Aerospace Parts Manufacturing Market by Product Type, Material, Aircraft Type and Region - Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2034

Overview

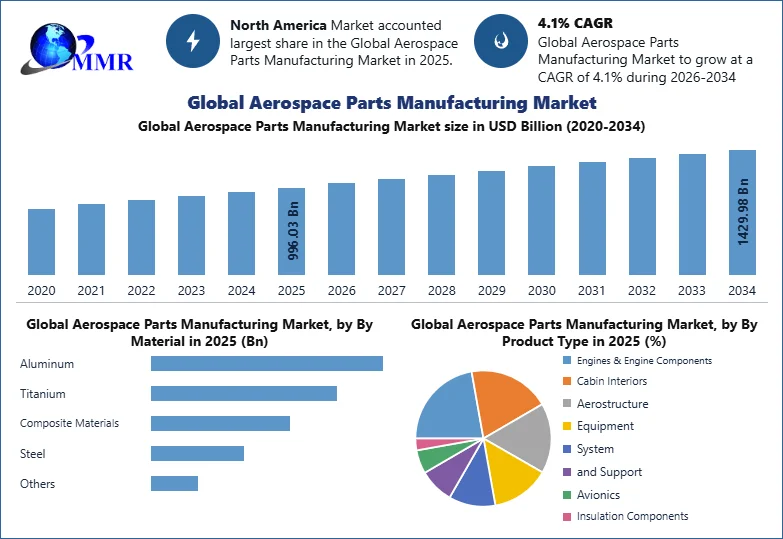

The Aerospace Parts Manufacturing Market size was valued at USD 996.03 Billion in 2025 and the total Aerospace Parts Manufacturing revenue is expected to grow at a CAGR of 4.10% from 2025 to 2034, reaching nearly USD 1429.98 Billion by 2034.

Aerospace Parts Manufacturing Market Overview:

