Automotive Radar Market – Global Market Size, Strategic Growth Drivers, Risk Assessment Framework, Regulatory Landscape Review, Competitive Intensity Mapping & Long-Term Industry Outlook to 2034

Overview

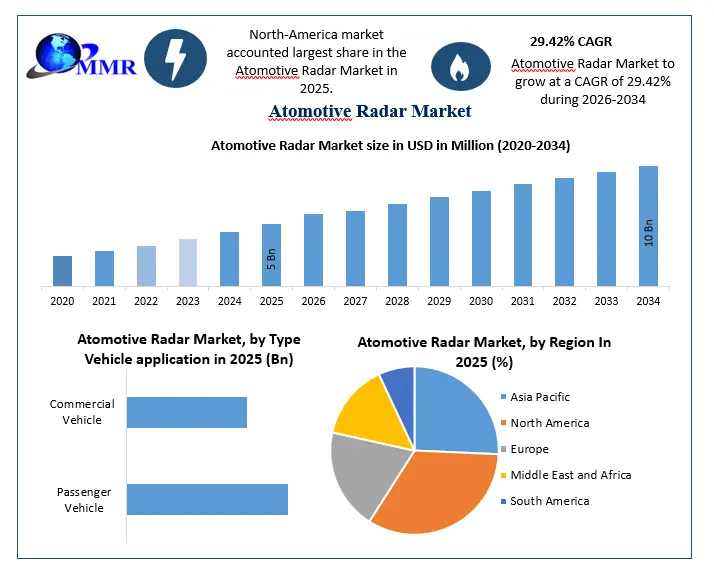

Automotive Radar Market size was valued at USD 8.82 Billion in 2025 and the total Automotive Radar Market revenue is expected to grow at a CAGR of 29.42% from 2026 to 2034, reaching nearly USD 89.91 Billion by 2034.

Overview of the Automotive Radar Market

Automotive radar technology is seamlessly integrated into vehicles with the primary function of detecting and quantifying the speed, proximity, and orientation of objects situated in the vehicle's immediate surroundings. This technology typically encompasses a transmitter, responsible for emitting radio waves that subsequently interact with nearby objects and return to a receiver. This process facilitates the highly accurate assessment of the objects' distance, velocity, and spatial coordinates. The deployment of automotive radar is pivotal in elevating safety standards and facilitating the operation of advanced driver assistance systems (ADAS). By furnishing critical data for functions like collision avoidance and adaptive cruise control, automotive radar significantly contributes to enhancing situational awareness and augmenting overall road safety. The graphical representation and structural exclusive information showed the dominating region of the Automotive Radar Market. The detailed and constructive formation of key drivers, opportunities, and unique segmentation outputs structural and optimistic data. Validated using primary as well as secondary research methodology and scope of the Automotive Radar Market.

Atomotive Radar Market Growth and Share Analysis

To know about the Research Methodology :- Request Free Sample Report

Automotive Radar Market Dynamics

Rising Demand for ADAS and Increasing Vehicle Production are the major drivers of Automotive Radar Market

The growing consumer demand for Advanced Driver Assistance Systems (ADAS) is a pivotal driver in the automotive radar industry. ADAS functionalities, such as adaptive cruise control, lane departure warning, and blind-spot detection, heavily rely on radar technology for their effective operation. This surge in consumer interest in ADAS-equipped vehicles has not only spurred the automotive radar sensors market but has also prompted automotive radar manufacturers to innovate in response to market demands, leading to continuous growth in the Radar Sensor market. The expansion of the automotive radar market is closely tied to the overall increase in vehicle production, particularly in emerging markets. As the production of vehicles grows, there is a greater opportunity for automotive radar integration. Automotive radar companies are strategically positioned to tap into these expanding markets, further fuelling the growth of the Automotive Radar Industry Analysis.

The automotive radar sensors market is greatly influenced by the stringent safety regulations and standards set by governments and regulatory bodies globally. These regulations mandate the inclusion of advanced safety features like automatic emergency braking, pedestrian detection, and collision avoidance systems, which are contingent on automotive radar technology. Automotive radar companies and manufacturers are compelled to integrate radar systems into their vehicles to comply with these standards. Consequently, the automotive radar applications market has experienced significant growth, driven by regulatory requirements that prioritize safety.

