Ceramic Armor Market by Material, Application, Platform and Region – Global Market Size Estimation, Industry-Wide Analysis, Competitive Landscape Assessment & Long-Term Forecast to 2032

Overview

The Ceramic Armor Market size was valued at USD 2.71 Billion in 2024 and the total Ceramic Armor revenue is expected to grow at a CAGR of 8.6% from 2025 to 2032, reaching nearly USD 5.25 Billion.

Ceramic armor, thanks to its high compressive strength and hardness, is majorly utilised in armored vehicles and personal armor to withstand bullet penetration. In soft ballistic vests, ceramic plates are typically utilised as inserts. Ceramic armor is a growing sector with several prospects in the military and defence industries. Ceramic armor is widely used in the manufacture of aircraft armors because it provides a high level of protection against ballistic threats. This is expected to drive the growth of ceramic armor market during the forecast period.

Furthermore, the use of ceramic armor in the manufacture of vehicle armor protects them from harsh and unfavourable weather conditions, resistance to corrosion, and ease in vehicle movement. The rise in security challenges in developing nations throughout the world, as well as the increased need for homeland security, are expected to drive the growth of the ceramic armor market during the forecast period. Furthermore, changes in the warfare environment, as well as the proliferation of deadly ammunition and weaponry, are driving the growth of the ceramic armor industry.

To know about the Research Methodology:- Request Free Sample Report

To know about the Research Methodology:- Request Free Sample Report

Ceramic Armor Market Growth Opportunity

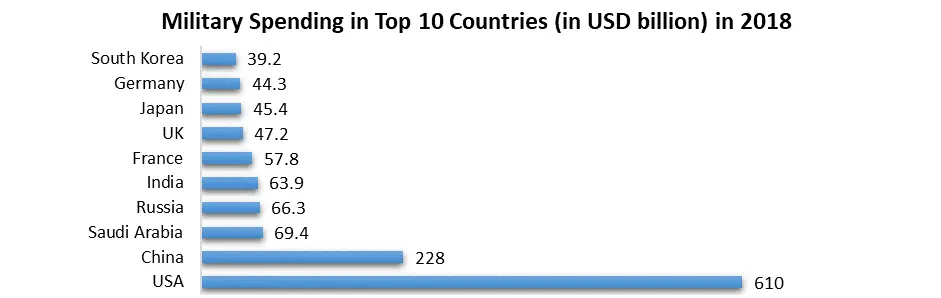

In order to maintain peace and security, all countries have been investing in defense. In countries like United States, China, India, etc., governments have been increasing the defense budget regularly. India was the fifth largest in terms of defense expenditure, wherein the country’s actual defense spending reached INR 2,63,004 crore, i.e., more than the allocated amount. Further, under the “Make In India” initiative, the government has allowed 100% FDI for defense production in the country, which is further expected to attract investments in the defense sector.

Besides this, the country has planned to manufacture 200 helicopters in collaboration with Russian, for the intensification and diversification of their strategic ties. Hence, with increasing defense budgets in countries across the world, the production of defense-related products, such as guns, body armors, weapon armors, armored vehicles, tankers, helicopters, etc., is estimated to increase, further providing opportunities for the ceramic armor market, during the forecast period.

Ceramic Armor Market Drivers

Ceramic Armor Market Drivers

Increasing demand for enhancing soldier safety and ensuring survivability across various regions

Modern-day warfare practices include counter-insurgency, counter-terrorism, and guerrilla warfare operations that may inflict fatal injuries on soldiers. Similar scenarios exist in the law enforcement field wherein criminals, felons, and law offenders can fatally injure corresponding officers, thus necessitating investment in personal protection suits and related equipment. Consequently, a rise in military warfare across several regions globally propels the need for ballistic protection suits and equipment for safeguarding military forces. Also, modernization activities have created several opportunities for ceramic armor market players, leading to alliances with military agencies in a contractual environment.