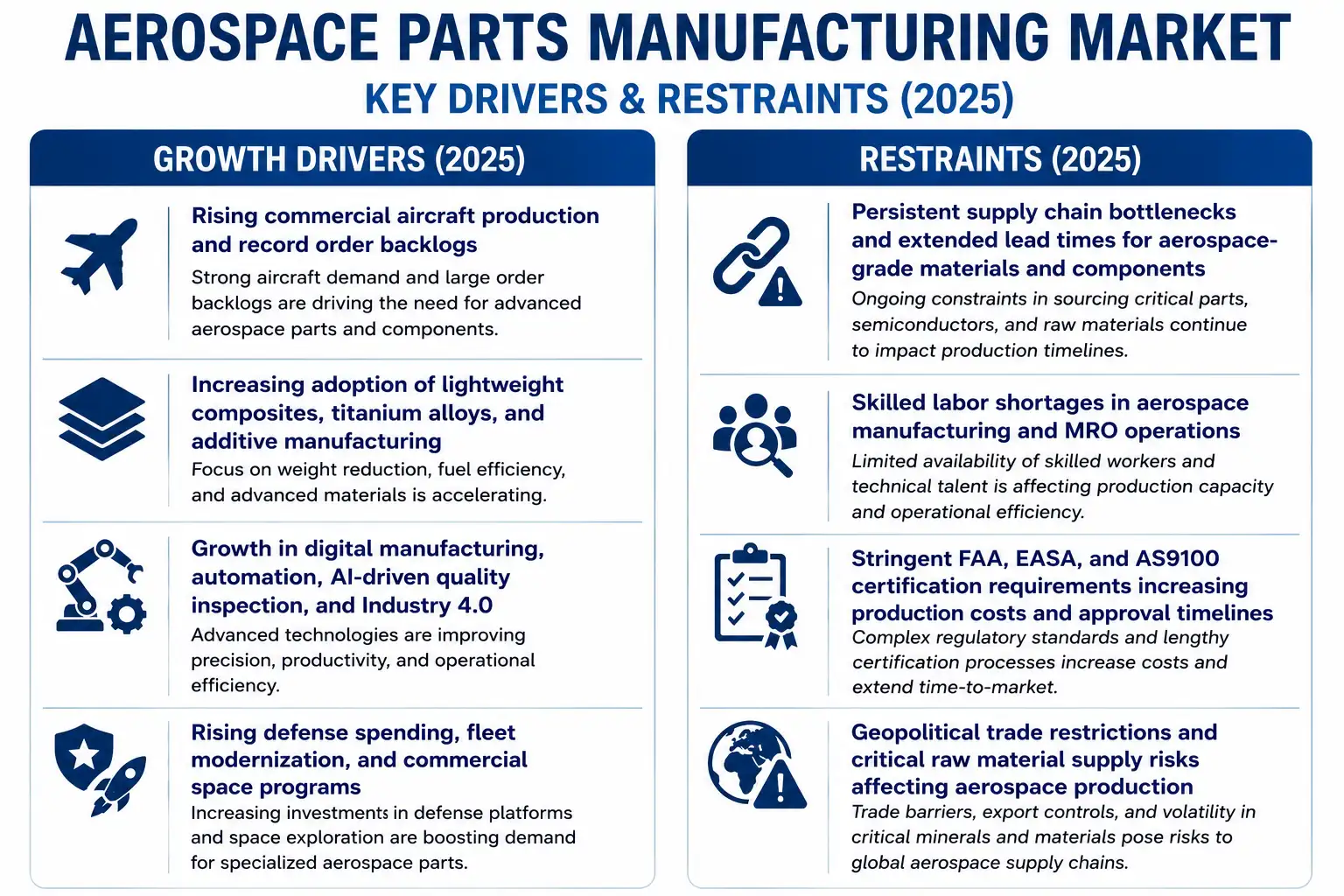

Growth in the Aerospace Parts Manufacturing Industry is being fueled by an increase in the production of commercial aircraft, initiatives for military modernization, and growth in investments in the space industry across the globe. Growth in the number of airline passengers, expansion in their fleets, and retirement of older aircraft are causing a need for aerospace parts that include engines, aerostructures, landing gear, avionics casings, and flight control components. Companies that produce aerospace components are relying on advanced manufacturing processes like additive manufacturing (3D printing), CNC machining, automation, and digital manufacturing to increase efficiency and performance while reducing weight. Passenger traffic in the global airline industry, as per International Air Transport Association (IATA), surpassed the pre-pandemic mark in 2024 and continues to grow, providing support to production and demand in the aftermarket. Further, as per Boeing's Commercial Market Outlook, there will be a requirement for more than 43,000 new commercial aircraft in the next 20 years.

In addition, the market is also driven by increased defense procurements, greater investments in domestic aerospace manufacturing, and rigorous certification standards laid out by aviation authorities such as the Federal Aviation Administration (FAA) and the European Union Aviation Safety Agency (EASA). Manufacturers have been concentrating on lightweighting material such as titanium alloy, aluminum-lithium alloy, and carbon fiber composite to increase fuel economy and lower emissions while meeting the changing environmental regulations. Also, the increasing usage of technologies related to Industry 4.0, digital twin, quality prediction systems, and automation in inspection will increase the precision of manufacture and reliability of the supply chain. In addition, the increased maintenance, repair, and overhaul activities along with the production of future generation commercial aircraft, military aircraft, and spacecraft will ensure sustained demand for aerospace parts during the forecast period.

Aerospace Parts Manufacturing Market Executive Summary

Every decade transforms what aerospace vehicles can achieve; the next decade will redefine what their parts can deliver. The Global Aerospace Parts Manufacturing Market is standing at the intersection of precision manufacturing, aircraft engineering, and advanced aerospace technology. Between 2025 and 2034, the market is expected to grow from USD 996.03 Bn. to USD 1429.98 Bn.by 2034, at a CAGR of 4.10%.

Aerospace parts are not just mechanical and structural components; they have now become a strategic node linking aircraft systems, avionics engineering, and digital aerospace manufacturing solutions. Deeper technological transformation: commercial aircraft require lightweight and modular aerospace components, defense applications are driving precision aerospace parts for military applications, and space exploration is demanding aerospace parts for satellites and propulsion systems.