Ongoing technological advancements in radar systems, including higher resolution, improved range, and reduced interference, are pivotal drivers of market growth. These advancements enhance the capabilities of radar sensors, making them more appealing to both automakers and consumers. The continuous evolution of radar technology contributes significantly to the competitive edge of automotive radar companies and their products in the Automotive Radar sensors market. The increasing awareness among consumers about the benefits of safety systems and ADAS is a driving force behind the automotive radar market, radar technology becomes more cost-effective due to economies of scale and technological improvements, it becomes accessible to a broader range of vehicle models and consumers.

The reduction in radar system costs is instrumental in driving market growth, expanding its reach across various segments of the automotive industry, including Automotive Radar sensors, and increasing the affordability of these safety features for consumers. Competition within the automotive radar market fuels innovation and the development of new radar-based applications. Automotive radar companies are continually striving to outperform their competitors by introducing cutting-edge radar technologies, leading to market expansion and fostering innovation within the sector.

The rise of autonomous vehicles and the increasing market for electric vehicles significantly contributes to the demand for radar technology. Radar systems are not only indispensable for autonomous navigation but also play a vital role in enhancing the safe operation of electric vehicles. This intersection of radar technology with autonomous and electric vehicles augments the Radar Sensor market. The growing environmental concerns and the push for enhanced fuel efficiency are driving the adoption of radar systems for features like adaptive cruise control. These radar-based systems optimize vehicle speed, reduce fuel consumption, and align with the goals of environmental sustainability, making them an important driver in the automotive radar industry.

Expansion of Autonomous Vehicles and Radar for Commercial Vehicles are the potential opportunities in the Automotive Radar Market

The growth of autonomous vehicles represents a significant opportunity within the automotive radar market. These self-driving cars rely heavily on radar technology for their safety and functionality. As the adoption of autonomous vehicles increases, there is a heightened demand for advanced radar systems, driving innovation and growth in the automotive radar sensors market. Automotive radar companies are well-positioned to seize this opportunity, with radar applications expanding to support autonomous driving functions. The adoption of radar technology in commercial vehicles, including trucks and buses, is gaining momentum. In urban settings where the risk of collisions is higher, radar systems offer substantial safety benefits.

Automotive radar companies tap into this sector, providing radar solutions tailored to the unique needs of commercial vehicles. This opportunity contributes to the expansion of the Radar Sensor market. With the rapid expansion of the electric vehicle (EV) market, there is a notable opportunity for automotive radar manufacturers. Radar systems play a crucial role in enhancing the safety and operational efficiency of EVs. The unique characteristics of electric vehicles, such as their silent operation, provide a niche where radar applications can excel. This trend contributes to the growth of the Automotive Radar Industry Analysis and offers avenues for the development of specialized radar solutions for the EV sector.

The integration of 5G connectivity and vehicle-to-everything (V2X) communication systems presents a promising opportunity for the automotive radar market. Radar sensors can collaborate with these advanced technologies, enhancing road safety and delivering sophisticated features to vehicles. This convergence expands the capabilities of radar systems, making them more attractive to automakers, and fosters growth in the automotive radar applications market. The continuous evolution of ADAS technologies, in which radar plays a pivotal role, offers opportunities for innovation and growth. As ADAS features become more advanced, there is a growing demand for radar sensors to support these functionalities. Automotive radar companies are at the forefront of developing radar solutions that keep pace with the evolution of ADAS, expanding the market reach to a broader range of vehicle models. Offering customizable radar solutions and differentiated features holds promise as a lucrative opportunity. Tailoring radar systems to specific applications or industries, such as agriculture or construction, can lead to the creation of niche markets and specialized product offerings. This customization and differentiation are drivers for the development of specialized radar solutions and new business segments within the automotive radar industry.

Automotive Radar Market Segment Analysis

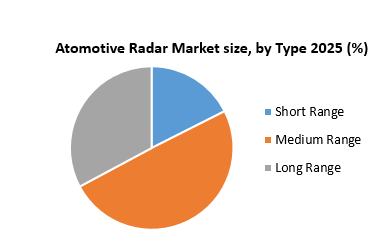

Range Type: Short-Range Radar (SRR): Short-range radar sensors are a pivotal component within the automotive radar market. These sensors are employed for proximity sensing and collision avoidance applications, making them indispensable for parking assistance and low-speed scenarios. The growing demand for advanced driver assistance systems (ADAS) has amplified the market share for short-range radar sensors. Medium-Range Radar (MRR): Medium-range radar sensors are a crucial aspect of the automotive radar market, serving the purpose of adaptive cruise control (ACC) and collision warning systems. The advent of these sensors has facilitated the development of semi-autonomous vehicles, thereby contributing to their steady market growth. Long-Range Radar (LRR): Long-range radar sensors hold a prominent share in the automotive radar market, primarily responsible for applications like blind-spot detection and forward collision warning systems. As the automotive industry progresses toward fully autonomous vehicles, the Automotive Radar market share of long-range radar sensors is anticipated to expand significantly.