For Example, in July 2019, KDH Defense Systems, a U.S.-based body armor manufacturer, received two separate delivery orders worth USD 40 million from the U.S. Armed Forces. Emerging economies, such as India and China, are increasingly focusing on replacing legacy military equipment and increasing their defense budget. For instance, in May 2020, China hiked its defense budget to USD 179 billion compared to that of USD 177.6 billion in 2019. However, it has been the lowest hike in recent years due to the significant economic disruption caused by the coronavirus outbreak.

Increasing Homeland Security Concerns to drive the ceramic armor market growth

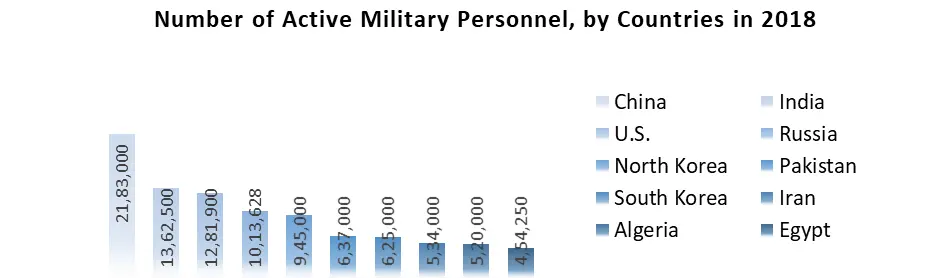

Homeland security concerns have made it necessary for all countries to have well-trained defense forces. The army is trained to fight, in the event of wars with other countries. For homeland security, soldiers are meant to fight, for which they require weapons, vehicles, and body shields to protect them. During wars, soldiers have to wear body armor and carry weapons such as guns, grenades, etc. Hence, these are to be made available to military personnel during wars. Every year, more individuals join the army, creating further demand for armors and weapons.

As per the data provided in the graph, millions of soldiers are active in several countries, which further reflects the demand for guns, armor, etc. in these countries. Countries across the globe invest heavily in maintaining sufficient supply of all such goods in anticipation of war. Ceramic armor are used extensively to produce body armors, weapon armors, armored vehicles, tankers, etc. Hence, the demand for ceramic armor is driven considerably by increasing homeland security concerns.

Continuous innovation of new materials for better ballistic resistance to drive the growth of ceramic armor market

Continuous innovation of new materials for better ballistic resistance to drive the growth of ceramic armor market

The materials used to make ballistic plates play a decisive role in shaping the customer’s decision about purchasing body armor. Ceramics are preferred over steel when it comes to performance requirements. Ceramics have tremendous advantages in terms of weight and design flexibility. A basic ceramic composite armor plate is nearly half the weight of a similar steel armor plate. Besides, it provides resistance to stress rupture at temperatures up to 16,50O°C. All these advantages increase the importance of ceramics for armors. Also, ceramic plates are most often used with para-aramid backing, such as Kevlar brand fiber developed by DuPont.

The latest developments achieved in ceramic armors signify the usability of ceramics for lightweight products. Kata Vitec, an Israeli protection solution (including hard armor plates) provider, produces and supplies assault vests with advanced glass-ceramics insert to enable unrestricted movement of the wearer. Additionally, the vests are low in cost and weight. Another example is Pinnacle Armor’s Dragonskin body armor. This armor utilizes bulletproof ceramic leaves, which create flexible layers shaped like fish scales. As a result, the demand for lightweight, comfortable, and improved protection ceramic armor is expected to provide growth opportunities for ceramic armor manufacturers over the forecast period. This is expected to drive the growth of ceramic armor market.

Ceramic Armor Market Restraints

Stringent government regulations to restraint the growth of ceramic armor market

The body armor plate industry is highly sensitive and is governed by various regulations and acts. It is tested by three regulatory bodies, comprising the National Institute of Justice (NIJ), United States Department of Defense (DoD), and Underwriters Laboratories (UL India). Vendors manufacturing and selling armor plates must comply with the standards to test the level of intensity the body armor can withstand against any threat. In addition to this, the standards help recognize the strength of the attack that an armor plate would be able to combat. Regulatory changes, to ensure enhanced safety, are creating a challenging environment for vendors in the market.