North America leads with technological innovation and established aerospace hubs, while Asia-Pacific emerges as the fastest-growing ecosystem, powered by the expansion of the Indian aerospace industry, Bangalore aerospace companies, and Hyderabad aerospace companies. The market’s pulse is accelerating as aircraft manufacturing companies, AS9100-certified manufacturers, and precision aerospace component suppliers shift from conventional materials to advanced aerospace composites and smart aerospace structures.

To know about the Research Methodology :- Request Free Sample Report

Aerospace Parts Manufacturing Market Objective & Scope

The goal of this report is to equip OEMs, Tier 1 and Tier 2 suppliers, aftermarket integrators, investors, and regulators with a comprehensive understanding of the aerospace parts manufacturing market’s transformation into a high-precision, technology-driven sector.

Scope includes:

• Market evolution (2021–2024) and forecast till 2034

• Demand segmentation by Product Type, Material, and Aircraft Type

• Cost structure and margin of products across OEM and aftermarket suppliers

• Technological disruption – precision aerospace components, custom aerospace components, aerospace parts for electric aircraft

• Regional intelligence – North America, Europe, APAC, MEA, and South America

• Competitive benchmarking, value chain shifts, and regulatory frameworks

Aerospace Parts Manufacturing Market Definition & Strategic Context

Aerospace parts are not only passive mechanical or structural components. They are critical interfaces connecting mechanical, electronic, and digital systems across aircraft, defense vehicles, drones, and satellites.

The modern aerospace parts market extends across:

• Aerospace parts for commercial aircraft – high-volume precision components

• Aerospace parts for military applications – rugged and mission-critical systems

• Aerospace parts for space exploration – propulsion, avionics, and satellite systems

• Unmanned aerial vehicle (UAV) parts – lightweight and autonomous-compatible

• Electric and supersonic aircraft components – optimized for new aviation technologies

These parts integrate into aircraft engines, flight control systems, landing gear systems, hydraulic and pneumatic systems, and cabin interiors, expanding from traditional manufacturing to digital aerospace manufacturing and smart component integration.

Aerospace Parts Manufacturing Market Dynamics: The Evolution Story

The industry narrative is one of reinvention — a shift from rugged mechanics to responsive aerospace technology.

1. Commercial Aviation & Defense Expansion

Global commercial aircraft and defense production continues to grow, pushing demand for aerospace parts manufacturing companies in India, the USA, and Europe. Defense programs, UAVs, and satellite initiatives are driving precision requirements and increased reliance on custom aerospace components.

