Bones Grafts and Substitutes Market – Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2032

Overview

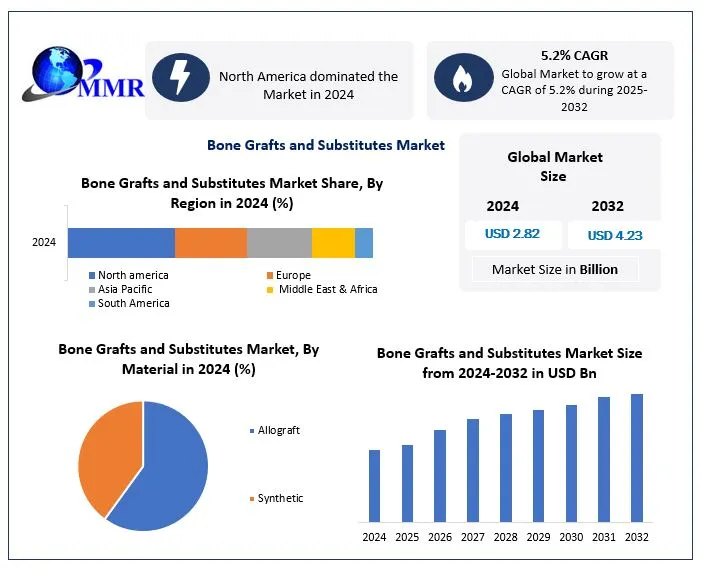

Bones Grafts and Substitutes Market was valued at USD 2.82 Bn in 2024, and total global Bones Grafts and Substitutes Market revenue is expected to grow at a CAGR of 5.2% with aging population, surgical innovations and synthetic grafts drive global adoption and reaching nearly USD 4.23 Bn from 2025-2032

Bones Grafts and Substitutes Market Overview

Bone Grafts and Substitutes Market is a rapidly evolving, industry is focused on biologic and synthetic material used for bone regeneration in orthopaedic, spinal and dental procedures. Growth of market is driven by rising incidence of musculoskeletal disorders affecting over 1.7 billion people globally, increased demand for dental and orthopaedic surgery and shift from autografts to advanced allografts and synthetic grafts due to lower infection risk and better outcomes. Innovations like 3D printed scaffolds, bioactive ceramics and AI integrated robotic surgery platforms are enhancing surgical precision and graft efficacy. North America leads the market by strong healthcare infrastructure and key players like Medtronic, Stryker and Zimmer Biomet, Asia Pacific is fastest growing region fueled by aging demographic and growing healthcare investments. Companies are focusing on R&D, clinical trials and strategic partnerships to expand indications and improve raegenerative capabilities. Recent U.S. and Europe tariff adjustments on imported medical devices ranging from 2.5% to 6% have impacted cross border pricing and disrupted global supply chain, posing cost challenges for manufacturer and distributors.

Report covers the market dynamic, structure by analysing the market segments and projecting Bones Grafts and Substitutes Market size. Clear representation of competitive analysis of key players by type, price, financial position, product portfolio, growth strategies and regional presence in the market. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Bones Grafts and Substitutes Market Dynamics

The increase in the incidence of musculoskeletal disorders, the advance of biocompatible synthetic bone grafts, technological advancements in the medical field leading to a shift from autograft to allograft, and an increase in demand for dental bone grafts. Moreover, an increase in the concentration of prominent players toward research & development activities in bone grafts and substitutes and an increase in demand for orthopedic procedures among the aged population are expected to deliver productive opportunities for the market players in the forecast period (2024-2030). The key trend was seen in the market is the beginning of new polymer and ceramic products that have biologically superior characteristics. The outline of new manufacturing technologies, such as prototyping or 3D printing, is also helping in the fabrication of free-form biomaterial scaffolds for tissue regeneration. However, higher costs of surgeries and ethical issues related to bone grafting procedures are anticipated to limit the bone grafts and substitute market growth.

Bones Grafts and Substitutes Market Segment Analysis

Based on the material segment, the market is segmented into Allograft and Synthetic. The Allograft segment is further sub-segmented into Demineralized Bone Matrix and Others. The Synthetic segment is further sub-segmented into Ceramics, Composites, Polymers, and Bone Morphogenic Proteins (BMP). Among these, the allograft material segment is expected to hold the largest market share by 2032. This is mainly because Allografts have both osteoinductive and osteoconductive properties, hence it serves as a substitute for autografts. These are generally used in spine, hip, and knee areas.

