Automotive Polycarbonate Glazing Market Size by Vehicle Type, Technology, Application, Region, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

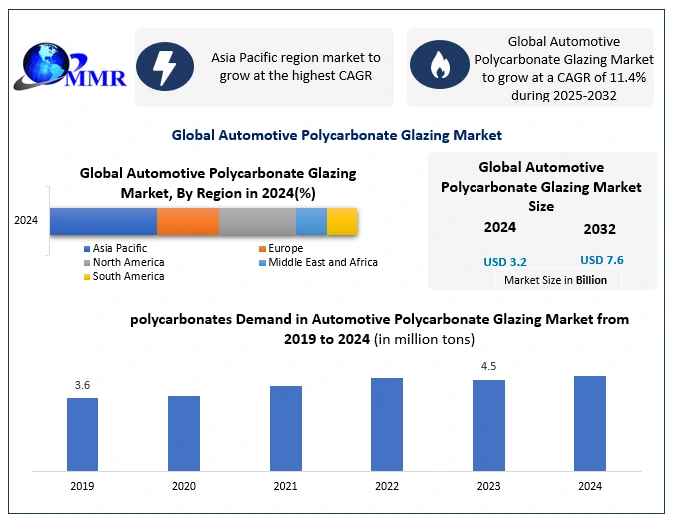

The Global Automotive Polycarbonate Glazing Market is estimated to be valued at USD 3.2 Billion in 2024. The market is expected to reach USD 7.6 Billion by 2032, exhibiting a compound annual growth rate (CAGR) of 11.4% from 2025 to 2032.

Global Automotive Polycarbonate Glazing Market Overview

The Automotive Polycarbonate Glazing Market is a rapidly growing segment of the automotive industry, offering innovative, lightweight alternatives to traditional glass for applications such as side and rear windows, panoramic sunroofs, windshields, and roof panels. This market provides a wide range of benefits, including significant weight reduction, up to 50% compared to glass, which contributes to improved fuel efficiency and extended battery range in electric vehicles (EVs), enhanced impact resistance, greater design flexibility for futuristic vehicle architectures, and the ability to integrate smart functionalities like head-up displays, embedded sensors, and ambient lighting systems. As environmental regulations tighten and automakers strive to meet increasingly stringent CO₂ emission standards, polycarbonate glazing emerges as a key enabler of energy-efficient, sustainable vehicle design. The market presents various emerging trends in the automotive polycarbonate glazing industry, driven by growth factors and multiple opportunities, and the major shareholding companies. To know about the Research Methodology:-Request Free Sample Report

To know about the Research Methodology:-Request Free Sample Report

Global Automotive Polycarbonate Glazing Market Dynamics

The Increasing Demand for Lightweight Vehicles to Boost the Automotive Polycarbonate Glazing Market Growth

A major driver boosting the growth of the automotive polycarbonate glazing market in 2024 is the increasing demand for lightweight vehicles aimed at improving fuel efficiency and reducing carbon emissions. One of the most significant influencing factors in this market is the need to lower vehicle weight, especially in electric and hybrid vehicles, where weight reduction directly translates to longer battery range and enhanced energy efficiency. Polycarbonate glazing, which is up to 50% lighter than traditional glass, plays a crucial role in achieving these goals.

• For instance, in February 2024, Covestro AG announced a strategic collaboration with BMW Group to develop advanced panoramic roofs and side windows using its Makrolon polycarbonate for upcoming EV models. This glazing not only reduces weight but also offers UV protection, design flexibility, and structural integrity.

• Similarly, Tesla and Lucid Motors have adopted polycarbonate materials in sunroofs and rear quarter windows to enhance efficiency and performance. In China, automakers like NIO and BYD are incorporating polycarbonate glazing into their EV designs to meet stringent national fuel consumption and emission standards.

Furthermore, the European Union’s CO strict ₂ fleet targets for 2025 are accelerating the shift toward lighter automotive components. These developments collectively highlight how increasing regulatory pressures, sustainability goals, and consumer demand for energy-efficient vehicles are acting as major influencing factors, significantly boosting the automotive polycarbonate glazing market growth in 2024.

