Carbon Credit Market Size by Type, Project Type, End Use, Region – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Mapping & Forecast to 2032

Overview

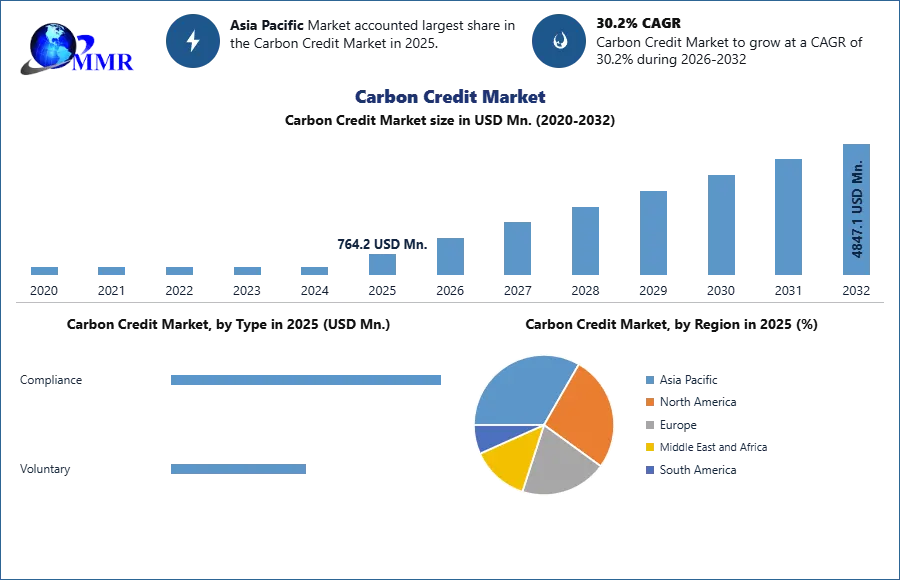

The Carbon Credit Market size was valued at USD 764.2 Million in 2025 and the total Carbon Credit Market size is expected to grow at a CAGR of 30.2% from 2026 to 2032, reaching nearly USD 4847.1 Million by 2032.

Carbon Credit Market Overview:

Carbon credits are a key component of national and international emission trading schemes that have been implemented to mitigate global warming. Credits are exchanged between businesses or bought and sold in international markets at the prevailing market price. Credits are used to finance carbon reduction schemes between trading partners and around the world. Carbon Credit is a certificate that allows individuals or small, medium, and large enterprises to emit one ton of carbon dioxide or other greenhouse gases. This happens when the organization reduces its greenhouse gas emissions below a specific level. The carbon credit certification is given by an independent organization.

The growing focus on the use of sustainable energy sources for energy consumption and production is expected to drive the Carbon Credit Market. For example, according to the MMR Study Report, India has positioned itself as a significant gainer in the carbon credit trade, constituting over 25% of the total global transactions. The country distinguishes itself as a significant beneficiary, amassing roughly $5 billion annually. With an annual output exceeding 30 billion tonnes of greenhouse gases (GHGs), there is a growing initiative across the world to confront this environmental challenge.

Approximately 175 nations, collectively accountable for nearly 60% of global emissions, are actively committed to reducing their greenhouse gas discharges. Remarkably, despite ongoing global endeavors to combat climate change, the United States, the largest single emitter contributing 30.3% to global emissions, has not yet ratified the protocol.

To know about the Research Methodology :- Request Free Sample Report

Carbon Credit Market Dynamics

Increasing Emphasis on Sustainability to Boost Carbon Credit Market

The growing corporate social responsibility and rising awareness among companies regarding the reduction in greenhouse gases to achieve zero-emission goals are expected to drive the Carbon Credit Market. Among all industry verticals, the financial industry has recognized the potential of the carbon credit market and is actively engaging in its development. Financial institutions are investing in carbon credit projects, creating specialized funds, and incorporating carbon credits into their investment portfolios. This increased participation of the financial sector adds a revenue stream to the market that enhances transparency, and attracts further investments, and is expected to propel the growth of the Carbon Credit Market.

Increasing awareness of climate change and environmental impact, businesses are under pressure to adopt eco-friendly practices. Carbon credits, a key component of sustainable initiatives, allow companies to offset their carbon emissions by investing in projects that reduce and capture greenhouse gases. This market surge is driven by both regulatory requirements and a genuine commitment to corporate social responsibility by procuring carbon credits, companies not only adhere to environmental regulations but also support initiatives promoting renewable energy, afforestation, and emission reduction.

As sustainability takes center stage in business priorities, the carbon credit market is positioned for substantial growth. It provides a concrete avenue for organizations to address their carbon footprint and actively engage in the worldwide drive toward a more environmentally friendly future.