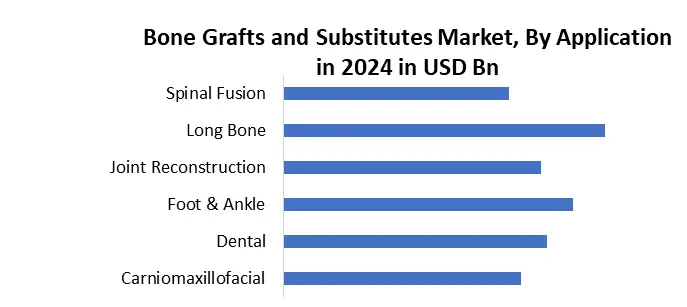

Based on application, segment, the Bone Grafts and Substitutes Market is segmented into craniomaxillofacial, dental, foot & ankle, joint reconstruction, long bone and spinal fusion procedures. Craniomaxillofacial grafts support facial and skull reconstruction, especially after trauma or tumor removal. Dental applications are rapidly growing due to rising demand for implants and periodontal regeneration. In foot and ankle surgeries, grafts are used for structural correction and fracture healing. Joint reconstruction, especially of the hip and knee, relies on grafts for bone defects and revision surgeries. Long bone applications help in healing fractures or filling defects in major bones like the femur and tibia. Spinal fusion holds a dominant share, as grafts are critical for stabilizing vertebrae and enhancing surgical outcomes in spinal disorders.

Bones Grafts and Substitutes Market Regional Insights

North America held the largest market share in the global market in 2024 and is expected to hold a constant position during the forecast period (2025-2032). This is mainly because of the developed healthcare sector in North America and an increase in awareness among healthcare providers about bone grafts and substitutes. Moreover, favourable government regulations about the usage of bone graft & substitutes motivation the growth of the market in North America. Asia-Pacific is expected to hold the largest market share in the global market by 2032, technological developments and growth in the adoption of innovative bone grafts and substitute products are expected to boost the market during the forecast period.

Bones Grafts and Substitutes Market Competitive Landscape

Bone Grafts and Substitutes Market is competitive and innovation driven, with several major players focusing on advanced biologics, synthetic grafts and regenerative technologies to gain market share. Among top companies, Medtronic plc leads with its flagship product INFUSE Bone Graft which alone accounts over 30% of global rhBMP-2 segment, leveraging its expertise in recombinant human Bone Morphogenetic Protein-2 (rhBMP-2) and integrating biologic with robotic-assisted surgery platforms like Mazor X. Company invests USD 2.5 billion annually in R&D and clinical trials to expand indications and improve outcomes. Stryker Corporation is known for its expansive orthobiologics portfolio that includes synthetic grafts and DBM products, backed by significant R&D funding approximately 6.4% of its annual revenue and the integration of enabling technologies like Mako robotic system. Stryker growth is driven by strategic acquisitions and innovations in nano-engineered scaffolds and calcium phosphate based materials. Zimmer Biomet Holdings Inc. maintains a strong position with its comprehensive suite of DBMs, allografts, and synthetic substitutes, focusing on digital health integration through platforms like ZBEdge and surgeon-specific solutions that blend implants, biologics and data. DePuy Synthes a Johnson & Johnson company, combines advanced orthopedic hardware with a robust biologics pipeline. It emphasizes cross platform synergy, minimally invasive techniques, and global expansion, supported by Johnson & Johnson’s R&D spending more than USD 15 billion annually and distribution capabilities. These companies shape the industry through aggressive investment in innovation, evidence based development and integrated surgical ecosystems.

