Agricultural Tractors Market – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning / Landscape Review & Global Market Size Forecast to 2032

Overview

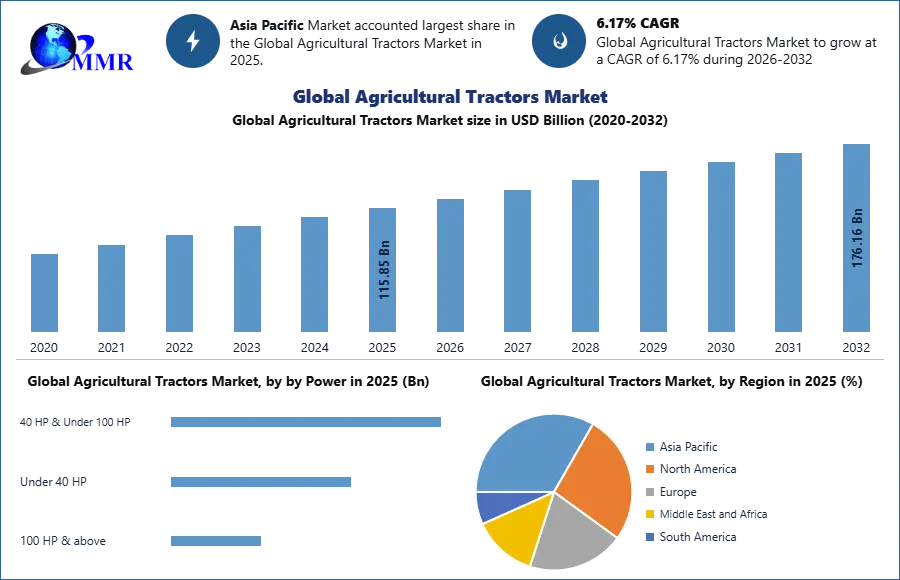

Global Agricultural Tractors Market was valued at USD 115.85 Bn in 2025 and is expected to reach USD 176.16 Bn by 2032, growing at a CAGR of 6.17% during the forecast period.

Agricultural Tractors Market Overview:

An agricultural tractor is a vehicle designed to perform essential farming tasks such as plowing, sowing, and harvesting. It powers and operates farm machinery, improving efficiency and reducing manual labor. Modern models often feature advanced technologies for precision and sustainable agriculture.

To know about the Research Methodology:-Request Free Sample Report

To know about the Research Methodology:-Request Free Sample Report

The global agricultural tractors market size is witnessing robust growth, primarily driven by the rising farm mechanization rate across developed and developing regions. Tractors are essential for plowing, tilling, sowing, harrowing, and harvesting, and their ability to pull or push various machinery enhances operational efficiency while reducing labor dependency. The integration of advanced technologies, such as GPS-guided systems, automation, autonomous tractors, and electric tractors with hybrid powertrains, is further boosting market CAGR and demand. By 2032, the agricultural sector is expected to account for 77.6% of the total tractor market, underscoring the increasing reliance on mechanized farming solutions.

The Asia-Pacific agricultural tractors market dominated in 2024, fueled by a large population of smallholder farmers, supportive government initiatives, and rapid adoption of modern agricultural technologies. Key drivers of the agricultural tractors market include labor shortages in farming, rising focus on sustainable low-emission tractors, and demand for compact tractors in fragmented landholdings, presenting opportunities for electric tractors, hybrid models, and rental/leasing services. Major agricultural tractor competitors, such as John Deere, CNH Industrial, AGCO Corporation, and Kubota, dominate due to technological innovation, extensive distribution networks, localized manufacturing, and diverse product offerings. Emerging trends include autonomous tractors, precision agriculture integration, telematics-enabled connectivity, and the adoption of smart tractors.

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 20 January 2026 | The Business Research Company | Published data confirming the Agricultural Tractors market reached $80.93 billion in 2025, driven by a surge in autonomous farming practices. | This growth sets a benchmark for the 5.2% CAGR expected through 2030, highlighting a shift toward low-emission and precision-compatible platforms. |

| 05 February 2026 | AGCO Corporation | Reported full-year 2025 results with net sales of $10.1 billion, noting a moderate demand shift toward precision and smart-farming technologies. | The company successfully navigated market softness in high-horsepower categories by focusing on Fendt and Massey Ferguson technology integration. |

| 09 February 2026 | Astute Analytica | Identified a 2025–2026 trend where autonomous retrofit kits reached 30% adoption for existing tractor fleets. | This decoupling of technology from new sales allows mid-sized farms to access AI-driven steering without the high cost of new 2026 machinery. |

