Automotive Crankshaft Market Size by Crankshaft Type, Material Type, Vehicle Type, and Region - Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2032

Overview

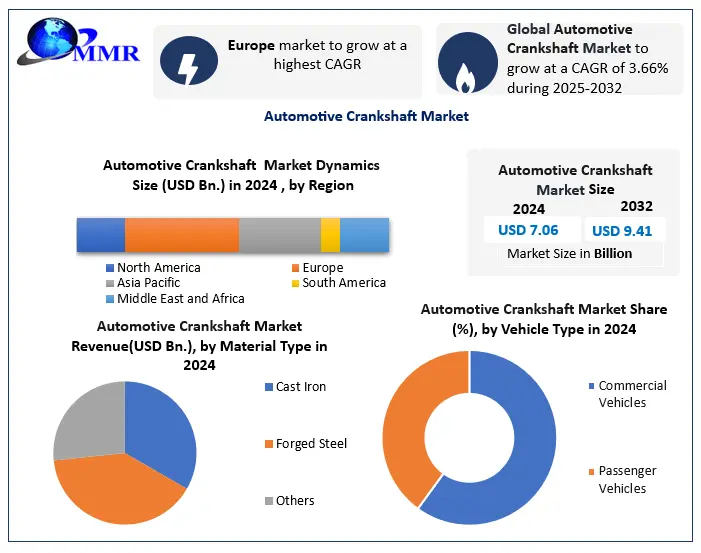

Global Automotive Crankshaft Market size was valued at USD 7.06 Bn. in 2024, and the total Automotive Crankshaft Market revenue is expected to grow by 3.66% from 2025 to 2032, reaching nearly USD 9.41 Bn.

Automotive Crankshaft Market Overview

In terms of design, the Automotive Crankshaft Market differentiates between flat-plane and cross-plane crankshafts based on application requirements. Flat-plane crankshafts are primarily used in high-performance vehicles due to their lower mass and superior high-RPM capabilities. In contrast, cross-plane crankshafts are more common in passenger and commercial vehicles because they provide smoother engine operation, making them ideal for everyday use.

From a materials perspective, the Automotive Crankshaft Market segments demand based on cost and performance. Cast iron crankshafts are widely used in price-sensitive regions and lower-end vehicles due to their affordability. Meanwhile, forged steel crankshafts, known for their high durability, shock tolerance, and corrosion resistance, are preferred in premium and heavy-duty vehicle segments.

In terms of vehicle type, the Automotive Crankshaft Market is dominated by the commercial vehicle segment, which accounts for the majority of global demand. Crankshafts with increased thickness offer enhanced durability, optimized weight, tighter dimensional tolerances, and improved mechanical performance characteristics essential for such applications.

Material innovation is another key trend in the Automotive Crankshaft Market. Billet steel and composite materials are being increasingly considered for niche, high-performance, and racing applications. These advancements align with a broader industry trend toward light weighting and fuel efficiency to meet global regulatory and performance standards.

Regional dynamics also play a significant role in shaping the Automotive Crankshaft Market. In the Asia-Pacific region, cast iron crankshafts remain the preferred, cost-effective choice. In contrast, developed regions such as North America and Europe are witnessing increased adoption of advanced forged steel crankshafts, driven by stricter emission norms and higher performance expectations. As technological advancements and regulatory pressures continue to shape the landscape, the Automotive Crankshaft Market is expected to evolve further. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Automotive Crankshaft Market Dynamics:

Increasing Demand for Passenger and Commercial Vehicles to Drive Automotive Crankshaft Market Growth

The growing demand for passenger and commercial vehicles worldwide is a significant driver of the automotive crankshaft market. As more vehicles are manufactured and sold, there is a proportional demand for crankshafts to power their engines. For example, the growth of the middle-class population in emerging economies like India and China has led to a surge in automotive sales, driving the demand for crankshafts. Technological advancements in engine design, such as the development of high-performance and fuel-efficient engines, drive the demand for advanced crankshaft materials and designs. For instance, lightweight and durable materials like forged steel and billet crankshafts are increasingly used in modern engines to enhance performance and fuel efficiency. The automotive industry's focus on achieving higher fuel efficiency and reducing emissions is propelling innovations in engine components, including crankshafts. Lightweight crankshafts with improved balance and reduced friction contribute to better fuel economy and lower emissions, aligning with stringent regulatory standards such as Euro 6 and CAFE standards in the United States.