Specific laws governing the ownership and possession of body armor, such as the Body Armor Control Act and Body Armor Possession Act 2015, inhibit their largescale adoption in emerging countries such as India. It is illegal in Australia to possess a body armor plate without the Australian government’s approval in certain territories. Canadian provinces mandate the individual's license to possess a body armor system. However, there are no such restrictions in the rest of the country. In the European Union, ‘ballistic protection’ is valid only for ‘main military usage,’ and civilians are not permitted to possess it.

Reduction in national defense budgets to restraint the ceramic armor market growth

Over the past few years, many nations across the globe have been considering reducing their expenses on military systems. Developing nations often find it difficult to invest aggressively in defense procurements as they need to focus on developing public infrastructure. In view of the growing debts and inflation, even the UN is encouraging such nations to curb their military spending. For example, in March 2022, developing nations such as India have been facing an increasing threat from both China and Pakistan has till reduced their government’s total expenditure by four percent over the last six years.

In December 2020, in the MEA region where there are unending conflicts and pressures still the government defense spending by middle east countries is around USD 44 billion a year less than the previous year. With globalization and the increasing interdependence of economies, nations are finding it crucial to build trust and confidence among each other. By reducing military expenditures, countries are trying to promote peace. If such factors prompt various governments to consider cuts in military spending, the ceramic armor market would have to witness a plummeting demand.

Ceramic Armor Market Segment Analysis

Ceramic Armor Market Segment Analysis

Based on material, the Ceramic Armor market is segmented into boron carbide, silicon carbide, alumina, ceramic metal composite, and others. The demand for lightweight, comfortable, and enhanced protective material is driving the ceramic armor industry growth. Alumina dominated the ceramic armor market in terms of revenue in 2024, thanks to its extensive use by armor manufacturers. Alumina has a high cost-benefit ratio, as well as high refractoriness, modulus of elasticity, and hardness. Boron carbide is largely employed in ceramic plates, which are used to guard against smaller projectiles in armored helicopters and body armors.

Because of the criticality of operations, armor materials are subject to stringent standards. Various regulatory agencies control design and performance criteria. For example, in the United States the performance of armor materials is subject to standard compliance given by the National Institute of Justice (NIJ).

Based on application, the Ceramic Armor market is segmented into body armor, vehicle armor, aircraft armor, marine armor, and others. Body armor has the highest market share in the ceramic armor market and thanks to demand for the same from homeland security departments across the globe is expected to register the highest growth. The use of ceramic armor in the manufacture of body armor provides lightweight and corrosion resistant qualities, which improve mobility and assembly simplicity.

Weapon modernization has boosted threat effectiveness, necessitating the requirement for better body armor. Body armor deflects ballistic strikes by lowering their kinetic energy and thereby lessening the impact. The most profitable markets are the United States, China, and Russia. Body armor is increasingly being provided to first responders such as firemen, police officers, and Emergency Medical Service (EMS) employees in the United States and Europe.

Ceramic Armor Market Regional Insights

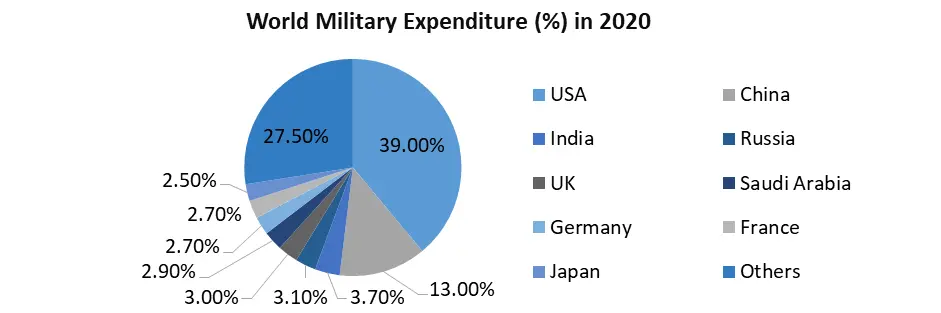

The North America region dominated the global ceramic armor market in 2024 and is expected to hold the highest revenue of the ceramic armor market. The government military programs, such as the Extremity Protection program and Soldier Protection System–Torso for providing full body armor to the armed forces, are expected to drive the growth of ceramic armor industry in the regional market. The U.S. held the top position in military spending in 2024. Such a high budget for military applications and services has further fueled the development and adoption of body armor in the North America market, further driving the growth of ceramic armor market.

