Global Bifacial Solar Market Size by Product Type, Frame Type, Power Capacity, Cell Technology, Material Type, Installation Type, and End User – Segment-Level Market Assessment, Growth Opportunity Analysis, Competitive Landscape & Forecast to 2032

Overview

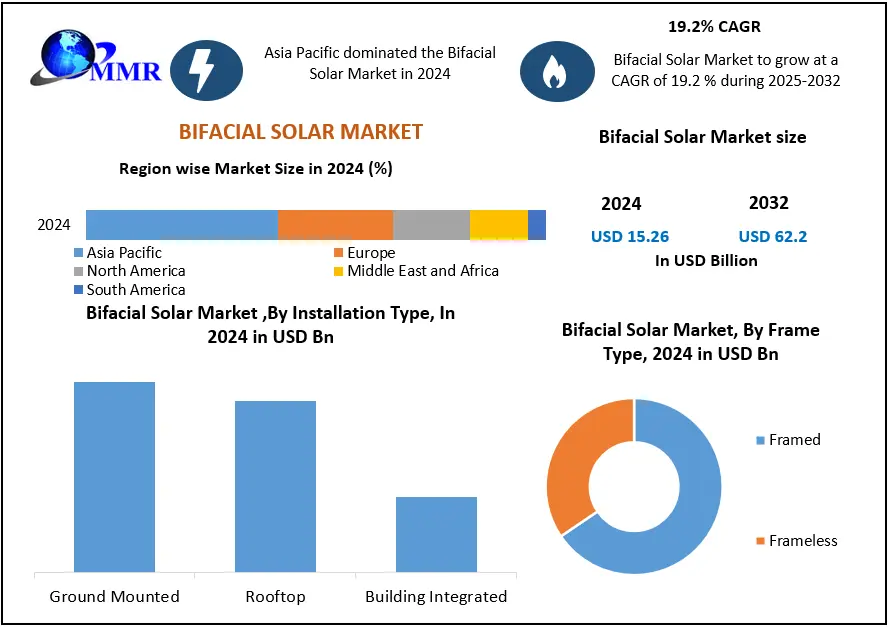

The Bifacial Solar Market size was valued at USD 15.26 Billion in 2024, and the total revenue is expected to grow at CAGR of 19.2 % from 2025 to 2032, reaching nearly USD 62.2 Billion.

The MMR report on the Global Bifacial Solar Market provides an in-depth analysis covering all critical aspects of industry performance and outlook. It includes detailed insights on regional installation capacity, per capita solar trends, and deployment patterns, along with an extensive supply chain and raw material assessment. The report further explores performance benchmarking, technological innovations, and investment trends, supported by comprehensive pricing, cost structure, and demand-side analysis. it examines trade flows, environmental sustainability metrics, and policy frameworks across key regions, concluding with real-world yield performance and field case studies to provide a holistic understanding of market dynamics and future opportunities.

Bifacial Solar Market Overview:

Bifacial solar modules, as opposed to conventional monofacial solar modules, can generate electricity from both the front and back sides of the panel, increasing energy yield. A bifacial solar panel is made up of bifacial solar cells and a back cover glass. Photons that do not absorb in the front layer can be absorbed when they bounce off any adjacent surface. This improves the cell's efficiency. The dual glass mounting has several advantages, including reduced delamination, micro cracking, and moisture corrosion. They have a low degradation rate and a high cell temperature, as well as a high flameproof rating, mechanical strength, and less flexing. Many advanced in commercial solar cells are inherently bifacial, which means that electricity generation from the back side incurs little extra cost at the cell manufacturing level and only a minor increase at the module assembly level to allow the back side of the panel to access sunlight.

As a result, bifacial module solar projects of the same size would generate more electricity, have a lower levelized cost of energy, and provide higher economic returns.

To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Solar energy has emerged as a major source of energy. Solar photovoltaic (PV) energy is a significant source of renewable energy around the world. The cost of a photovoltaic module has decreased significantly in recent years. Growing government support in the form of subsidies, incentives, investments, and so on is being analysed to drive the market. Furthermore, several advantages of bifacial solar panels over monofacial solar panels, as well as increased investments by companies for innovation in this solar panel, are analysed to drive the market. Maxeon will launch Fifth-Generation Shingled Bifacial Solar Panels for the Global Power Plant Market in 2020.