High-Performance and Replacement Crankshafts to Drive Automotive Crankshaft Market Growth

The growth of the automotive aftermarket, driven by increasing vehicle ownership and aging vehicle fleets, boosts the demand for replacement crankshafts. Aftermarket suppliers like Continental offer OE-quality replacement crankshafts, providing customers with reliable options for engine repairs and maintenance. The growing popularity of motorsports and performance tuning enthusiasts drives demand for high-performance crankshafts capable of withstanding extreme operating conditions. Companies like Tomei Engineering cater to this market segment by offering specialized forged billet crankshafts designed for racing and performance applications

Advanced Engine Technology Systems in Commercial Vehicles

| Technology System | Description | Benefits |

| Common rail injection | Higher injection pressure, Maximum around 2700 to 3000 bar | Smaller and faster fuel droplets, improved air entrainment, and mixing reduce soot emission. Offset the drawbacks of a high EGR rate 1.1% FC reduction |

| Higher compression ratio | Optimization of combustion chamber design impacting the combustion process | Theoretical benefits in BTE; different values are reported from 2% to 15% in HD engines |

| Peak cylinder pressure (PCP) | There is a trend towards higher PCPs. Volvo in Super Truck II has claimed 250 bar PCP, and other teams also utilized high PCPs (not quantified) | Contributes to the higher efficiency and BMEP |

| Advanced turbocharging and downsizing | Variable geometry turbine (VGT), Multi-stage turbocharging Twin scroll housing Double scroll housing | 2.9% FE benefit Improvement in transient and part load conditions |

| Variable Valve Actuation (VVA) | Variable cam phasing, valve lift, and cylinder deactivation Valvetrain adjusts as a function of engine load and speed | Limited benefits in diesel engines Enables late inlet valve closure (Miller cycle) Provides thermal management system of engine aftertreament system (EATS) by changing exhaust gas temperature FC benefits in the part load of gasoline engines |

| Turbocompounding | Using a turbine to recover the exhaust energy Connected directly to the crankshaft or powers a generator | 1.8% to 4% FE improvement |

| WHR | Conversion of dissipated engine heat to mechanical or electrical energy Closed Rankine cycle Thermo-electric generators | BTE improvement 3% to 4% FE improvement |

| Engine friction reduction | Piston skirt and piston ring friction reduction: Advanced materials/lubricants | 1.5% FE improvement |

| On-demand coolant and oil pump | Decoupling the pumps from the engine when they are not needed, Electronically controlled viscous coupling or on/off friction clutch | 0.8% FE improvement |

Increasing adoption of electric vehicles (EVs) to drive the Automotive Crankshaft Market

While the shift toward electric vehicles reduces the demand for traditional crankshafts in EV powertrains, it also presents opportunities in hybrid vehicles where internal combustion engines coexist with electric motors. Crankshafts in hybrid vehicles require design modifications to accommodate integrated electric motor components, opening new avenues for crankshaft manufacturers. Beyond automotive applications, crankshafts find use in various industrial machinery and equipment, including generators, pumps, and compressors. The growth of industries like construction, mining, and energy drives demand for heavy-duty crankshafts capable of powering large-scale machinery. With engine components being critical for vehicle performance and safety, there is a growing emphasis on the quality and reliability of crankshafts. Manufacturers that adhere to strict quality standards and offer warranties and certifications gain a competitive edge in the Automotive Crankshaft Market, earning the trust of automotive OEMs and aftermarket customers.

The globalization of automotive supply chains has led to increased collaboration between OEMs and crankshaft suppliers across different regions. This trend fosters innovation, knowledge sharing, and cost-effective manufacturing practices, driving market growth through efficient supply chain management. Government initiatives promoting automotive manufacturing, such as subsidies, tax incentives, and investment in infrastructure, stimulate market growth by encouraging OEMs to expand production capacity and invest in advanced technologies. For example, initiatives aimed at promoting electric vehicle adoption indirectly benefit the Automotive Crankshaft Market, including crankshaft manufacturers supplying hybrid vehicles.

High Manufacturing Costs and Materials to Restrain the Automotive Crankshaft Market

The automotive crankshaft market faces restraints due to high manufacturing costs associated with advanced materials and precision machining processes. For instance, the production of forged billet crankshafts requires costly raw materials and specialized equipment, limiting their widespread adoption and affordability for mass-market vehicles. Crankshafts undergo complex design and engineering processes to meet performance and durability requirements. These challenges increase development time and costs, especially for innovative crankshaft designs catering to specific vehicle applications, such as high-performance sports cars or heavy-duty trucks. Compliance with stringent regulatory standards, particularly regarding emissions and fuel efficiency, poses constraints on crankshaft manufacturers. Meeting these standards necessitates investments in research and development for advanced materials and manufacturing techniques, adding to production costs and time-to-market pressures.

