Bio Fertilizers Market Size by Product Type, Form, Microbe Type, Crop Type, Farming System, Application, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2034

Overview

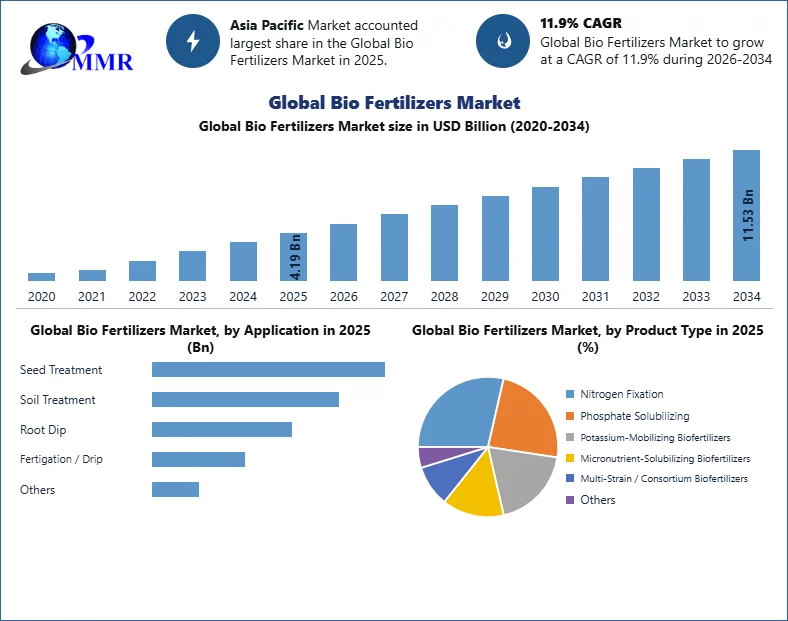

The Bio Fertilizers Market size was valued at USD 4.19 Billion in 2025, and the total revenue is expected to grow at CAGR of 11.9 % from 2026 to 2032, reaching nearly USD 11.53 Billion.

The MMR Biofertilizers Market report comprehensively covers the complete regulatory, demand, and value-chain ecosystem, including region-wise regulatory frameworks and compliance requirements, microbial strain approvals, quality and labeling standards, and organic certification norms. It analyzes global adoption trends, consumption patterns, and crop-wise demand drivers, supported by detailed production, sourcing, and trade dynamics. The report further evaluates pricing trends, technology innovations, distribution effectiveness, ESG and sustainability impacts, and the end-to-end biofertilizer supply chain, providing stakeholders with a holistic, decision-ready market assessment.

Bio Fertilizers Market Overview:

Global Bio Fertilizers Market was valued at US$ 4.19 Bn. in 2025. Microbes are increasingly being used in bio fertilizers, demonstrating their promise for sustainable farming and food safety. Over the forecast period, the market for bio fertilizers is expected to be driven by rising food safety concerns. Bio fertilizer is a chemical made up of live microorganisms that aid plant growth by increasing the amount of nutrients available to it. It enhances soil nutrients or makes them physiologically accessible for plants when applied to seed, soil, or plants. Bio fertilizers are essential in natural farming, hence the market is growing steadily all over the world. Farmers are increasingly using nitrogen-fixing bio fertilizers in the cultivation of high-demand crops including wheat, rice, and soybeans. These bio fertilizers can help to balance nitrogen levels in the soil, allowing plants to grow properly.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

The biofertilizers market in 2025 is showing steady demand as farmers, input suppliers, and governments focus on improving soil fertility, reducing chemical fertilizer dependence, and supporting sustainable crop production. Biofertilizers are relatively easier to manufacture through local microbial production systems, so domestic companies are expected to remain important suppliers in many countries. Their use is increasing across food crops such as cereals, pulses, oilseeds, fruits, vegetables, and rice because repeated cultivation and intensive farming are reducing soil nutrition and increasing the need for biological nutrient restoration. Biofertilizers help improve nitrogen fixation, phosphorus solubilization, nutrient availability, and soil microbial activity, making them a practical tool for long-term productivity. Government support for organic farming, natural farming, balanced nutrient use, and reduced fertilizer losses is also strengthening adoption; India’s National Mission on Natural Farming focuses on improving soil health and reducing input costs, while the EU targets lower nutrient losses and reduced fertilizer use by 2030. As a result, the market is expected to grow steadily, supported by rising demand for residue-free food, climate-resilient agriculture, and cost-effective soil health solutions.