• Rising electricity demand and the lower cost of large-scale electric photovoltaics than fossil fuels are the primary drivers of the bifacial solar panel market.

• Governments around the world are providing incentives and promoting large-scale solar energy deployment, which is fueling the growth of the bifacial solar panel market.

• Key manufacturers are focusing on improving various properties such as low degradation rate, cell temperature, high flameproof rating, mechanical strength, less flexing, reduction of delamination, micro-cracking, and moisture corrosion to improve the quality and functions of the bifacial solar panel.

High initial investment and cost of manufacturing

Although bifacial module technology is gradually becoming more common, high costs continue to be a barrier for manufacturers. Because bifacial solar module technology is still in its early stages, manufacturing equipment must be customised for almost every application. As a result, manufacturing costs are high, while the financial return on process and manufacturing asset investments is low. Until bifacial module manufacturing achieves mass production and economies of scale, production costs are likely to remain higher than for monofacial solar modules. As a result, adoption may continue to be low. As a result, high manufacturing costs are expected to stymie market growth during the forecast period 2024-2030.

Bifacial Solar Market Segment Analysis:

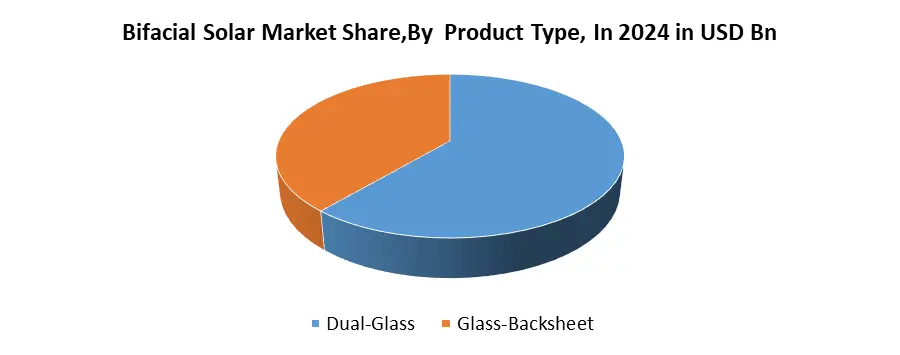

Based on the Product Type, in 2024, Dual-Glass modules are expected to dominate the global Bifacial Solar Market due to their enhanced durability, superior weather resistance, and higher bifacial efficiency. Their glass-glass structure ensures better protection against moisture and microcracks, resulting in longer lifespan and lower degradation rates, making them ideal for utility-scale and harsh-environment installations. Meanwhile, Glass-Backsheet modules retain significance in cost-sensitive projects due to their lightweight design, easier handling, and lower initial investment. Although Dual-Glass modules lead in value and adoption for high-performance applications, Glass-Backsheet variants are projected to gain traction in distributed and rooftop installations, collectively supporting the market’s diversified growth trajectory.

Based on Cell Technology, in 2024, Tunnel Oxide Passivated Contact (TOPCon) technology is expected to dominate the global Bifacial Solar Market owing to its high efficiency, improved temperature coefficient, and compatibility with existing PERC production lines. Heterojunction (HJT) technology follows closely, driven by its superior performance in low-light and high-temperature conditions, along with growing adoption in premium bifacial modules. Passivated Emitter Rear Contact (PERC) remains prevalent in cost-sensitive segments due to its affordability and mature manufacturing base, though its efficiency ceiling limits future growth. The Others segment, including emerging perovskite-tandem and IBC technologies, is projected to expand rapidly as innovation accelerates, collectively contributing to efficiency-driven market evolution.

Bifacial Solar Market Regional Insights:

Due to bifacial solar research and development in the US, the US held the largest share of the market in North America and is expected to grow at the fastest CAGR during the forecast period. However, bifacial solar production in the United States is currently low. The National Renewable Energy Laboratory (NREL) began a study on bifacial performance in March 2020 and will begin testing in Colorado.

Due to bifacial solar research and development in the US, the US held the largest share of the market in North America and is expected to grow at the fastest CAGR during the forecast period. However, bifacial solar production in the United States is currently low. The National Renewable Energy Laboratory (NREL) began a study on bifacial performance in March 2020 and will begin testing in Colorado.