Integration of Smart and Functional Glazing Technologies in Next-Generation Vehicles

A significant opportunity emerging in the automotive polycarbonate glazing market in 2024 is the increasing integration of smart and functional glazing technologies in next-generation vehicles. As automakers push toward advanced driver assistance systems (ADAS), connected car features, and enhanced user experience, polycarbonate glazing is being leveraged not just for weight reduction, but also as a multi-functional platform for embedding advanced features. This includes infrared (IR) filtering, head-up displays (HUDs), embedded antennas, solar control coatings, and electrochromic shading capabilities. These functionalities are difficult or costly to implement with conventional glass, positioning polycarbonate as a preferred alternative.

• For example, in early 2024, SABIC unveiled a new grade of LEXAN polycarbonate resin tailored for curved, large-area automotive windows that can integrate sensor transparency zones and optical clarity for LiDAR and camera systems.

• Similarly, Teijin Limited is expanding its development of polycarbonate composites that support adaptive lighting systems and interactive displays within glazing structures.

The growing trend of panoramic roofs, wrap-around windshields, and embedded lighting in EVs and luxury vehicles further underscores this shift. Automakers such as Mercedes-Benz and Hyundai have begun testing advanced polycarbonate panels with touch-sensitive and ambient lighting features. This convergence of automotive design innovation and digital technology is creating a lucrative opportunity for manufacturers and suppliers in the polycarbonate glazing space. As demand grows for smart mobility and immersive cabin experiences, polycarbonate glazing is poised to become a critical enabler of next-generation vehicle architecture, thereby offering strong potential for market expansion and differentiation.

Global Automotive Polycarbonate Glazing Market Segmentation

By Vehicle Type:

In 2024, within the Automotive Polycarbonate Glazing Market, the passenger vehicles segment represents the dominant category within the vehicle type, accounting for approximately 73.22% of total market share. This dominance is driven by the increasing production of electric and hybrid passenger cars, where polycarbonate glazing plays a critical role in achieving vehicle lightweighting objectives, improving energy efficiency, and meeting stringent global emission regulations.

• Leading automotive manufacturers such as Tesla, BMW, and BYD have integrated polycarbonate glazing into models like the Model Y, Neue Klasse series, and Han EV respectively, particularly for applications such as sunroofs, sidelites, and rear windows.

By Technology:

Under the technology segment, conventional polycarbonate glazing holds the largest market share, estimated at around 38%, due to its widespread use across economy and mid-range vehicles where cost-efficiency and regulatory compliance are key considerations. However, sun control glazing emerges as the sub-dominant and fastest-growing technology, with an estimated XX% market share in 2024. The increasing need for solar heat mitigation, UV protection, and thermal comfort in vehicles—particularly in electric and premium models, is accelerating its adoption.

• Automotive OEMs such as Mercedes-Benz and Hyundai have incorporated advanced sun control polycarbonate solutions in models like the EQE and IONIQ 6 to reduce solar heat gain and optimize interior climate control.

Global Automotive Polycarbonate Glazing Market Regional Analysis

In 2024, Asia-Pacific continues to be the dominant region in the global automotive polycarbonate glazing market, accounting for the major share in the market. This leadership is primarily driven by the strong presence of automotive manufacturing hubs in countries such as China, Japan, South Korea, and India. Among these, China plays a pivotal role, being the world’s largest producer and consumer of automobiles, particularly electric vehicles (EVs). The growing demand for lightweight and fuel-efficient vehicles, along with government incentives for EV adoption, has significantly accelerated the integration of polycarbonate glazing in automotive design.

In addition, the presence of global polycarbonate suppliers and local tier-1 automotive component manufacturers in the region fosters rapid technology adoption. OEMs such as BYD, SAIC Motor, Hyundai, and Toyota have increasingly adopted polycarbonate for applications such as sunroofs, sidelites, and backlites, enhancing vehicle energy efficiency and safety standards. Moreover, stringent emission regulations, rising consumer preference for modern vehicle aesthetics, and growing R&D investments in lightweight materials are major growth factors boosting the market in this region. Asia-Pacific’s cost advantages in production and supply chain localization further reinforce its dominant segment position in the market.