Bio Fertilizers Market Dynamics:

Growth in the organic food industry: Due to growing health concerns, consumers are becoming increasingly concerned about food safety issues, rising residue levels in food, and environmental issues. As a result of their increased awareness, they have begun to prefer chemical-free foods. As a result, major supermarket chains like Wal-Mart and Cosco are expanding their organic food product lines. Many developed countries' restaurants are now offering organic food menus to cater to health-conscious customers. As the organic food industry grows, so does demand for bio fertilizers and organic manures, which are required for organic farming.

Environmental and technological constraints: Bio fertilizers have a short shelf life and are highly susceptible to contamination. When exposed to high temperatures, the microorganisms used as bio fertilizers become non-viable. As a result, it's critical to keep them in a cool, dry location. The survival of microorganisms during storage is a major challenge in agricultural inoculation technology; other challenges include culture medium, physiological state of microorganisms when harvested, dehydration process, rate of drying, temperature maintenance during storage, and inoculant water activity. Microbes' shelf-life is influenced by these challenges.

Lack of awareness & low adoption rate of bio fertilizers: Farmers' lack of understanding about bio fertilizers poses a market barrier in undeveloped and developing countries. Chemical fertilizers are preferred because they are simple to use. This can be traced back to a lack of knowledge and training. The established nature of the chemical fertilizer market is also one of the reasons for the slow adoption of bio fertilizers, as conventional fertilizer companies have a diverse product portfolio and a well-established distribution network. Furthermore, because the market is highly fragmented at the regional level, there is a growing lack of awareness of the various brands. This lack of knowledge is causing consternation among the public.

Bio Fertilizers Market segment analysis:

Based on the Product Type, in 2025, nitrogen-fixing biofertilizers hold the dominant share due to their widespread use in cereals, pulses, and oilseeds to enhance soil nitrogen availability and reduce chemical fertilizer dependence. Phosphate-solubilizing biofertilizers follow, driven by their ability to improve phosphorus uptake in nutrient-deficient soils. Potassium-mobilizing biofertilizers are gaining traction with rising focus on balanced fertilization and soil health. Micronutrient-solubilizing biofertilizers address trace element deficiencies and support crop quality improvements. Multi-strain or consortium biofertilizers are the fastest-growing segment, as they offer synergistic benefits, higher efficiency, and adaptability across diverse crops, while other biofertilizers maintain limited adoption for niche or region-specific applications.