2. Technological Advancement & Material Innovation

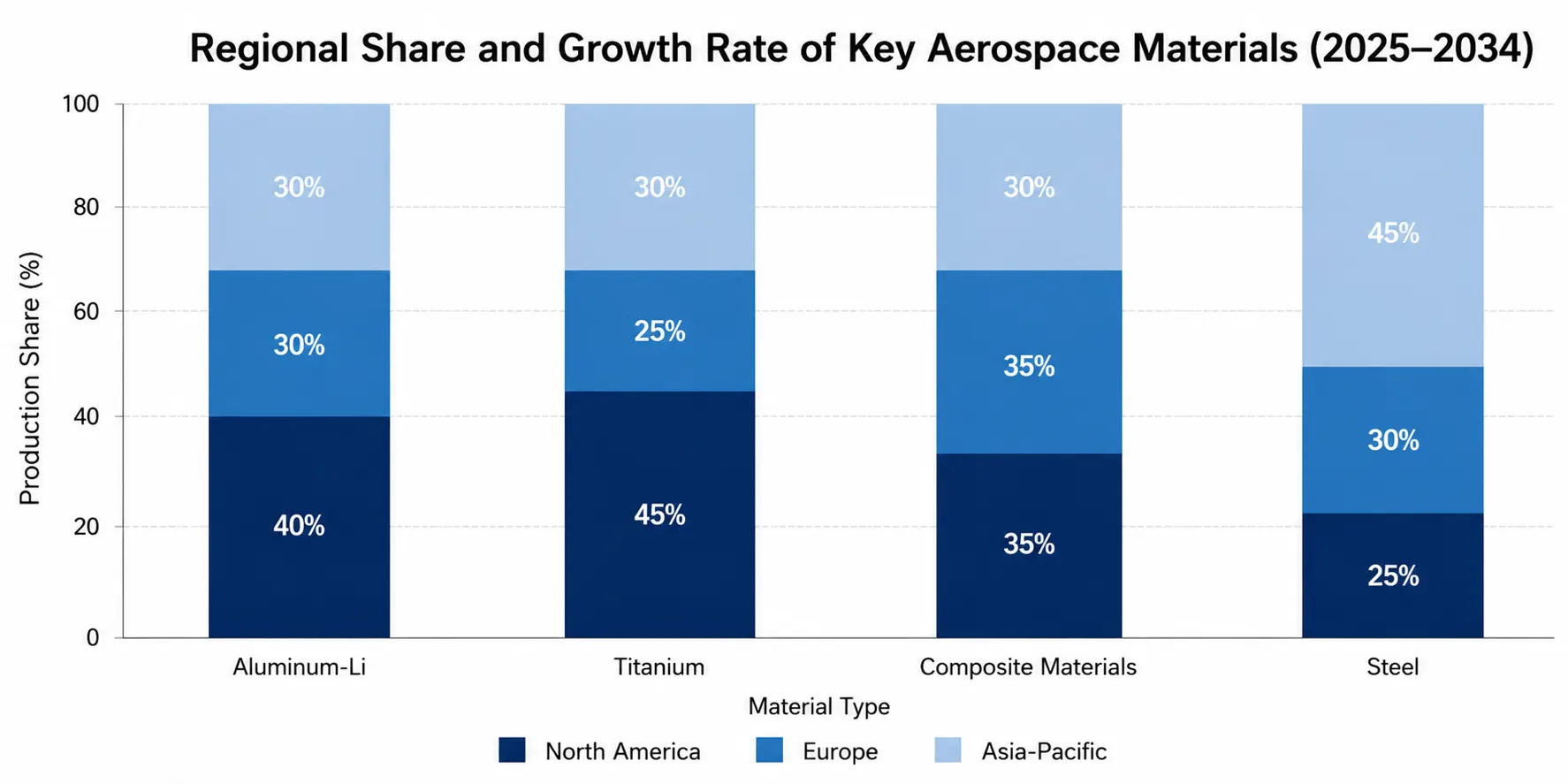

Traditional aluminum and titanium alloys are being supplemented with aerospace composites and advanced aerospace materials. Aerospace structures are now designed to integrate sensors, avionics, and lightweight designs, reducing weight while improving performance.

3. Smart Integration & Digital Manufacturing

Aerospace parts suppliers are adopting AS9100 certified manufacturing, digital twin modeling, and predictive maintenance technologies. AI-driven quality control, automated aerospace machining services, and real-time telemetry integration are becoming standard.

4. Sustainability & Circular Manufacturing

Manufacturers are shifting to green materials, recyclable components, and precision manufacturing processes that reduce emissions and waste. ESG compliance is becoming a key differentiator for top aerospace companies worldwide.

Aerospace Parts Manufacturing Market Growth Drivers & Restraints 2025

Regional Intelligence: Global Growth, Local Momentum

Europe – The Innovation Hub

Europe accounts for a significant share of aerospace engineering revenue, driven by strong OEMs, regulatory standards, and defense programs. Aircraft companies in Germany, France, and the UK lead in integrating aerospace parts for propulsion systems, flight control systems, and aerospace parts for avionics systems.

North America – The Technology Leader

The US remains the epicenter of aerospace innovation. Demand for aerospace parts for military applications, space exploration, and UAVs is high. Companies leverage precision aerospace component suppliers and advanced aerospace composites for next-generation aircraft.

Asia-Pacific – The Growth Engine

China, India, and Japan are rapidly expanding their aircraft manufacturing companies and regional aerospace hubs. The Indian aerospace industry, centered around Bangalore aerospace companies and Hyderabad aerospace companies, is witnessing exponential growth. Demand for aerospace parts for commercial aircraft, UAVs, and electric aircraft is soaring.

