Connected Car Market– Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

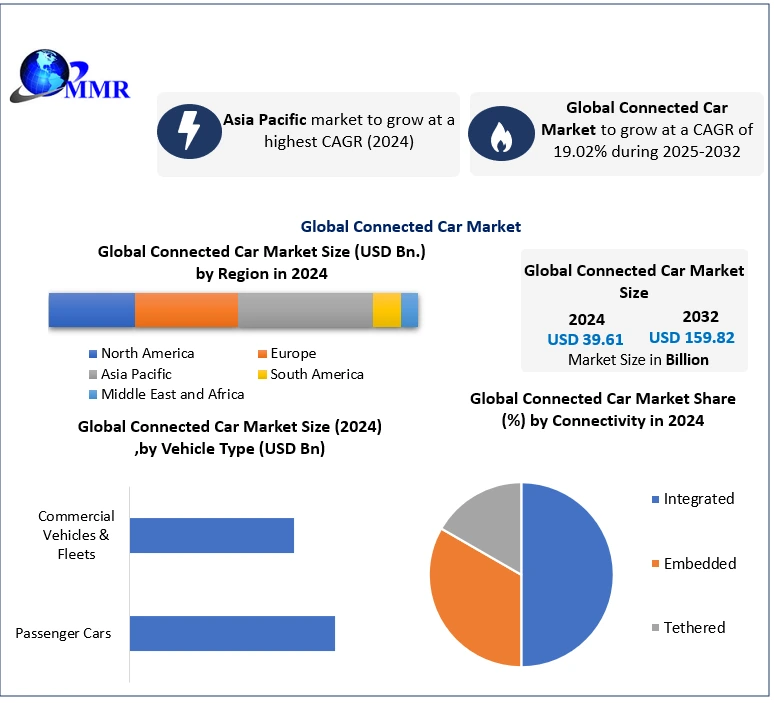

Global Connected Car Market size was valued at USD 39.61 Bn in 2024, and the total Connected Cars Market revenue is expected to grow at a CAGR of 19.02% from 2025 to 2032, reaching nearly USD 159.82 Bn

Connected Car Market Overview:

A connected car is one that has two-way communication capabilities with external systems (LAN). This allows the automobile to exchange data and provide internet access with other devices inside and outside the vehicle. Global automobile markets are already being dominated by connected vehicles. More and more automakers are implementing connected technologies into their automobiles to drive the connected car market.

This allows them to provide services more quickly and directly, such as breakdown support. It is now possible to create a wide range of cutting-edge and intelligent goods and services thanks to digitalization and the connection of automobiles, including alternatives like app-controlled breakdown help, anti-theft defense, or emergency calls in the case of an accident. Thus, connected automobiles bring value to vehicle owners in terms of safety and comfort and drive the connected car market globally.

Connected automobiles provide a unique consumer experience while bringing cost and revenue benefits to mobility organizations such as OEMs, suppliers, dealers, insurance, fleets, tech players, and others. The Connected car market covers the most recent technological advances, government regulations to promote connected features in vehicles, and the global market share of key connected car manufacturers.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Connected Car Market Dynamics:

Strategic planning and collaboration penetrating the connected car market globally.

The automobile industry is undergoing the most radical transformation in 2022. As collaborative software mobility companies, automakers must now quickly transform their organizational structures and technical capabilities. OEMs manufacture cars as well as software solutions for a more connected, individualized customer experience.

OEMs have the potential to develop new income streams and more direct interactions with their customers because of the car industry's constant evolution. OEMs face a number of challenges as a result of the shifting corporate environment, including the necessity to concentrate on services and goods outside of their core strengths and the need to increase profitability by including connectivity in their entire connected car market strategy.

OEMs are coming up with a variety of plans to take full advantage of the connected car market potential. While some OEMs are building their own ecosystem, others are forming alliances with specialized vendors. The increased connected car ecosystem is crucial for meeting the growing consumer demand of today and in the future.

