Biopsy Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

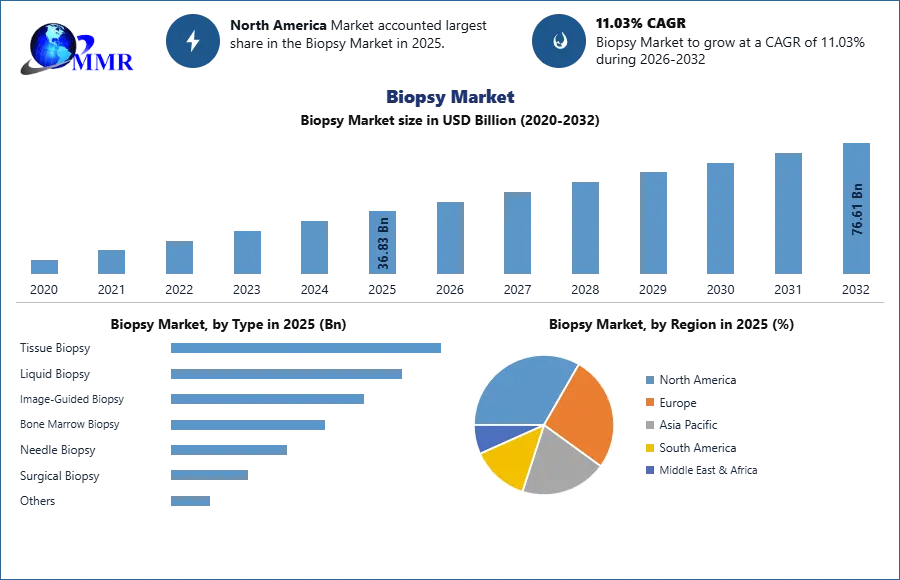

The Biopsy Market size was valued at USD 36.83 Billion in 2025 and the total biopsy revenue is expected to grow at a CAGR of 11.03% from 2026 to 2032, reaching USD 76.61 Billion by 2032.

Global Biopsy Market Overview:

A biopsy is a medical procedure involving the removal of tissue or cells for examination, primarily used to detect, diagnose, and monitor diseases such as cancer, infections, and inflammatory conditions. The global biopsy market is expected to experience strong growth, driven by rising cancer prevalence, increasing demand for minimally invasive diagnostic procedures, and advancements in imaging-guided technologies. Key innovations such as liquid biopsies, AI-assisted diagnostics, and robotic-assisted procedures are enhancing precision and efficiency. North America leads the market due to advanced healthcare infrastructure and strong R&D investments, while Asia-Pacific is driven by growing healthcare access and awareness. With continuous regulatory approvals, technological innovation, and integration of personalized medicine approaches, the biopsy industry is set to grow, offering significant opportunities for healthcare providers and medical device manufacturers.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Biopsy Market Dynamics:

The increasing global burden of cancer continues to be a major driver of the biopsy market. According to the World Health Organization (WHO), cancer remains one of the leading causes of death worldwide, with millions of new cases diagnosed each year and the global incidence projected to rise significantly in the coming decade. This growing disease burden is increasing the need for reliable diagnostic procedures such as biopsies for accurate disease confirmation and treatment planning. Biopsies continue to be the gold standard for cancer diagnosis, staging, and molecular profiling, which is strengthening their adoption across hospitals, diagnostic laboratories, and cancer research centers. In addition, advancements in image-guided biopsy techniques, robotic-assisted procedures, and minimally invasive biopsy technologies are improving diagnostic precision while reducing patient discomfort and recovery time.

As oncology remains the largest clinical application for biopsy procedures, the rising number of cancer screening programs, increasing awareness of early diagnosis, and expanding oncology infrastructure are expected to further accelerate the demand for biopsy instruments, consumables, and diagnostic services globally.

Innovations in Liquid Biopsy and Point-of-Care Devices to Create Lucrative Opportunities for Market Growth

The growing adoption of liquid biopsy presents a transformative opportunity for the Biopsy Market growth. Unlike invasive tissue biopsies, liquid biopsies use blood or other fluids to analyze biomarkers, enabling early disease detection, treatment monitoring, and personalized medicine approaches. With increasing focus on precision oncology, companies are investing in developing advanced point-of-care liquid biopsy devices capable of detecting circulating tumor DNA (ctDNA) and other biomarkers in real time. These innovations not only improve accessibility but also reduce diagnostic turnaround times, particularly in decentralized and resource-limited settings. As healthcare shifts toward personalized care models, the convergence of liquid biopsy and point-of-care technologies is expected to unlock substantial growth potential in the biopsy industry.