Price Volatility Expected to Limit the Carbon Credit Market

The carbon credit market faces challenges due to inherent price volatility, which impedes its growth. Prices are influenced by factors such as regulatory changes, market demand, and geopolitical events, making them unpredictable. Investors and businesses may be hesitant to engage in carbon credit transactions due to the uncertainty surrounding returns on investment. Additionally, the lack of standardized pricing mechanisms and the absence of a centralized global market contribute to price fluctuations. This volatility poses a barrier to widespread adoption, as stakeholders may perceive it as a financial risk, hindering the market's ability to attract consistent participation and investment.

A lack of clear and consistent regulations is expected to discourage investments in emission-reduction projects and reduce market participation. Also, Maintaining the quality and integrity of carbon credits is important for the credibility and effectiveness of the market. Concerns about the accuracy and transparency of carbon credit projects undermine confidence among buyers and investors. Issues such as double counting, inadequate verification processes, or the inclusion of questionable projects are expected to lead to reputational risks and Carbon Credit market inefficiencies.

Government policies and Increased Environmentally Aware Customers Create a Lucrative Opportunity for the Carbon Credit Market

Government policies are expected to play an important role in shaping the carbon credit market. Many governments offer incentives and subsidies to encourage emission reduction projects and create favorable regulatory frameworks for the Carbon Credit Market to grow significantly. Additionally, governments often lead by example, offsetting their emissions and signaling the importance of carbon neutrality. Factors such as favorable conditions for carbon credit transactions and encouraging participation and collaborations are expected to boost the Carbon Credit Market.

Government policies mandating carbon reduction, coupled with a growing base of environmentally aware consumers, form a lucrative landscape for the carbon credit market. Stringent emissions regulations push businesses to seek carbon offsets, boosting demand. As consumers prioritize eco-friendly choices, companies embracing carbon credits gain a competitive edge, appealing to a conscientious market segment. This trend stimulates private investment, fostering innovation in carbon reduction projects. Government-backed initiatives, alongside a discerning consumer base, not only drive the carbon credit market's growth but also encourage corporate responsibility, creating a symbiotic relationship between regulatory frameworks, eco-conscious consumers, and the expanding carbon credit market.

Trends in the Carbon Credit Market:

Increased Digitization and Blockchain Technology: The carbon credit market is leveraging digitalization and blockchain technology to enhance transparency, traceability, and efficiency. Blockchain enables secure and immutable tracking of carbon credits, ensuring their integrity and preventing double counting, which is expected to boost the Carbon Credit Market. It also enables streamlined transactions, automated verification, and easier access for market participants, including smaller buyers and sellers.

Cooperation Between Companies and Measurement and Reporting of Impact: With the growing emphasis on sustainability and ESG (Environmental, Social, and Governance) considerations, there is an increased focus on measuring and reporting the impact of carbon credit projects. Buyers and investors are seeking credible and transparent information on the environmental benefits generated by projects. Standardized methodologies, third-party verification, and reporting frameworks are being developed to provide reliable and comparable data on the emissions reductions achieved. These factors are expected to propel the other end-users to adopt and buy carbon credits, which is simultaneously driving the Carbon Credit Market.

Carbon Credit Market Segment Analysis

Based on By Type, The carbon credit market is broadly categorized into two key types: Compliance and Voluntary. The compliance carbon credit market, regulated under mandatory schemes like the EU Emissions Trading System (EU ETS), represents the larger share of the global carbon market, accounting for over 85% of total traded value in 2025. This segment is driven by legally binding emissions reduction targets imposed on industries and governments.

On the other hand, the voluntary carbon market (VCM) is gaining traction as corporations and individuals proactively invest in carbon offset projects to meet net-zero commitments and ESG goals. The VCM reached a great deal of valuation 2025, supported by growing demand for nature-based solutions, renewable energy credits, and reforestation programs. Together, these segments play a pivotal role in global decarbonization efforts, with increasing cross-border trading, digital MRV tools, and blockchain verification enhancing transparency and scalability in both markets.

Based on Project Type, Carbon credit projects are primarily segmented by type into Avoidance/Reduction and Removal/Sequestration initiatives, each playing a distinct role in climate mitigation. Avoidance or reduction projects focus on preventing the release of greenhouse gases, such as renewable energy installations, improved cookstoves, and methane capture. These projects currently dominate the market due to their cost-efficiency and faster implementation timelines. However, growing attention is shifting toward removal or sequestration projects, which physically extract CO₂ from the atmosphere. This includes nature-based solutions like afforestation, reforestation, and soil carbon sequestration, as well as technology-based solutions such as direct air capture (DAC) and carbon mineralization.

Nature-based solutions alone accounted for nearly 40% of issued credits in the voluntary carbon market in 2025, reflecting strong buyer preference for co-benefits like biodiversity conservation and community development. While technology-based solutions remain limited by high costs and scalability issues, investment is accelerating. As corporate buyers and governments prioritize long-term net-zero strategies, the market is witnessing a gradual shift from avoidance to high-integrity removal credits, underscoring the evolving dynamics of carbon offsetting.