The strategy for volume brands like Ford, Opel, and Volvo as well as luxury automakers like BMW, Porsche, Audi, and Mercedes varies depending on the OEM's relative market share, customer involvement, internal capabilities, innovation, and Capital investments in the connected car market.

For example, Automotive OEMs are in a challenging position as a result of the leading role that large tech companies such as Facebook, and Amazon are playing in connected car technologies. OEMs are up against a significant struggle to maintain their position of dominance in the rapidly developing ecosystem since the expertise required for connected vehicles extends beyond their core competencies. Some OEMs are actively competing with these technology companies by developing their own in-house connected car assets and capabilities to drive the connected car market.

Volkswagen is redefining itself as a digital mobility provider by making significant investments in a number of fields, including software development, autonomous driving technology, battery solutions for electric vehicles, and other mobility services. The Volkswagen Group is transitioning from a leading, worldwide provider of software-driven mobility to a vehicle manufacturer with the new Group strategy "NEW AUTO - Mobility for Generations to Come."

Additionally, in order to create the Microsoft Connected Vehicle Platform, Volkswagen has formed a strategic alliance with Cubic Telecom and Microsoft (MCVP). Volkswagen Automotive Cloud, often known as VW.AC is one of the largest specialized automotive industry clouds that VW intends to grow more quickly alongside Microsoft.

With the aim of offering connected experiences to consumers all over the world starting in 2022, VW.AC is expected to manage data from millions of cars every day. This is a key component of the Volkswagen Group’s vision to become a leading automotive software innovation.

Less than 10% of the software that runs on Volkswagen Group's cars is created by the company itself; the remainder is linked to proprietary software that is held by third parties. in an endeavor. In order to create digital technologies for linked vehicles and upcoming mobility services, certain automotive OEMs are collaborating with other OEMs by forming international alliances.

One such international collaboration is called "The Alliance," in which Group Renault, Nissan Motor Company, and Mitsubishi Motors Corporation collaborate on the next mobility technologies and solutions to drive the connected car market. More detailed strategy planning by each key players by region is covered in the report.

New opportunities and value chain analyses for new and small market players

Various new opportunities will be created as a result of the changing automotive value chain for both internal industry players and outside technology providers. By 2030, connected-car use cases may have generated more than $550 billion in value, up from around $64 billion in 2020. Players in the automotive value chain have the opportunity to improve their operations and customer services as a result of increased connectivity.

Consider the use of predictive maintenance in automobiles. Connected car Aftermarket maintenance and repair currently primarily involve following a set interval maintenance program or reactive maintenance/repair. Lack of insight into the number of cars that require maintenance within a certain time period causes inefficiencies in service planning, buying replacement parts, and inventory management, among other things. By allowing OEMs and dealers to start and oversee the maintenance process, predictive maintenance employing remote vehicle diagnostics might improve the operation.

Traditional players moving into adjacent markets and new entrants from industries outside the automotive value chain, such as communication system providers (CSPs), hyperscalers, and software developers, might both speed up value creation. Increased efficiencies and benefits from vertical integration result from players like Intel, Nvidia, and the Taiwan Semiconductor Manufacturing Company developing automotive software capabilities. In addition to speeding up value generation, new competitors can fight for a greater portion of the overall value, also creating opportunities for upcoming and smaller connected car market players.

Connected Car Market Segment Analysis:

Connected Car Market Segment Analysis:

Based on the Application, the Connected Car Market is segmented into Driver Assistance, Telematics, Infotainment, and others. Infotainment Segmented is expected to dominate the connected car market during the forecast period. Any infotainment in-dash system that can send and receive updated information wirelessly through the internet is referred to as a "connected" automobile.

These devices often have touch displays and voice control, although their features and compatibility with smartphone apps vary greatly. A connected car with built-in wireless connections can benefit from features like starting or unlocking the vehicle from anywhere, tracking teenage drivers, and enabling anti-theft features, such as remotely stopping a stolen car. Each automaker offers its own system, and there are frequently multiple different infotainment systems within a single car line. Onboard navigation systems are no longer a standard feature of connected automobile systems.

