boasts a strong economy with a large number of high-net-worth individuals and corporations, driving demand for private aviation services. The United States, in particular, has a strong culture of business aviation, with many companies utilizing private jets for executive travel and transporting goods. North America is home to some of the world's leading manufacturers of business jets, such as Gulfstream Aerospace, Bombardier, and Textron Aviation. These companies produce a wide range of aircraft catering to different segments of the market, from small, cost-effective models to large, ultra-long-range jets. Also, the continent's extensive infrastructure of airports and FBOs (Fixed Base Operators) supports the operation of business jets, making it convenient for businesses and individuals to travel efficiently and access remote locations. Regulatory frameworks in North America also favor private aviation, with relatively lenient regulations compared to other regions, facilitating the ownership and operation of business jets. Therefore, the combination of a strong economy, leading manufacturers, strong infrastructure, and favorable regulations has positioned North America as the dominant force in the global Business Jet Market.

Business Jet Market Scope: Inquire before buying

| Business Jet Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 33.86 USD Billion |

| Forecast Period 2026-2032 CAGR: | 4.3% | Market Size in 2032: | 45.46 USD Billion |

| Segments Covered: | by Business Jet Type | Large Jets Very Light Jet Light Jets Midsize Jets Super-Midsize Jets Ultra-Long-Range Jets |

|

| by Operational Range | Less than 3,000 NM 3,000–5,000 NM More than 5,000 NM |

||

| by Business Model | Full Ownership Leasing (Operating Lease, Finance Lease) Fractional Ownership Jet Cards & Block-Hour Programs On-Demand Charter Private Jet Membership Others |

||

| by Systems | Avionics Aerostructures Cabin Interiors Aircraft Systems Others |

||

| by Components | Airframe Fuselage Wings Engine Others |

||

| by Point of Sale | OEM Aftermarket Global Business Jet Market Size and Forecast, By End User Individual Owners Businesses and Corporate Entities Charter/Air-Taxi Operators Training and Academic Institutions Government and Special-Mission Operators |

||

Business Jet Market, by Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, and the Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, and the Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria, and the Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Business Jet Market Key Players

- Gulfstream

- Boeing Business Jets.

- Bombardier

- Dassault

- HondaJet

- Textron

- Airbus

- Pilatus

- Embraer Executive

- Cessna Aircraft Company (America)

- Piaggio Aerospace

- Daher

- Diamond Aircraft

- Eclipse Aerospace

- Saab

- Airshare

- Cirrus Aircraft

- Tecnam

- General Dynamics Corp.

- SyberJet LLC.

Others

).