Key Challenge: Financial and Policy Barriers Limiting Accessibility

Despite technological progress, reimbursement and cost challenges significantly hinder biopsy adoption. Liquid biopsies and molecular testing are often expensive, with complex and fragmented reimbursement structures creating uncertainty for patients and providers. Many insurers cover only single-gene analyses, leaving patients to bear high out-of-pocket expenses for comprehensive multi-gene tests. This lack of transparency in billing contributes to anxiety and limits the practical uptake of innovative biopsy methods. Moreover, evolving cancer care payment policies require constant compliance, posing additional administrative burdens. Without clear reimbursement frameworks and equitable coverage, access to advanced biopsy technologies will remain restricted, particularly in low- and middle-income countries, restraining the Biopsy Market growth potential.

Global Biopsy Market Segment Analysis:

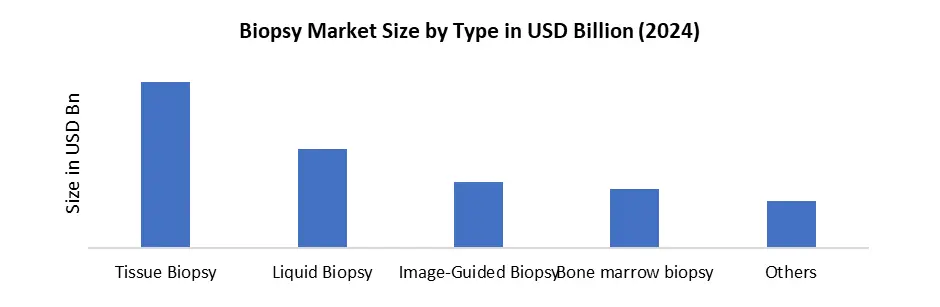

Based on the type segment, tissue biopsy held the largest share in the global biopsy market in 2024. This dominance is primarily attributed to its widespread use in cancer diagnosis and disease staging, where tissue sampling remains the gold standard for confirming malignancies and determining treatment pathways. Tissue biopsies provide high diagnostic accuracy through histopathological examination, making them a preferred choice among clinicians despite being invasive. The increasing global burden of cancer and advancements in image-guided tissue biopsy techniques are reinforcing its adoption. Tissue biopsy continues to account for the largest share compared to liquid and other biopsy types.

North America dominated the global biopsy market in 2025, driven by the high prevalence of cancer, strong healthcare infrastructure, and rapid adoption of advanced diagnostic technologies. The United States remains the major contributor, supported by high healthcare expenditure, increasing cancer screening programs, and continuous product approvals and technological innovations in biopsy devices.

Europe held the second-largest share of the market due to well-established healthcare systems, growing cancer awareness, and increasing adoption of minimally invasive biopsy techniques in countries such as Germany, the UK, and France. Asia Pacific is expected to witness the fastest growth due to expanding healthcare infrastructure, rising cancer incidence, and increasing demand for early diagnostic procedures in countries such as China, India, and Japan. South America is experiencing steady growth due to improving healthcare accessibility and rising diagnostic procedures in countries such as Brazil and Mexico. Middle East & Africa is projected to grow gradually with increasing healthcare investments and expanding oncology diagnostic services in countries such as Saudi Arabia, the UAE, and South Africa.

The strong collaboration between medical device companies, research institutions, and healthcare providers is driving the introduction of AI-driven diagnostic platforms, robotic biopsy devices, and improved imaging-guided systems. With high healthcare spending, a large patient pool, and continuous product launches, North America is expected to remain the key driver of the biopsy market during the forecast period, mirroring its trajectory of innovation-driven growth seen in other advanced healthcare technology markets.