During the forecast period, Asia-Pacific is expected to have the largest market share. This is primarily because countries in the region, particularly India, China, and a few South Asian countries, are heavily focused on developing renewable energy sources and investing in solar energy.

Due to extensive government support for renewable energy development, China held the largest market share in Asia-Pacific in 2023. Because of the large installed base of solar panels, the bifacial solar market in India and China is expected to grow at the fastest CAGR during the forecasted period. In the Middle East & Africa, the UAE is expected to be one of the leading markets for bifacial solar modules.

The report's goal is to provide industry stakeholders with a comprehensive analysis of the Bifacial Solar market. The report analyses complicated data in simple language and presents the past and current state of the industry, as well as forecasted market size and trends. The report examines all aspects of the industry, including a detailed examination of key players such as market leaders, followers, and new entrants.

The report includes a PORTER and PESTEL analysis, as well as the potential impact of market microeconomic factors. External and internal factors that are expected to positively or negatively affect the business have been analysed, providing a clear future view of the industry to the reader.

The report also aids in understanding the Bifacial Solar market dynamics, structure, and size projections by analysing market segments. A clear representation of competitive analysis of key players in the Bifacial Solar market by product, price, financial position, product portfolio, growth strategies, and regional presence makes the report an investor's guide.

Bifacial Solar Industry Ecosystem

Bifacial Solar Market Scope: Inquiry Before Buying

| Global Bifacial Solar Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2024 | Forecast Period: | 2025-2032 |

| Historical Data: | 2019 to 2024 | Market Size in 2024: | USD 15.26 Bn. |

| Forecast Period 2025 to 2032 CAGR: | 19.2% | Market Size in 2032: | USD 62.2 Bn. |

| Segments Covered: | by Product Type | Dual-Glass Glass-Backsheet |

|

| by Frame Type | Framed Frameless |

||

| by Power Capacity | Upto 200 WP 200-400 WP Above 400 WP |

||

| by Cell Technology | Passivated Emitter Rear Contact (PERC) Heterojunction (HJT) Tunnel Oxide Passivated Contact (TOPCon) Others |

||

| by Material Type | Silicon Cadmium Telluride Copper Indium Gallium Selenide Organic Photovoltaics |

||

| by Installation Type | Ground Mounted Rooftop Building Integrated |

||

| by End User | Commercial & Industrial Residential Others |

||

Bifacial Solar Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Bifacial Solar Market, Key Players

1. Jinko Solar

2. LONGi Solar

3. JA Solar

4. Trina Solar

5. Canadian Solar

6. Risen Energy

7. Hanwha Q CELLS

8. REC Group

9. Suntech

10. HT-SAAE (Huantai Group)

11. Maxeon Solar Technologies

12. Meyer Burger

13. GCL-SI

14. Talesun Solar

15. Vikram Solar

16. Adani Solar

17. Boviet Solar

18. AE Solar

19. Solaria

20. Jolywood Solar Technology Co., Ltd.

21. LG Electronics

22. Maxeon Solar Technologies

23. SunPower Corporation

24. Tongwei Co., Ltd.

25. Lumos Solar

26. Prism Solar Technologies

27. Neo Solar Inc.

28. Yingli Green Energy

29. Panasonic Corporation

30. Jakson Solar Modules & Cells

31. Others

Frequently Asked Questions:

1] What segments are covered in the Bifacial Solar Market report?

Ans. The segments covered in the Bifacial Solar Market report are based on Product Type, Frame Type, Power Capacity, Cell Technology, Material Type, Installation Type, End User and region

2] Which region is expected to hold the highest share of the Bifacial Solar Market?

Ans. The Asia Pacific region is expected to hold the highest share of the Bifacial Solar Market.

3] What is the market size of the Bifacial Solar Market by 2032?

Ans. The market size of the Bifacial Solar Market by 2032 is USD 62.2 Bn.

4] What is the growth rate of the Bifacial Solar Market?

Ans. The Global Bifacial Solar Market is growing at a CAGR of 19.2% during the forecasting period 2025-2032.

5] What was the market size of the Bifacial Solar Market in 2024?

Ans. The market size of the Bifacial Solar Market in 2024 was USD 15.26 Bn.