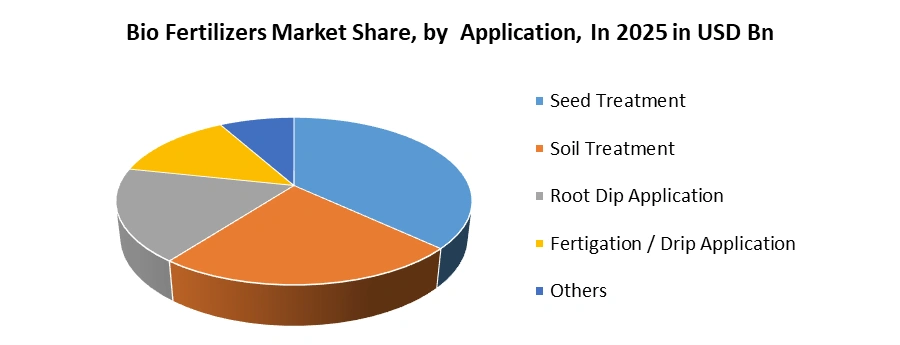

Based on Application, in 2025, seed treatment dominated Bio Fertilizers Market due to its cost-effectiveness, ease of application, and high efficiency in improving early-stage crop establishment. Soil treatment follows, supported by its widespread use in restoring soil microbial balance and enhancing long-term soil fertility. Root dip application is commonly adopted in transplant crops such as vegetables and horticulture, ensuring direct microbial contact with plant roots. Fertigation or drip application is gaining momentum with the expansion of precision agriculture and micro-irrigation systems, enabling uniform nutrient delivery. Other application methods account for a smaller share, primarily catering to specialized crops and localized farming practices.

Based on Crop Type, in 2025, the cereals and grains segment had the highest volume share 76.4%. For proper development, cereals and grains require a significant amount of bio fertilizer. Studies conducted worldwide have revealed that Azotobacter inoculation results in increased development and growth in cereal and grain crops, thereby reducing nitrogen requirements. Furthermore, phosphate-solubilizing bacteria and Azoteobacter inoculation showed to be highly effective bio fertilizers in terms of crop yield for the healthy development of wheat. When these are used for cereal and grain production, they produce a lot of vegetation and a lot of photosynthesis.

During the forecast period of 2025 to 2034, oilseeds and pulses are anticipated to grow at the fastest rate in terms of volume in the bio fertilizer market, with a CAGR of 12.2 %.Growing global demand for soybean, sunflower, and groundnuts is seen as a key benefitting element for the product's use in the oilseeds and pulses sector. Furthermore, several microbiological developments in finding the appropriate composition of bio fertilizers for application in wheat cultivation among main cereals & grains cultivation are expected to drive demand during the forecast period.

Based on Source, the Global Biofertilizers Market is segmented into Microbes, Plant Extracts, and Others. The Microbes segment held the largest Global Biofertilizers Market share in 2025. The growth of this segment is driven by the widespread use of beneficial microorganisms such as bacteria, fungi, and algae that naturally improve nutrient availability and soil health. Microbial biofertilizers enhance nitrogen fixation, phosphorus solubilization, and potassium mobilization while promoting plant growth and resistance to environmental stress. Continuous research in microbial biotechnology and increasing demand for sustainable crop nutrition solutions continue to strengthen the leadership of the microbes segment.

Based on Form, the Global Biofertilizers Market is segmented into Liquid, Powder/Dry, Carrier Based, Encapsulated/Gel Based, and Others. The Liquid segment held the largest Global Biofertilizers Market share in 2025. Liquid biofertilizers are widely preferred because they offer longer shelf life, higher microbial viability, easy application, and uniform distribution across crops. They are compatible with modern irrigation systems, including drip and fertigation, allowing efficient nutrient delivery while minimizing wastage. Increasing adoption of precision agriculture and improved formulation technologies continue to drive the demand for liquid biofertilizers worldwide.

Based on Microorganism Type, the Global Biofertilizers Market is segmented into Rhizobium, Azotobacter, Azospirillum, Pseudomonas, Bacillus, VAM, and Others. Rhizobium held the largest Global Biofertilizers Market share in 2025. Rhizobium bacteria are extensively used in leguminous crops because of their exceptional nitrogen-fixing capability through symbiotic association with plant roots. These microorganisms improve soil fertility, increase crop yields, and reduce the need for chemical nitrogen fertilizers. Rising cultivation of pulses, soybean, and other legume crops, along with growing awareness of sustainable farming practices, continues to reinforce the dominance of the Rhizobium segment.

Based on Farming System, the Global Biofertilizers Market is segmented into Conventional Farming, Organic Farming, Sustainable/Regenerative Farming, and Others. Conventional Farming held the largest Global Biofertilizers Market share in 2025. Although conventional agriculture continues to utilize synthetic fertilizers, farmers are increasingly integrating biofertilizers to improve nutrient use efficiency, enhance soil health, and reduce fertilizer consumption without compromising crop yields. Government support for integrated nutrient management and increasing awareness regarding sustainable farming practices have accelerated the adoption of biofertilizers within conventional farming systems, making this segment the largest contributor to the market.