Europe represents the sub-dominant region in the automotive polycarbonate glazing market. The market growth in Europe is primarily driven by the region’s stringent carbon emission regulations under the European Union Green Deal, which promote the adoption of sustainable and lightweight materials in vehicle manufacturing. Countries such as Germany, France, Sweden, and the Netherlands are at the forefront of this transition, with strong incentives for electric mobility and a growing emphasis on vehicle efficiency and innovation. Germany, in particular, stands out due to the concentration of premium automotive brands such as BMW, Mercedes-Benz, and Audi, all of which are integrating advanced polycarbonate glazing into their high-performance electric and hybrid models. Polycarbonate is increasingly used in panoramic roofs, sun control glazing systems, and advanced driver assistance display panels, supporting the region’s push toward smart and sustainable mobility. Furthermore, Europe's well-established automotive testing and certification ecosystem supports the development of regulatory-compliant polycarbonate applications, which are now being integrated into both new vehicle platforms and modular redesigns. Growth factors in Europe include high R&D investment in next-generation materials, increasing EV sales, consumer demand for luxury and comfort features, and regulatory alignment with CO₂ fleet emission targets for 2025. These dynamics contribute significantly to boosting the market across the region, reinforcing its position as the sub-dominant segment in the global market.

Global Automotive Polycarbonate Glazing Market Competitive Landscape

The competitive landscape of the automotive polycarbonate glazing market in 2024 is characterized by moderate to high competitive rivalry among leading global materials manufacturers and specialized suppliers. The market is driven by innovation in lightweight glazing technology, compliance with safety and emission standards, and rising adoption of electric and smart vehicles. Among the key players, Covestro AG (Germany), SABIC (Saudi Arabia), and Teijin Limited (Japan) emerge as the top three companies holding major shares in the global market, supported by their advanced product portfolios, global manufacturing footprint, and long-standing OEM partnerships.

Covestro AG holds a leading position in the market with its well-established Makrolon polycarbonate product line, which is widely used for sunroofs, sidelites, panoramic roofs, and rear glazing applications. With a strong market presence across Europe, North America, and Asia-Pacific, Covestro maintains high brand equity due to its emphasis on sustainable innovation, durability, and UV-resistant polycarbonate sheets. The company has entered strategic collaborations with major OEMs such as BMW and Volkswagen to develop advanced glazing for EVs. In 2024, Covestro reported robust demand growth in its automotive division, generating an estimated USD XX billion in revenue from its mobility and transportation segment. Its early focus on circular materials and compliance with EU automotive directives gives it a competitive edge.

SABIC, a global materials science leader, is another major market shareholder, recognized for its LEXAN resin solutions, tailored for high-performance automotive glazing. The company’s innovations in solar-control, impact-resistant, and LiDAR-transparent polycarbonate glazing place it at the forefront of demand from electric and autonomous vehicle manufacturers. SABIC's strong presence in North America and Asia, especially in China’s fast-growing EV segment, contributes significantly to its automotive revenue, which crossed USD XX billion in 2024 for automotive thermoplastics. The company enjoys a high degree of brand loyalty and OEM preference due to its ability to offer tailored, scalable solutions, and its vertically integrated supply chain further strengthens its market positioning.

Teijin Limited, with its Panlite polycarbonate resins and advanced composite solutions, is also a key competitor in this market. The company has made strategic investments in polycarbonate composite technologies that enhance design flexibility and structural integrity, particularly in sunroof panels and backlite applications. Teijin’s collaborations with Japanese and European automakers such as Toyota, Nissan, and Stellantis underline its strong OEM relationships. While slightly smaller in market share compared to Covestro and SABIC, Teijin is rapidly gaining ground, driven by its innovation in lightweight structural glazing and sustainability-focused product development. In 2024, its automotive-related polycarbonate segment generated estimated revenues of around USD XX million, with high demand noted in Asia-Pacific and Europe.