Companies like Mitsubishi have abandoned such pricey solutions in favor of letting new owners display navigation data from their phones on the in-dash display with the help of free smartphone-based navigation applications that are regularly updated.

But even without cellular service, built-in navigation devices can function. Smartphone applications won't entirely replace such services since higher-resolution built-in nav systems are required for the next semi-automated and fully autonomous driving capabilities in the connected car market.

In most infotainment systems, drivers can use a few specific smartphone apps, such as Pandora, although all-in-one apps like Apple's CarPlay are growing more common. CarPlay displays a pre-selected set of applications on the LCD screen of a connected automobile in a sequence of panels that are easy to read and operate. Apps for CarPlay include texting, music, and mapping services.

With many of the same capabilities as CarPlay, including voice control and navigation, as well as a larger selection of applications, Android Auto is Apple's response. When an Android phone is connected, all of these apps appear on the dashboard screen. Additionally, the hugely well-liked Waze live traffic and navigation app is now available for Android Auto these infotainment companies drives the connected car market globally.

On the other hand, Amazon's Alexa is designed to communicate with thousands of linked devices through a variety of instructions or "skills." It can place a pizza order, unlock locks, and switch on the lights. And now it's being utilized to link living rooms with automobiles.

The Tesla is not a typical dash-connected car, but it is one of several electric cars (EVs) that are readily accessible in Canada. With the help of a tablet, users may operate virtually all of the connected car capabilities of the automobile.

Easter eggs are another feature of the Tesla infotainment system that provides some entertainment to owning and operating a vehicle. In Santa mode, snow will fall around your car on the infotainment screen, or you may rename it. Users may even activate Camp Mode if they're feeling a little nostalgic. The infotainment screen will transition to a movie of a bonfire made of logs after 10 minutes of inactivity and many more features, which drive the internet in the connected car market.

Based on Connectivity, the Connected Car Market is segmented into Integrated, Embedded, and Tethered. Integrated connectivity held the largest market share in 2024. The capacity of the modern automobile to communicate between actuators, modules, and sensors and to save wire weight depends heavily on in-vehicle networking and communications.

The anti-lock brake system (ABS), airbags, air conditioning, anti-theft, door locks, engine, radio, steering, suspension, gearbox, windows, diagnostic tests, and other features are all controlled by this network. There are a number of sub-networks inside this network, including LIN/SAE 2602, FlexRay, Media Oriented Systems Transport (MOST), etc. The automobile industry is changing as a result of innovative developments in automotive connection and technology. The industry is getting closer to autonomous driving functionality thanks to technologies like artificial intelligence (AI) and next-generation advanced driver assistance systems (ADAS), as well as expanding V2X infrastructure.

Customers are expecting more from their mobility experience, including improved navigation, customized in-vehicle infotainment (IVI) systems, predictive maintenance, and over-the-air (OTA) updates in the connected car market. Automotive IoT can be powered by data from connected automobiles transmitted via integrated modems or SIMs. The ability to connect directly with other vehicles (V2V), infrastructure (V2I), pedestrians (V2P), and networks are provided by Vehicle to Everything (V2X) technologies (V2N).

Connected Car Market Regional Insights:

The Asia Pacific region dominated the market with a 45 % share in 2022. The Asia-Pacific Connected Cars Market was valued at USD 38.8 billion in 2022 and is expected to cross USD 102.61 billion by 2027, registering a CAGR of 17.6% during the forecast period. From 2022 to 2027, major industry players are expected to increase their R&D expenditures. Young car buyers are also expected to boost the global connectivity features in the connected car market. The market's leading competitors are increasing their investments and forming partnerships with companies listed to meet the rising demand for connected cars. For example, SAIC Motor and OPPO established a joint venture in August 2022 to develop a software framework for cross-platform connectivity between automobiles and smartphones. Chinese state-owned SAIC Motor announced in March 2022 that it will invest USD 43 billion over the following five years on cutting-edge automotive technology, including connected vehicle solutions.