Skilled Labor Shortage and Raw Material Price Volatility to Create Automotive Crankshaft Market Challenges

The automotive industry's reliance on skilled labour for precision machining and assembly tasks presents a restraint in the crankshaft market. Shortages of skilled workers, exacerbated by demographic shifts and technological advancements, lead to production delays, quality issues, and increased labour costs, impacting overall manufacturing efficiency. Fluctuations in raw material prices, such as steel and aluminium, pose challenges for crankshaft manufacturers. Sudden price increases disrupt production planning and profitability, as material costs account for a significant portion of overall manufacturing expenses. This volatility necessitates effective supply chain management and risk mitigation strategies to maintain competitiveness in the Automotive Crankshaft Market.

Automotive Crankshaft Market Segment Analysis:

Based on Crankshaft, Cross-plane crankshafts dominated the Automotive Crankshaft Market in 2024, due to their widespread adoption in most internal combustion engines. Cross-plane crankshafts offer smoother engine operation and better NVH (Noise, Vibration, and Harshness) control compared to flat-plane designs, making them the preferred choice for mainstream vehicles. Flat-plane crankshafts are gaining traction, particularly in high-performance and sports car applications, where their lightweight construction and superior high-end power delivery are valued.

With advancements in materials and manufacturing techniques, flat-plane crankshafts are expected to witness increased adoption, especially in niche automotive segments seeking enhanced performance characteristics. The adoption of crankshaft types depends on various factors, including engine configuration, vehicle type, and performance requirements. While cross-plane crankshafts remain dominant in conventional engines powering everyday vehicles, flat-plane designs are increasingly favoured in performance-oriented applications where engine responsiveness and high RPM capabilities are paramount. As automotive technology evolves and consumer preferences shift towards more efficient and powerful engines, the demand for flat-plane crankshafts is projected to grow, challenging the dominance of traditional cross-plane designs in certain Automotive Crankshaft Market segments.

Automotive Crankshaft Market Regional Analysis

Europe dominated the automotive crankshaft market in 2024, driven by advancements in automobile engines and a strong automotive manufacturing base. Europe's established automotive industry, coupled with stringent emissions regulations, fosters continuous innovation in engine technology, creating a robust demand for crankshafts. Europe's focus on electric vehicle (EV) development and consumer purchasing power is expected to further stimulate market growth, as demand for Automotive Crankshafts may rise alongside EV sales.

The Asia-Pacific region has emerged as a key growth market for Automotive Crankshafts. With the rapid growth of the automotive industry, particularly in countries like China and India, Asia-Pacific is expected to witness substantial growth in the demand for crankshafts. Factors such as increasing vehicle production, rising disposable incomes, and urbanization contribute to the region's Automotive Crankshaft Market growth. Moreover, the shift towards electric and hybrid vehicles in the Asia-Pacific region presents new opportunities for crankshaft manufacturers to cater to evolving engine requirements. For instance, China's ambitious electric vehicle goals and government support for EV adoption drive investments in electric powertrain components, including crankshafts.

Automotive Crankshaft Market Competitive Landscape:

The automotive crankshaft industry is characterized by a of competition from specialized crankshaft producers, with leaders in technology and OEM contracts including Thyssenkrupp AG (Germany), Bharat Forge (India), and Maschinenfabrik ALFING Kessler GmbH (Germany). Thyssenkrupp dominates the forged steel market in the premium segment, providing crankshafts to most of the large European OEMs and developing lightweight and alternative materials for hybrid applications.

Bharat Forge is well established in cost-sensitive markets and has established a position in commercial vehicles with low-cost chain-driven designs and the costs associated with these parts. Bharat Forge is pursuing opportunities in EV range-extender applications in the traction markets sales.

NSI Crankshaft (U.S.A.) and Arrow Precision (U.K.) focus on design, material, and manufacturing innovation for high-performance motorsports and luxury OEM crankshafts, including the advanced use of billet and 3D-printed architecture. The industry is evolving rapidly with the advances in electrification, where there is a focus on advanced design. Nippon Steel (Japan) is targeting compact engine hydrogen combustion engine crankshaft designs with very high strength. Regional players such as TIANRUN CRANKSHAFT (China) with low-cost manufacturing are estimated to penetrate emerging markets, while the European traditionalists are projected to continue to dominate OEM precision engineering in the high-value segments. All players across the segments will see an upswing in applied R&D investments in materials science (e.g., carbon fibre, nanocomposites) and smart manufacturing technologies that are required to address the evolving efficiency and emissions targets.

Automotive Crankshaft Market Key Developments:

• Thyssenkrupp AG (Germany) – May 2025: Thyssenkrupp presented its next-gen forged hybrid crankshaft. It combines high-strength steel with carbon-fiber reinforcement, reducing weight by 20% while keeping durability and strength. It is made to optimize turbocharged hybrid engines and has integrated mounting points for sensors to continuously monitor performance. It's a component that the company intends to sell to major EU OEMs with scaled production starting in 2026.