Bio Fertilizers Market Recent Development:

Bio Fertilizers Market Regional Insight:

The objective of the report is to present a comprehensive analysis of the global Bio Fertilizers market to the stakeholders in the industry. The past and current status of the industry with the forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all the aspects of the industry with a dedicated study of key players that include market leaders, followers, and new entrants.

PORTER, PESTEL analysis with the potential impact of micro-economic factors of the market have been presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the industry to the decision-makers.

The report also helps in understanding the global Bio Fertilizers market dynamics, structure by analyzing the market segments and projects the global Bio Fertilizers market size. Clear representation of competitive analysis of key players by product, price, financial position, product portfolio, growth strategies, and regional presence in the global Bio Fertilizers market make the report investor’s guide.

Bio Fertilizers Market Scope: Inquire before buying

| Global Bio Fertilizers Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 4.19 Bn. |

| Forecast Period 2026 to 2034 CAGR: | 11.9% | Market Size in 2034: | USD 11.53 Bn. |

| Segments Covered: | by Product Type | Nitrogen Fixation Phosphate Solubilizing Potassium-Mobilizing Biofertilizers Micronutrient-Solubilizing Biofertilizers Multi-Strain / Consortium Biofertilizers Others |

|

| by Form | Liquid Carrier-based |

||

| by Microbe Type | Rhizobium Azotobacter Azospirillum Pseudomonas Bacillus VAM Others |

||

| by Crop Type | Cereals & Grains Oilseeds & Pulses Fruits & Vegetables Plantation Crops (Tea, coffee, rubber) Fiber & Industrial Crops (cotton, sugarcane, jute) Others |

||

| by Farming System | Conventional Farming Organic Farming Sustainable / Regenerative Farming |

||

| by Application | Seed Treatment Soil Treatment Root Dip Application Fertigation / Drip Application Others |

||

Bio Fertilizers Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Bio Fertilizers Market, Key Players are

- Novozymes A/S

- Rizobacter Argentina S.A.

- IPL Biologicals Limited

- UPL Limited

- Bayer CropScience LLC

- Syngenta AG

- AgriLife

- BASF SE

- National Fertilizers Limited (NFL)

- Gujarat State Fertilizers & Chemicals Ltd. (GSFC)

- Symborg (Corteva Biologicals)

- American Vanguard Corporation

- Bioceres Crop Solutions Corp.

- Mapleton Agri Biotec Pty Ltd.

- Biolchim SpA

- Toopi Organics

- Biopartner sp. z o.o.

- EuroChem Group AG

- Agrocare Canada

- Anuvia Plant Nutrients

- Nurture Growth Bio Inc.

- Greenbelt Fertilizers Ltd.

- ETG Inputs Holdco Limited

- Certis Biologicals (Mitsui & Co.)

- AMVAC Chemical Corporation

- Nutri-Tech Solutions

- Lallemand Inc.

- BioConsortia

- Clean & Green Recycling Corp.

- Suståne Natural Fertilizer, Inc.

Others

Frequently Asked Questions:

1] What segments are covered in the Bio Fertilizers Market report?

Ans. The segments covered in the Bio Fertilizers Market report are based on Product Type, Form, Microbe Type, Crop Type, Farming System, Application and region

2] Which region is expected to hold the highest share of the Bio Fertilizers Market?

Ans. The Asia Pacific region is expected to hold the highest share of the Bio Fertilizers Market.

3] What is the market size of the Bio Fertilizers Market by 2034?

Ans. The market size of the Bio Fertilizers Market by 2034 is USD 11.53 Bn.

4] What is the growth rate of the Bio Fertilizers Market?

Ans. The Global Bio Fertilizers Market is growing at a CAGR of 11.9 % during the forecasting period 2026-2034.

5] What was the market size of the Bio Fertilizers Market in 2025?

Ans. The market size of the Bio Fertilizers Market in 2025 was USD 4.19 Bn.