Carbon Credit Market Regional Insights

Asia Pacific dominated the Carbon Credit Market in the year 2025. The largest automobile and other industries are situated in countries such as China and India. There are many emerging Carbon Credit Key Companies in these countries such as Emertech Innovations Pvt Ltd., The Green Meat, and Krish Hortus. These companies are offering and providing solutions and certificates regarding carbon credit. These factors are expected to propel the growth of the Asia Pacific Market. The Indian government passed a bill of Energy Conservation Act 2001 and that became a foundation for the Market.

North America is the fastest-growing market for carbon credit. In the United States, the American Carbon Registry, a nonprofit enterprise of Win rock International, established in 1996 is the first private carbon credit registry in the world. This has created an economic opportunity for tribal nations in North America. The Passamaquoddy Tribe was issued 3.2 million carbon credits, which is expected to generate $35-$45 million in total revenue while protecting 90,000 acres of land. Also, the Confederated Tribes of Washington State and Chugach Alaska Corporation are having benefit from this, which is expected to generate a reliable source of income. These factors are expected to drive the Carbon Credit Market.

India’s Carbon Credit Trading Scheme

India’s central government has passed an amendment to the Energy Conservation Bill that will enable the setting up of a domestic carbon credit trading scheme. The Lower House passed the amendment in August 2022 and the Upper House in December 2022 and it is now law. Entities within India that are allotted credits will be able to trade them domestically.

The scheme allows entities to trade carbon credits on the Indian Carbon Market (ICM) Registry, where they buy and sell carbon credits to meet their emission targets. Entities that surpass their emission targets are eligible for carbon credit certificates, calculated based on the variance between the targeted and actual emissions. The scheme's framework includes the governance structure and the roles and responsibilities of participating entities, providing a comprehensive organizational architecture for the domestic carbon market in India

Recent Industry Developments (2025–2026)

| Exact Date | Company | Development | Impact |

|---|---|---|---|

| 18 March 2026 | Carbon Pulse | Two nature-based climate solutions firms merged to form a new Southeast Asia carbon project developer to scale regional credit supply. | The merger consolidates regional expertise to meet the rising demand for high-quality nature-based offsets in Asian markets. |

| 07 April 2025 | EKI Energy Services Ltd | EKI announced a strategic investment in Tvasta Manufacturing Solutions to integrate sustainable 3D printing technology into its carbon offset portfolio. | This diversification expands technological carbon removal options beyond traditional nature-based sequestration projects. |

| 15 January 2025 | Intercontinental Exchange (ICE) | ICE launched ICE GreenTrace™, a digital environmental registry technology to track the lifecycle of carbon credits using blockchain. | The platform improves market transparency and reduces the risk of double-counting in global carbon credit transactions. |

| 10 January 2025 | Carbonmark | Carbonmark launched Carbonmark Direct, a blockchain-enabled platform designed for the instant issuance and purchase of carbon credits. | This development lowers transaction costs and increases liquidity by allowing direct interaction between project developers and corporate buyers. |

Carbon Credit Market Competitive Landscape

The Carbon Credit market is competitive and dominated by the major key players the key players in the market including Merge Electric Fleet, H2next Private Limited, The Green Meat, Krish Hortus, and Emertech Innovations Pvt Ltd. The key players mainly focus on mergers acquisitions and partnerships to expand business for example, on November 3, 2022, Merge Electric Fleet Solutions entered into a strategic partnership with global climate solutions provider 3Degrees.

This collaboration empowers customers to leverage 3Degrees' expertise in facilitating the transition to electric vehicle fleets and accessing clean fuels programs for new enterprises. Such synergies are expected to boost the Carbon Credit Market, reflecting the industry's commitment to sustainable practices and climate solutions. The collaborative efforts of these key companies underscore a shared dedication to advancing carbon credit initiatives and driving positive environmental impact on a global scale.

Carbon Credit Market Scope: Inquire before buying

| Carbon Credit Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 764.2 USD Mn. |

| Forecast Period 2026-2032 CAGR: | 30.2% | Market Size in 2032: | 4847.1 USD Mn. |

| Segments Covered: | by Type | Compliance Voluntary |

|

| by Project Type | Avoidance / Reduction projects Removal / Sequestration projects Nature Based Solutions Technology based Solutions Others |

||

| by End Use | Power & Energy Aviation Transportation Construction Industrial Agriculture Others |

||

Carbon Credit Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players / Competitors Profiles Covered in Brief in Global Carbon Credit Market Report in Strategic Perspective:

- South Pole

- Gold Standard Foundation

- Verra

- ClimatePartner

- Myclimate

- EcoAct

- Natural Capital Partners

- Siemens

- Plan Vivo Foundation

- EKI Energy Services Ltd

- MSCI (Trove Research)

- Ambipar Group

- Rubicon Carbon

- 3Degrees

- Climate Impact Partners

- Allcot Group

- Green Mountain Energy

- First Climate

- ClimeCo LLC

- Shell (UK)

- Forliance

- Xpansiv

- AirCarbon Exchange (ACX)

- Intercontinental Exchange (ICE)

- CME Group