• Bharat Forge (India) – April 2025 Bharat Forge presented their crankshaft series, "E-Forged" crankshaft, which is optimized for range-extender EVs and specially designed hydrogen combustion engines. Using AI-led forging methods, these crankshafts achieve 15% higher on fatigue resistance, and are 30% faster to produce than conventional crankshafts. Bharat Forge has contracts to supply crankshafts to Tata Motors and Volvo for use in their commercial vehicle applications.

• NSI Crankshaft (USA) – March 2025 NSI Crankshaft introduced the 3D-printed titanium billet crankshaft for hypercars and motorsports. This crankshaft configuration has an increasing weight advantage over traditional steel crankshafts by nearly 25%. With a hollow-core crankshaft backbone, they reduce inertia swinging loads, improve engine performance, and response. The crankshaft is already being utilized by two Formula 1 teams, with limited consumer release now set for late 2025.

• Nippon Steel (Japan) – February 2025 Nippon Steel developed a Kevlar-composite crankshaft for Toyota's hydrogen-powered engines. This crankshaft reduces weight by 10% and carries an additional 40% better corrosion resistance in comparison to conventional crankshafts. Furthermore, the design was developed with self-lubricating micro-channels in its design to provide a 12% reduction in friction losses. Mass production is expected to begin in Q4-2025.

• Maschinenfabrik ALFING Kessler (Germany) – January 2025 The company launched its "SmartForge" crankshaft

Automotive Crankshaft Market Key Trends

| Category | Key Trend | Example Product/Innovation | Market Impact |

| Lightweight Materials | Shift toward high-strength, low-weight composites | Thyssenkrupp Carbon-Fiber Hybrid Crankshaft | 20% weight reduction in performance vehicles; 15% better fuel efficiency in hybrids |

| Electrification-Ready | Designs optimized for hybrid/EV range extenders | Bharat Forge "E-Forged" Crankshaft | 60% of new R&D now targets electrified powertrains; contracts with Tata/Volvo |

| Additive Manufacturing | 3D-printed crankshafts for hyper-performance | NSI 3D-Printed Titanium Crankshaft | 25% lighter than steel; adopted by Formula 1 teams; limited consumer rollout 2025 |

Automotive Crankshafts Market Scope: Inquire before buying

| Automotive Crankshafts Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 7.06 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 3.66% | Market Size in 2032: | USD 9.41 Bn. |

| Segments Covered: | by Crankshaft | Flat Plane Cross Plane |

|

| by Material Type | Cast Iron Forged Steel Others |

||

| by Vehicle | Commercial Vehicles Passenger Vehicles |

||

Automotive Crankshafts Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Automotive Crankshaft Market Manufacturers

North America:

1. NSI Crankshaft (Headquarters: Illinois, USA)

2. Crower Cams & Equipment (Headquarters: California, USA)

3. Bryant Racing Inc (Headquarters: California, USA)

Europe:

4. Arrow Precision (Headquarters: Northamptonshire, United Kingdom)

5. Maschinenfabrik ALFING Kessler GmbH (Headquarters: Germany)

6. Rheinmetall (Headquarters: Düsseldorf, Germany)

7. Cigueñales Sanz SL (Headquarters: Spain)

Asia Pacific:

8. TIANRUN CRANKSHAFT (Headquarters: Zhejiang, China)

9. Nippon Steel Integrated Crankshaft LLC (Headquarters: Tokyo, Japan)

10. Bharat Forge Ltd (Gujarat, India)

FAQs:

1. What are the growth drivers for the Automotive Crankshaft Market?

Ans. Increasing Demand for Passenger and Commercial Vehicles is the the major driver for the Automotive Crankshaft Market.

2. What is the major Opportunity for the Automotive Crankshaft Market growth?

Ans. Increasing adoption of electric vehicles (EVs) is expected to be the major Opportunity in the Automotive Crankshaft Market.

3. Which country is expected to lead the global Automotive Crankshaft Market during the forecast period?

Ans. Europe is expected to lead the Automotive Crankshaft Market during the forecast period.

4. What is the projected market size and growth rate of the Automotive Crankshaft Market?

Ans. The Automotive Crankshaft Market size was valued at USD 7.06 billion in 2024, and the total Automotive Crankshaft Market revenue is expected to grow at a CAGR of 3.66% from 2025 to 2032, reaching nearly USD 9.41 billion.

5. What segments are covered in the Automotive Crankshaft Market report?

Ans. The segments covered in the Automotive Crankshaft Market report are by Crankshaft, Material Type, Vehicle, and Region.