Bones Grafts and Substitutes Market Trends

| Trends | Details | Implications on the Market |

| Shift Toward Synthetic & Biologic Grafts | Increased demand for synthetic grafts, DBMs, and cell-based allografts over traditional autografts and allografts due to lower infection risk. | R&D focus on biocompatibility, osteoconductivity, and regenerative material innovation. |

| Integration of Digital Surgery Platforms | Manufacturers are integrating bone grafts with robotic surgery, AI-assisted planning, and intraoperative navigation systems | Push for product bundling, smart implants, and biologics tailored for minimally invasive procedures. |

| Strategic M&As and Collaborations | Rise in mergers, acquisitions, and licensing deals to expand biologics portfolios and enter new markets. | Investment in clinical data, regulatory clearances, and cross-platform product synergy. |

Bones Grafts and Substitutes Market Key Development

• 7thJanuary, 2025, Medtronic signed a five-year sales agency agreement with Kuros Biosciences to market the MagnetOs bone graft technology alongside its flagship Infuse product in U.S. spinal procedures. This strategic collaboration strengthens Medtronic’s biologics portfolio and expanded surgical ecosystem

• 1st November, 2024, RTI Surgical completed acquisition of Collagen Solutions, a global provider of engineered medical grade collagen and xenograft tissue. This acquisition, following earlier deals such as Cook Biotech, broadens RTI allograft/xenograft portfolio across orthopedics, cardiac, sports medicine and reconstructive surgery.

• 9th January, 2024, Smith & Nephew acquired CartiHeal for USD 180 million upfront, securing access to the Agili C implant for bone and cartilage lesions, this acquisition enhances its sports medicine and regenerative healing offerings.

• 28th November 2023, Kuros Biosciences, MagnetOs Flex Matrix received FDA clearance for interbody spinal cage use, marking Kuros as the first company to gain this indication in the U.S.

• 12th June, 2018, NuVasive recently launched its AttraX Scaffold biologic, a ceramic collagen scaffold for spine surgery, which clinical data shows delivers desirable handling and high fusion rates. Company also published results validating its porous interbody implant and synthetic bone graft substitute as a cost-effective fusion solution.

Bones Grafts and Substitutes Market Scope: Inquire before buying

| Bones Grafts and Substitutes Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 2.82 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 5.2% | Market Size in 2032: | USD 4.23 Bn. |

| Segments Covered: | by Material | Allograft Synthetic |

|

| by Application | Craniomaxillofacial Dental Foot & Ankle Joint Reconstruction Long Bone Spinal fusion |

||

Bones Grafts and Substitutes Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Bones Grafts and Substitutes Market Key Players

North America

1. Medtronic plc (U.S)

2. Stryker Corporation (U.S)

3. Zimmer Biomet Holdings Inc. (U.S)

4. DePuy Synthes (Johnson & Johnson) (U.S)

5. Orthofix Medical Inc. (U.S)

6. NuVasive Inc. (U.S)

7. RTI Surgical (U.S)

8. Xtant Medical Holdings, Inc. (U.S)

9. SeaSpine Holdings Corporation (U.S)

10. LifeNet Health (U.S)

Europe

11. Smith & Nephew plc (UK)

12. Geistlich Pharma AG (Switzerland)

13. Baxter International (Ireland)

14. Exactech, Inc. (Netherlands)

15. Biobank (Italy)

16. NovaBone Products LLC (UK)

17. Bone Therapeutics (Belgium)

18. Bioventus Inc. (Germany)

Asia Pacific

19. OssGen Co., Ltd. (South Korea)

20. Kuros Biosciences (Switzerland)

21. Wright Medical (India)

22. Collagen Matrix, Inc. (Japan)

23. ICU Medical Japan Inc. (Japan)

24. REGEN Biotech Inc. (South Korea)

25. BioAlpha Holdings Berhad (Malaysia)

Bones Grafts and Substitutes Market FAQs

1. What is the market size of the Global Bone Grafts and Substitutes Market in 2024?

Ans. The market size Global market in 2024 was USD 2.82 Billion.

2. What are the different segments of the Global Bone Grafts and Substitutes Market?

Ans. The Global Bone Grafts and Substitutes Market is divided into Application and Material

3. What is the study period of this market?

Ans. The Global Bone Grafts and Substitutes Market will be studied from 2024 to 2032.

4. Which region is expected to hold the highest Global Bone Grafts and Substitutes Market share?

Ans. The Asia Pacific dominates the market share in the market.

5. Who are the top key players of the Global Bone Grafts and Substitutes Market?

Ans. Medtronic Plc, Stryker Corporation are the top key players of the Global Bone Grafts and Substitutes Market.