Vehicle Type: Automotive Radar market is sub-segmented into Commercial vehicle and Passenger vehicle. The passenger vehicle segment is expected to grow faster than the commercial vehicle market. The growing awareness of vehicle safety among mid-priced vehicle owners is the key element driving this segment's rise. According to OICA, worldwide passenger automobile sales increased by 4.5 % in 2025 compared to 2025. Major luxury car manufacturers such as Mercedes-Benz and BMW had a large boost in sales in 2025, with 2.08 million and 2.3 million units sold, respectively. The automotive radar market is likely to grow throughout the forecast period as more passenger cars are fitted with radar-based safety systems. Passenger vehicles constitute a substantial portion of the automotive radar market. Radar applications in passenger vehicles include adaptive cruise control, parking assistance, and lane departure warning systems. With consumers increasingly adopting ADAS for improved safety and convenience, this segment is poised for sustained growth. Commercial vehicles, such as trucks and buses, are deploying radar sensors to enhance safety and optimize driving. Applications encompass collision avoidance, blind-spot detection, and adaptive cruise control, making commercial vehicles a key segment in the automotive radar market.

Application: Adaptive Cruise Control (ACC): Adaptive cruise control applications have garnered significant attention in the automotive radar market. Radar sensors enable vehicles to maintain a safe following distance from the vehicle ahead, enhancing both safety and driving comfort. Blind-Spot Detection (BSD): Radar sensors used for blind-spot detection are instrumental in improving road safety by alerting drivers to vehicles in their blind spots. This application segment plays a crucial role in enhancing driver awareness and reducing accidents. Lane Departure Warning (LDW): The automotive radar market witnesses a growing demand for radar sensors in lane departure warning systems. These sensors assist drivers by notifying them of unintended lane departures, thus reducing the risk of accidents due to drifting out of the lane. Parking Assistance: Parking assistance applications, driven by radar sensors, have gained widespread popularity among consumers. These sensors aid drivers in manoeuvring their vehicles safely into parking spaces, thereby reducing the likelihood of collisions. Collision Avoidance System: Radar sensors play a pivotal role in collision avoidance systems. They detect obstacles in the vehicle's path and trigger braking or steering interventions, substantially enhancing road safety and reducing the severity of accidents.

Traffic Sign Recognition: Traffic sign recognition systems employ radar sensors for detecting and interpreting traffic signs, subsequently providing drivers with relevant information. This application contributes to improved traffic regulation compliance and safety. Pedestrian Detection: The automotive radar market encompasses radar sensors used in pedestrian detection applications, primarily designed to enhance pedestrian safety. These systems identify pedestrians near the vehicle and trigger braking or warnings to prevent accidents. Others: Besides the aforementioned applications, the automotive radar market caters to various other applications, including road condition monitoring, forward collision warning, and intersection assistance, illustrating the versatility and wide-ranging potential within this dynamic market segment.

Automotive Radar Market Regional Analysis

North America commands a significant share within the Automotive Radar market, representing a substantial portion of this industry. This region is characterized by a well-established automotive radar sensors market, with prominent automotive radar companies and manufacturers. The extensive adoption of automotive radar technology in North America is primarily propelled by stringent safety regulations, growing consumer demand for Advanced Driver Assistance Systems (ADAS), and a pronounced focus on automotive radar applications. These applications encompass crucial functions like collision avoidance and adaptive cruise control. Additionally, the emphasis on the development and integration of radar-based software has invigorated the Automotive Radar Industry Analysis within this region.

Europe also holds a substantial role in the global Automotive Radar market, boasting a noteworthy market share. The European market is renowned for its innovative strides in radar technology, housing several key automotive radar manufacturers and companies. Europe's Automotive Radar Industry Analysis benefits from the robust presence of safety regulations and standards, particularly exemplified by the European New Car Assessment Programme (Euro NCAP). The embrace of radar technology in Europe is largely fuelled by the demand for advanced ADAS features, further enhancing the region's market share. The ongoing development and integration of automotive radar software continue to be significant drivers in Europe, amplifying the scope and sophistication of radar applications in the automotive sector in various countries of Europe such are United Kingdom, France, Germany, Spain, Sweden, Austria and Italy.