GCC & South America – Emerging Markets

Investment in defense programs, UAVs, and satellite manufacturing is driving aerospace parts for military applications and space exploration. Emerging players are focusing on precision aerospace components to compete globally.

Aerospace Parts Manufacturing Market Revenue & Market Share (%) by Region 2024

Cost Structure & Profitability Lens

In a typical aerospace parts unit:

• Raw Materials (Aluminum, Titanium, Composites, Steel, Others): XX%

• Labor & Assembly: 20–25%

• Electrical/Avionics Components: 10–15%

• Gross Margin: xx% OEM | xx% Aftermarket

High-value components, such as aerospace parts for propulsion systems and aerospace parts for avionics systems, deliver gross margins 2–3x higher than standard structural components.

Aerospace Parts Manufacturing Market Competitive Landscape

Airbus Defence and Space, Boeing Defense, Space & Security, Spirit AeroSystems, GKN Aerospace, and Safran form a powerful, complementary competitive set in the Aerospace Parts Manufacturing Market. Airbus and Boeing dominate platform-level aerostructures and systems integration; Spirit AeroSystems excels in high-volume fuselage and wing assemblies; GKN focuses on advanced composite structures and engine components for civil and defense OEMs; Safran leads in propulsion systems, nacelles, and avionics subsystems—together driving innovation in composites, propulsion, and digital manufacturing.

The market is moderately consolidated with leading players including top aerospace companies in North America, Europe, and Asia. Focus areas include:

• Technological innovation in aerospace composites and aerospace structures

• Expansion of aerospace parts manufacturing companies in India, USA, UK

• Integration of custom aerospace components and digital manufacturing

Emerging competitors in Asia and Eastern Europe are driving innovation in lightweight aerospace parts and precision aerospace machining services, applying pressure on incumbents.

Regulatory & Technological Integration

• Safety and certification standards such as AS9100, FAA regulations, and EASA standards govern aerospace parts manufacturing.

• Industry is moving towards digital twin simulations, predictive AI maintenance, and IoT-enabled aerospace parts for unmanned aerial vehicles and space exploration systems.

Aerospace Parts Manufacturing Market Forecast & Financial Outlook

The global Aerospace Parts Manufacturing Market is forecast to grow from USD 956.81 Bn. to USD 1,319.57 Bn. by 2032, representing a CAGR of 4.10%.

Regional split:

• North America: USD xx Bn (Leading Region)

• Europe: USD xx Bn

• Asia-Pacific: USD xx Bn

• MEA: USD xx Bn

• South America: USD xx Bn

Aerospace Parts Manufacturing Market Strategic Recommendations

• For OEMs: Integrate advanced aerospace components, adopt AS9100 certified manufacturing, and collaborate with precision aerospace component suppliers to maintain technological leadership.

• For Aftermarket Players: Focus on custom aerospace components, predictive maintenance services, and digital integration for retrofits and upgrades.

• For Investors: Prioritize companies innovating in aerospace parts for propulsion systems, flight control systems, and avionics systems. High ROI exists in mid-tier supplier ecosystems.

• For Policymakers: Harmonize aerospace standards, incentivize sustainable aerospace materials, and support innovation in space engineering and UAV applications.

Analyst Insight: The Next Decade of Advanced Aerospace Parts

The aerospace parts manufacturing market is no longer a back-end industrial function. Between precision engineering and digital aerospace technology, these components are shaping the future of commercial aviation, defense, and space exploration.

By 2032, every aircraft, drone, and spacecraft will rely on smart, lightweight, and precision aerospace parts, connecting data, power, and purpose in a global ecosystem of aerospace innovation.