Global Biopsy Market Competitive Analysis:

The global Biopsy Market is marked by intensifying competition, with leading players leveraging R&D, acquisitions, and integrated imaging solutions to strengthen market presence. Companies navigate a complex regulatory and reimbursement landscape, with premium adoption in North America and Europe and cost-sensitive dynamics in Asia-Pacific and emerging economies. Market leaders such as Hologic, BD, and Danaher (Mammotome/Leica) dominate breast biopsy through vacuum-assisted platforms, image-guided systems, and marker portfolios, while Boston Scientific, Olympus, and Cook compete strongly in GI, pulmonary, and urology biopsy tools. Argon, Merit, and B. Braun address niche opportunities with regionally tailored kits and accessories. Players emphasize workflow efficiency, specimen accuracy, and integration with imaging modalities to enhance clinician adoption. Competitive strategies are increasingly shaped by ambulatory migration, AI-driven targeting, and digital pathology connectivity, positioning innovation, localized offerings, and ecosystem lock-in as the key differentiators in this evolving market.

Biopsy Market Recent Developments (2026-2032):

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 12 February 2026 | Roche Diagnostics | The company inaugurated its new Diagnostics Innovation Center in Penzberg, Germany, following a 300 million euro investment in digitalized R&D. | The facility accelerates the development of advanced reagents and diagnostic tests, shortening market access for precision tools used in tissue biopsy analysis. |

| 11 February 2026 | Fujifilm Corporation | The company celebrated the grand opening of its expanded £400 million biomanufacturing facility in Teesside, UK, featuring single-use bioreactor technology. | This expansion enhances global capacity for complex medicines and specialized therapies that require biopsy-confirmed diagnostic monitoring. |

| 09 February 2026 | Becton, Dickinson and Company (BD) | The company successfully completed the strategic spin-off of its Biosciences & Diagnostic Solutions segment into a standalone, publicly traded entity. | The separation allows BD to optimize its medical technology focus while the new entity concentrates on high-growth diagnostic and biopsy instrument innovations. |

| 09 December 2025 | Leica Biosystems | The company launched the Aperio GT 180 DX and CS5 DX scanners alongside Aperio iQC DX software to automate pathology quality control. | These digital pathology innovations improve the speed and consistency of biopsy slide analysis, reducing manual variability in diagnostic laboratories. |

| 21 October 2025 | Hologic, Inc. | The company entered a definitive agreement to be acquired by Blackstone and TPG for approximately USD 15.4 billion. | This major transaction provides Hologic with the financial scale to accelerate global adoption of its interventional biopsy and diagnostic imaging technologies. |

| 06 August 2025 | Exact Sciences Corporation | The company acquired exclusive rights to Freenome’s blood-based colorectal cancer screening technology and announced a 2026 launch for its next-gen Oncodetect test. | This move integrates liquid biopsy capabilities with molecular diagnostics, expanding the market for non-invasive surveillance post-tissue biopsy. |

Biopsy Market Scope: Inquire before buying

| Biopsy Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 36.83 USD Billion |

| Forecast Period 2026-2032 CAGR: | 11.03% | Market Size in 2032: | 76.61 USD Billion |

| Segments Covered: | by Type | Tissue Biopsy Liquid Biopsy Image-Guided Biopsy Bone Marrow Biopsy Needle Biopsy Surgical Biopsy Others |

|

| by Product Type | Instruments Kits & Consumables Services |

||

| by Application | Cancer Inflammatory Disorders Immune Disorders Peptic Ulcer Disease Endometriosis Infectious Diseases Others |

||

| by End-User | Hospitals Diagnostic Laboratories Cancer Research Centers Academic & Research Institutions Ambulatory Surgical Centers Others |

||

Biopsy Market, by Region:

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

South America (Brazil, Argentina, and rest of South America)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

Biopsy Market Key Players:

1. Hologic, Inc.

2. Leica Biosystems (Danaher Corporation)

3. Mammotome (Devicor Medical Products)

4. Becton Dickinson & Company (BD)

5. Medtronic plc

6. Johnson & Johnson (Ethicon)

7. C.R. Bard, Inc. (BD subsidiary)

8. Cook Medical

9. Guardant Health, Inc.

10. Triopsy Medical, Inc

11. Quibim

12. Exact Sciences Corporation

13. Celsee Diagnostics

14. Biocept, Inc.

15. Argon Medical Devices

16. Natera, Inc.

17. Freenome Holdings, Inc.

18. Leica Biosystems (Danaher Corporation)

19. Roche Diagnostics

20. QIAGEN N.V.

21. Fujifilm Holdings Corporation

22. Olympus Corporation

23. Nipro Corporation

24. Terumo Corporation

25. Biobot Surgical