| 08 October 2025 | MarketsandMarkets | Released analysis projecting the Autonomous Tractors Market to accelerate at a 24% CAGR, reaching significant commercial scale by 2028. | The rapid uptake is attributed to LiDAR and vision technologies that solve the acute global shortage of skilled labor on large farms. |

| 12 November 2025 | VST Tillers Tractors Ltd | Unveiled its first electric-powered farm implements and tillers at EIMA Agrimach India 2025 to support zero-emission small-scale farming. | This launch targets the sub-50 HP segment, which remains critical for mechanization in Asia-Pacific and emerging markets. |

| 07 January 2025 | John Deere | Launched a suite of new autonomous machines at CES 2025 specifically designed for large-scale agricultural and commercial operations. | The commercialization of these GPS-guided platforms aims to optimize resource utilization and fuel efficiency for 2025–2026 harvests. |

Agricultural Tractors Market Dynamics

Compact and Versatile Tractors to boost Agricultural Tractors Market Growth

The agricultural tractors market is propelled by the compact size, affordability, and multifunctional capabilities of tractors, particularly those under 40 horsepower (HP), which are widely used for general farming in emerging economies. In developed regions, the 41–99 HP tractor segment is experiencing strong growth due to rising demand for mechanized farming and mid-size utility tractors. Four-wheel-drive (4WD) tractors enhance adoption by offering superior traction and operational flexibility for tasks such as tilling, hauling, mowing, and loader applications. These factors collectively increase productivity, adoption rate, and agricultural tractor sales across diverse environments, particularly in high-demand regions like India, China, Europe, and North America.

In 2024, Mahindra & Mahindra launched the Yuvraj 215 DI tractor in India, a compact and fuel-efficient model under 40 horsepower, specifically designed for small and marginal farms, boosting mechanization in rural regions.

| Global Agricultural Tractors Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 115.85 USD Billion |

| Forecast Period 2026-2032 CAGR: | 6.17% | Market Size in 2032: | 176.16 USD Billion |

| Segments Covered: | by Power | 40 HP & Under 100 HP Under 40 HP 100 HP & above |

|

| by Drive type | 2-Wheel Drive 4-Wheel Drive |

||

| by operation mode | Manual tractor Autonomous tractor |

||

| by Agriculture Application | Harvesting Seed Sowing Irrigation Others |

||

Precision Farming Adoption to Create Opportunities in the Agricultural Tractors Market

The increasing adoption of precision farming tractors presents a significant growth opportunity for the agricultural tractors market. Farmers are increasingly investing in tractors equipped with GPS-enabled auto-steering, IoT sensors, and AI-powered systems that optimize the use of water, seeds, fertilizers, and machinery, thereby improving productivity and crop quality. Precision farming enables efficient resource management and addresses global food demand challenges by maximizing yields with minimal input. As awareness and implementation of these technologies expand, the demand for technology-driven, smart tractors is expected to grow, providing manufacturers with opportunities to innovate and capture high-value segments.

For instance, John Deere introduced precision-enabled tractors with GPS-guided auto-steering in India, helping farmers optimize input use and improve crop yields, demonstrating growing demand for technology-driven farming solutions.

High Costs and Financing Dependence to Limit Agricultural Tractors Market Expansion

Despite growing adoption, the high upfront costs of tractors remain a key challenge, particularly for small and marginal farmers in developing economies. This cost barrier drives dependence on tractor rental and leasing services as well as government-supported financial programs, such as farm loan waivers and subsidized credit schemes. While these measures improve accessibility, inconsistent policy support or limited rental infrastructure can hinder consistent agricultural tractor sales growth. Rising labor costs, fuel expenses, and operational expenditures further constrain farmers’ ability to purchase machinery outright, moderating direct tractor market penetration in certain regions.

Agricultural Tractors Market Segment Analysis

In 2025, the Power segment shows the highest demand for tractors in the 40 HP & Under 100 HP category. Tractors in this range are widely adopted by small- to medium-sized farms due to their balance of affordability, versatility, and fuel efficiency. While Under 40 HP tractors are preferred for small-scale operations and specialized farming, 100 HP & Above tractors are increasingly deployed for large-scale commercial farming and mechanized operations. Overall, mid-range tractors represent the largest revenue share and are projected to drive growth during the forecast period.