Aerospace Parts Manufacturing Market Scope: Inquiry Before Buying

| Global Aerospace Parts Manufacturing Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 996.03 Bn. |

| Forecast Period 2026 to 2032 CAGR: | 4.10% | Market Size in 2032: | USD 1429.98 Bn. |

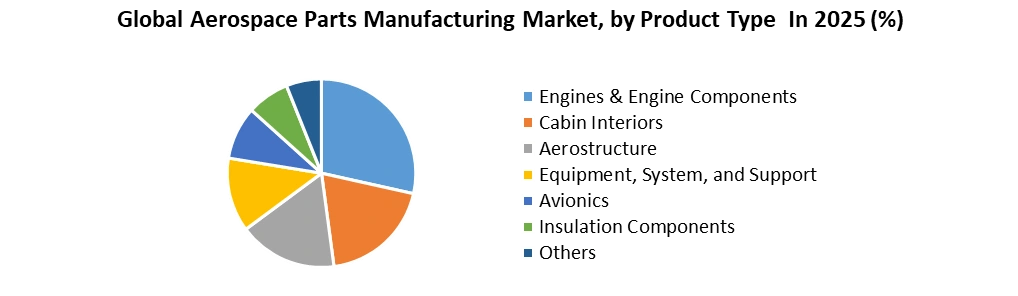

| Segments Covered: | by Product Type | Engines & Engine Components Cabin Interiors Aerostructure Equipment, System, and Support Avionics Insulation Components Others |

|

| by Material | Aluminum Titanium Composite Materials Steel Others |

||

| by Aircraft Type | Commercial Aircraft Business Aircraft Military Aircraft Others |

||

Aerospace Parts Manufacturing Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (razil, Argentina Rest of South America)

Aerospace Parts Manufacturing Market, Key Players

- Spirit Aerosystems Inc.

- GKN Aerospace

- Safran

- Honeywell Aerospace

- Rolls-Royce

- General Electric (GE Aerospace)

- Parker Aerospace

- MTU Aero Engines

- Liebherr-Aerospace

- Triumph Group

- Senior Aerospace

- Woodward, Inc.

- Thales Group

- FACC AG

- Magellan Aerospace

- Latecoere

- TAE Aerospace

- HAL (Hindustan Aeronautics Limited

- IAI (Israel Aerospace Industries)

- Patria Aviation

- COMAC

- CPI Aerostructures

- Intrex Aerospace

- Sansera

- Aequs Private Limited

- ALPHA DESIGN TECHNOLOGIES PVT LTD

- Bharat Electronics Limited

- L&T Technology Services Limited

- Tata Advanced Systems Limited

- Avantel Limited

- Collins Aerospace (Raytheon Technologies)

- Lockheed Martin Aeronautics

- Boeing Defense, Space & Security

- Airbus Defence and Space

- Leonardo S.p.A.

- Northrop Grumman Corporation

- Textron Aviation

- Dassault Aviation

- RUAG International Holding AG

- ST Engineering Aerospace Ltd

- Moog Inc.

- Eaton Aerospace

- Cobham Limited

- AAR Corp.

- Curtiss-Wright Corporation

- Ducommun Incorporated

- Kaman Corporation

- Hexcel Corporation

- Barnes Aerospace

- Senior Plc (UK)

Others

Frequently Asked Questions:

1. Which region has the largest share in the Global Aerospace Parts Manufacturing Market?

Ans: The North America region held the highest share in 2025.

2. What is the growth rate of the Global Aerospace Parts Manufacturing Market?

Ans: The Global Market is expected to grow at a CAGR of 4.10% during the forecast period 2026-2032.

3. What is the scope of the Global Aerospace Parts Manufacturing Market report?

Ans: The Global Aerospace Parts Manufacturing Market report helps with the PESTEL, PORTER, Market estimation of the forecast period, Material Analysis and Dependency Mapping, Production and Manufacturing Analysis, Pricing and Cost Structure Analysis (2025), etc.

4. Who are the key players in the Global Aerospace Parts Manufacturing Market?

Ans: The important key players in the Global Aerospace Parts Manufacturing Market are – Airbus Defence and Space, Boeing Defense, Space & Security, Spirit AeroSystems Inc., GKN Aerospace, Safran, etc.

5. What is the study period of this market?

Ans: The Global Aerospace Parts Manufacturing Market is studied from 2025 to 2032.