Global Automotive Polycarbonate Glazing Market Recent Developments

| Company | Date | Recent Developments |

| Covestro AG (Germany) | 2024 | Expanded Makrolon PC production in Europe & Asia to support EV glazing demand. Launched IR-filtering PC sheets for sunroofs and rear windows |

| 2023 | Partnered with European OEMs to replace glass with PC in side and rear windows; achieved up to 40% weight reduction. | |

| SABIC (Saudi Arabia) | 2023–2024 | Introduced LEXAN™ glazing with UV/optical clarity for curved automotive windows. Partnered with Asian OEMs for sensor-compatible PC modules |

| Teijin Limited (Japan) | 2023 | Launched Panlite PC glazing for autonomous vehicles; supports signal transparency. Partnered with Honda, Toyota for PC rear/quarter windows. |

| Freeglass GmbH (Saint-Gobain) | 2024 | Scaled production of hybrid glazing combining PC and glass. Collaborated on polycarbonate tailgates for European EV startups. |

| Webasto Group (Germany) | 2024 | Integrated polycarbonate panoramic sunroof modules with embedded lighting in EV platforms. Developed thermal/acoustic coatings for PC roof systems. |

Automotive Polycarbonate Glazing Market Scope: Inquire before buying

| Automotive Polycarbonate Glazing Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 3.2 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 11.4% | Market Size in 2032: | USD 7.6 Bn. |

| Segments Covered: | by Vehicle Type | Passenger Vehicles Commercial Vehicles |

|

| by Technology | Sun Control Glazing Hydrophobic Glazing Switchable Glazing Conventional |

||

| by Application | Windscreen Sidelites Backlite Sunroof Rear quarter glass |

||

Global Automotive Polycarbonate Glazing Market, By Region

North America (United States, Canada, and Mexico)

Europe (UK, France, Germany, Italy, Spain, Russia, Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Rest of Asia Pacific)

Middle East and Africa (South Africa, Saudi Arabia, UAE, Rest of the Middle East &Africa)

South America (Brazil, Argentina, Rest of South America)

Global Automotive Polycarbonate Glazing Market key players

1. Covestro AG (Germany)

2. SABIC (Saudi Arabia)

3. Teijin Limited (Japan)

4. Mitsubishi Chemical Group (Japan)

5. Trinseo S.A. (USA)

6. Lotte Chemical Corporation (South Korea)

7. Chi Mei Corporation (Taiwan)

8. Idemitsu Kosan Co., Ltd. (Japan)

9. LG Chem (South Korea)

10. Formosa Chemicals & Fibre Corp. (Taiwan)

11. Exolon Group (Germany) – formerly part of Covestro

12. Plazit Polygal Group (Israel)

13. Brett Martin Ltd. (UK)

14. Gallina Group (Italy)

15. SHEPLEY (SFS Group) (UK)

16. Palram Industries (Israel

17. 3A Composites GmbH (Germany)

18. PolyOne (Avient Corporation) (USA)

19. Webasto Group (Germany)

20. Saint-Gobain Sekurit (France)

21. AGC Inc. (Asahi Glass Co.) (Japan)

22. Fuyao Glass Industry Group (China)

23. NSG Group (Nippon Sheet Glass) (Japan)

24. Magna International (Canada)

25. Plastic OBnium (France)

26. Gentex Corporation (USA)

27. Flex-N-Gate Group (USA)

28. KRD Sicherheitstechnik GmbH (Germany)

29. Vision Systems (France)

30. SABIC IP China Ltd. (China)

Frequently Asked Questions

Q1. What is the current size of the automotive polycarbonate glazing market?

Ans: As of 2024, the market is valued at USD 3.2 billion and is expected to grow at a CAGR of 11.4% through 2032.

Q2. Which segment dominates the market by application?

Ans: Sunroofs are the leading application segment, driven by growing demand for panoramic and lightweight roof systems in EVs and premium vehicles.

Q3. Who are the major players in the market?

Ans: Key players include Covestro AG, SABIC, and Teijin Limited, accounting for the largest share due to strong OEM partnerships and innovation.

Q4. What is driving the growth of this market?

Ans: Growth is driven by vehicle lightweighting, electric vehicle expansion, fuel efficiency regulations, and rising demand for advanced glazing technologies.

Q5. Which region holds the largest market share?

Ans: Asia-Pacific is the dominant region, led by high automotive production in China, Japan, and South Korea.