Based on Drive Type, 4-Wheel Drive (4WD) tractors are the fastest-growing segment in 2025. They offer enhanced traction, stability, and efficiency in diverse terrains, making them ideal for commercial farming and challenging agricultural conditions. 2-Wheel Drive (2WD) tractors remain widely used in regions with flat terrain and smaller farm sizes but show slower growth compared to 4WD variants. The demand for 4WD tractors reflects the trend toward mechanization and higher productivity requirements in modern agriculture.

Agricultural Tractors Market Regional Analysis

Based on Region, Asia Pacific leads the global agricultural tractors market in 2025, driven by high agricultural activity, government subsidies, and rising adoption of mechanized farming in countries like India and China. North America shows strong demand, supported by advanced farming practices, large-scale commercial farms, and increasing adoption of autonomous and high-power tractors. Europe maintains moderate growth with focus on precision agriculture and sustainability initiatives. South America and MEA exhibit steady demand, influenced by mechanization trends, agricultural expansion, and government support programs.

Agricultural Tractors Market Competitive Landscape

The global agricultural tractor market in 2025 is characterized by robust growth, fueled by government initiatives and technological advancements. In India, the government's reduction of Goods and Services Tax (GST) on farm equipment from 12–18% to 5% has made tractors more affordable, lowering retail prices by 7–13%. This policy aims to promote mechanization and reduce labor dependency, aligning with the government's goal to enhance agricultural productivity. Additionally, state-level schemes like the Sub-Mission on Agricultural Mechanization (SMAM) are providing subsidies for the purchase of modern farming equipment. These efforts are contributing to the expansion of the tractor market, as farmers increasingly adopt mechanized solutions to improve efficiency and yield.

Leading agricultural tractor manufacturers include John Deere, Mahindra & Mahindra, CNH Industrial, Kubota, and AGCO Corporation, all focusing on localized manufacturing, dealer network expansion, and technology innovation. Recent developments include investments in autonomous tractor R&D, electric tractor launches, and partnerships for precision farming solutions, solidifying their presence in the global agricultural tractors market share.

Deere & Company and Mahindra & Mahindra are leading players in the global agricultural tractor market by combining innovation, sustainability, and localized strategies. Deere focuses on AI-driven autonomous tractors and eco-friendly equipment, supported by an extensive dealer network, while Mahindra emphasizes affordable, durable tractors with strong rural distribution and tailored financing, strengthening its market presence in India.

Agricultural Tractors Market Key Trends

Smart Farming with IoT-Enabled Tractors

Agricultural tractors are getting smarter with IoT integration, offering real-time monitoring, predictive maintenance, and data-driven insights. This trend is revolutionizing precision farming by boosting productivity, lowering operational costs, and empowering farmers with next-gen connectivity solutions.

Electric & Autonomous Tractors Reshaping Agriculture

The rise of electric and driverless tractors is transforming traditional farming into a sustainable, tech-driven industry. Electric tractors cut fuel costs and emissions, while autonomous tractors tackle labor shortages, enabling 24/7 field operations and maximizing agricultural efficiency.

Compact Tractors Driving Small Farm Growth

Compact tractors are emerging as a game-changer for small farmers and urban agriculture. With versatility, affordability, and multifunctional use, these tractors are fueling mechanization in peri-urban and fragmented landholdings, making modern farming accessible to wider segments.

Agricultural Tractors Market Scope: Inquire Before Buying

Agricultural Tractors Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players /Competitor Profiles Covered in the Global Agricultural Tractors Market Report from a Strategic Perspective.

- Deere & Company

- AGCO Corporation

- CNH Industrial N.V.

- CLAAS KGaA mbH

- SDF Group

- Argo Tractors S.p.A.

- Zetor Tractors a.s.

- Minsk Tractor Works (MTZ)

- Ursus S.A.

- Carraro SpA

- Goldoni S.p.A.

- Arbos Group

- Mahindra & Mahindra

- Kubota Corporation

- Yanmar Co. Ltd.

- Daedong Industrial Co.Ltd. / Kioti

- Iseki & Co. Ltd.

- LS Mtron Co.Ltd.

- TYM Corporation

- Escorts Limited

- TAFE — Tractors and Farm Equipment Ltd.

- International Tractors Limited

- Lovol Heavy Industry

- YTO Group Corporation

- Qilu Machinery

- Zoomlion Heavy Industry Science & Technology Co. Ltd.

- Eicher Motors Limited

- Dongfeng Motor Corporation

- Hattat Tarım Makinaları A.Ş.

- Agrale S.A.