The Asia Pacific region held a significant ceramic armor industry share in 2024 and is expected to significantly grow during the forecast period. The large-scale modernization activities of traditional systems and the rise in warfare & border disputes in the Asia Pacific region's emerging economies, such as China, India, and South Korea, drive the demand for ceramic armor in this region. In March 2020, Ordnance Factory Board (India) designed bullet resistant jacket (BRJ) in compliance with different national and international ballistic standards. These jackets are customizable with plate pockets in the carrier for soft/ hard armor panel protection.

The Europe ceramic armor market accounted for over 20% of the market share in 2024. However, in the European Union, ballistic protection is valid only for primary military usage, and civilians cannot legally purchase or possess it. In September 2020, Holding Technodinamika, a subsidiary of Rostec, announced that it would soon begin the serial production of armor plates made of corundum ceramics that demonstrated high protective properties than armored steel during tests.

In 2019, Saudi Arabia spent USD 61.9 billion on military applications and services and held the 5th position in military expenditure across the world. It had the highest spending as a share of its GDP (Gross Domestic Product), which is 8%. Thus, the growth of ceramic armor in the Middle East region is expected to grow significantly, further driving the growth of ceramic armor industry.

Ceramic Armor Market Scope: Inquire before buying

| Ceramic Armor Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 2.71 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 8.6% | Market Size in 2032: | USD 5.25 Bn. |

| Segments Covered: | by Material | Boron Carbide Silicon Carbide Alumina Ceramic Matrix Composite Others |

|

| by Application | Body Armor Vehicle Armor Aircraft Armor Marine Armor Others |

||

| by Platform | Defense Homeland security Civilians |

||

Ceramic Armor Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Ceramic Armor Market, Key Players are

1. Ceradyne (U.S.)

2. SAAB AB (Sweden)

3. ArmorWorks (U.S.)

4. CeramTec (Germany)

5. Koninklijke Ten Cate BV (Netherlands)

6. CoorsTek Inc. (U.S.)

7. M Cubed Technologies (U.S.)

8. Olbo & Mehler (Germany)

9. Safariland LLC (U.S.)

10. BAE Systems (UK)

11. Morgan Advanced Materials (UK)

12. Saint-Gobain S.A. (France)

13. 3M Company (U.S.)

14. II-VI Incorporated (U.S.)

15. Safariland, LLC (U.S.)

16. MKU Limited (India)

Frequently Asked Questions:

1] What is the growth rate of the Global Ceramic Armor Market?

Ans. The Global Ceramic Armor Market is growing at a significant rate of 8.6% during the forecast period.

2] Which region is expected to have the highest growth rate in the Global Ceramic Armor Market?

Ans. The North America region is expected to hold the highest growth rate in the Ceramic Armor Market during the forecast period.

3] What was the Global Ceramic Armor Market size in 2024?

Ans: The Global Ceramic Armor Market size was USD 2.71 Billion in 2024.

4] What are the major key players of the Global Ceramic Armor Market?

Ans. The major key players of the Global Ceramic Armor Market are Ceradyne (U.S.), SAAB AB (Sweden), ArmorWorks (U.S.), CeramTec (Germany), CoorsTek Inc. (U.S.), and Koninklijke Ten Cate BV (Netherlands).

5] What factors are driving the growth of the Global Ceramic Armor Market in 2024?

Ans. Security concerns in developing regions and growing demand from various applications are the major factors expected to drive the growth of the Global Ceramic Armor Market during the forecast period.