The market's leading competitors are increasing their investments and forming partnerships with companies listed to meet the rising demand for connected cars. For example, SAIC Motor and OPPO established a joint venture in August 2022 to develop a software framework for cross-platform connectivity between automobiles and smartphones. Chinese state-owned SAIC Motor announced in March 2022 that it will invest USD 43 billion over the following five years on cutting-edge automotive technology, including connected vehicle solutions.

Due to the desire for connection features over mechanical characteristics of the cars, decreasing data costs, increasing internet penetration, the introduction of 5G, and the proliferation of low-cost smart devices, Asia-Pacific has the largest market. The region's upcoming emerging markets are expected to be in Europe and North America.

The largest market is China, which is followed by India and South Korea. China will dominate the connected car industry in the Asia Pacific due to the growth in connection features in the newest automobile models. With rising technological advantages in ICT, data processing, and platform services, secure industrial investment, and a highly focused industrial strategy and backing from the central government, China's domestic market will influence the future associated vehicle industry.

By 2021, one in every two new automobiles sold in China, according to the National Development and Reform Commission, would have smart autonomous features. SAIC Motor, Hyundai Motor Group, NVIDIA Corp., Harman International, and TomTom B.V. are a few of the major companies dominating the international market. To maintain their market position and keep ahead of the competition, major firms are introducing new products and growing their manufacturing capacities. For example, SAIC Motor introduced the linked MG Mulan in China in September 2022.

Hyundai opened its first manufacturing plant in the ASEAN region in Cikarang, Indonesia, in March 2022. The building cost USD 1,5 billion and has a capacity to produce 250000 vehicles annually. New models such the Creta, Santa Fe, Tucson, Stargazer, and IONIQ 5, which will have the newest connection features, will be produced at the facility.

Connected Car Market Scope: Inquiry Before Buying

| Global Connected Car Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 39.61 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 19.02% | Market Size in 2032: | USD 159.82 Bn. |

| Segments Covered: | by Connectivity | Integrated Embedded Tethereds |

|

| by Technology | 4G 3G 2G |

||

| by Vehicle Type | Passenger Cars Commercial Vehicles & Fleets |

||

| by Application | Driver Assistance Telematics Infotainment Others |

||

Connected Car Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Connected Car Market, Key Players are

1. Robert Bosch GmbH (Germany)

2. Continental AG (Germany)

3. Audi AG (Germany)

4. ZF Friedrichshafen AG (Germany)

5. Infineon Technologies (Germany)

6. TomTom N.V. (Netherlands)

7. NXP Semiconductors N.V. (Netherlands)

8. Denso Corporation (Japan)

9. Tata Consultancy Services Limited (India)

10. Visteon Corporation (US)

11. Harman International (US)

12. AT&T Inc. (US)

13. Airbiquity Inc (US)

14. Qualcomm Technologies Inc. (US)

15. Tesla, Inc (US)

16. BorgWarner Inc (US)

17. Ford Motor Company (US)

18. Microsoft Corporation (US)

19. Verizon Communications Inc (US)

20. Intel Corporation (US)

21. Sierra Wireless (Canada)

22. Magna International (Canada)

Frequently Asked Questions:

1] What segments are covered in the Global Connected Car Market report?

Ans. The segments covered in the Connected Car Market report are based on Connectivity, Technology, Vehicle Type and Application.

2] Which region is expected to hold the highest share in the Global Connected Car Market?

Ans. The Asia Pacific region is expected to hold the highest share of the Connected Car Market.

3] What is the market size of the Global Connected Car Market by 2032?

Ans. The market size of the Connected Car Market by 2032 is expected to reach USD 159.82 Bn.

4] What is the forecast period for the Global Connected Car Market?

Ans. The forecast period for the Connected Car Market is 2025-2032.

5] What was the market size of the Global Connected Car Market in 2024?

Ans. The market size of the Connected Car Market in 2024 was valued at USD 39.69 Bn.