The Asia-Pacific region emerges as a dynamic and burgeoning segment of the Automotive Radar market, commanding a noteworthy market share. Particularly, countries such as China, Japan, and South Korea are witnessing robust growth. The adoption of radar technology in Asia-Pacific is driven by the burgeoning automotive industry, escalating vehicle production rates, and a dedicated focus on utilizing automotive radar applications to enhance road safety. This region has witnessed the emergence of local automotive radar manufacturers and companies, actively contributing to the expansion of the Radar Sensor market. As Asia-Pacific places increasing emphasis on safety standards and the development of ADAS features, the Automotive Radar Industry Analysis in this region is poised for further expansion.

Automotive Radar Market Competitive Landscape

Bosch and APCOA, in a significant collaborative effort, are set to introduce automated valet parking technology in parking facilities across Germany. Following the successful commercial implementation of automated valet parking in the P6 parking garage at Stuttgart airport, the two entities are embarking on an expansion journey to deploy this technology in 15 additional parking garages across Germany, spanning cities from Hamburg to Munich. The expansion project is slated to commence in 2025, marking the worldwide market launch of automated valet parking. This strategic master agreement signed by Bosch and APCOA marks the inaugural step toward a global market launch, with the ultimate objective of equipping hundreds of parking garages across the world with automated valet parking systems in the coming years. Notably, Germany has positioned itself as one of the early adopters, having established Level 4 legislation that provides the framework for systems like automated valet parking. This ground-breaking technology is poised to become accessible in selected parking facilities within cities such as Hamburg, Berlin, Cologne, Frankfurt, and Munich, with plans for further expansion into other European parking garages.

Frank van der Sant, a member of the board of management and chief commercial officer of APCOA PARKING Group, underscores the significance of this technological advancement for parking customers, especially in time-sensitive scenarios at locations like airports, concert halls, event venues, and trade fair facilities. The deployment at Stuttgart airport is just the starting point of a larger vision.

Automotive Radar Industry Ecosystem

Automotive Radar Market Scope: Inquiry Before Buying

| Automotive Radar Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2034 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | USD 8.82 Bn |

| Forecast Period 2026 to 2034 CAGR: | 29.42% | Market Size in 2034: | USD 89.91 Bn |

| Segments Covered: | by Range | Long Range Medium Range Short Range |

|

| by Vehicle | Commercial Vehicles Passenger Vehicle |

||

| by Frequency | 24 GHz 77 GHz |

||

| by Application | Adaptive Cruise Control (ACC) Autonomous Emergency Braking (AEB) Blind Spot Detection (BSD) Forward Collision Warning System Intelligent Park Assist Other ADAS Applications |

||

Automotive Radar Market, by Regions

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Key Players in the Automotive Radar Market

AISIN CORP.

Arbe Robotics Ltd

AU Inc

Autoliv Inc.

Bosch Mobility Solutions

Banner Engineering Corp.

Continental AG

DENSO Corp.

Eravant

Faurecia SE

Infineon Technologies AG

MediaTek Inc.

NXP Semiconductors NV

Renesas Electronics Corp.

Rohde and Schwarz GmbH and Co. KG

S.m.s Smart Microwave Sensors GmbH

Texas Instruments Inc.

Tsien UK Ltd

Vayyar Imaging Ltd.

Analog Devices Inc,

Aptiv plc, Autoliv Inc.,

Denso Corporation,

HELLA GmbH & Co.

KGaA

Infineon Technologies AG,

NXP Semiconductors,

Robert Bosch GmbH,

Valeo,

ZF Friedrichshafen AG.

Frequently Asked Questions

1. What is the Automotive Radar Market?

Ans: The automotive radar market is a segment of the automotive industry that focuses on radar technology used in vehicles to detect and measure the speed, range, and direction of objects in the vicinity.

2. What are the key applications of automotive radar?

Ans: Automotive radar is primarily used for collision avoidance, adaptive cruise control, blind-spot detection, and pedestrian detection, enhancing vehicle safety and driving assistance.

3. What are the drivers of the automotive radar market?

Ans: Drivers include stringent safety regulations, rising demand for Advanced Driver Assistance Systems (ADAS), increasing vehicle production, technological advancements, consumer awareness, urbanization, cost reduction, competition, and the growth of autonomous and electric vehicles..

4. What regions are driving the Automotive Radar Market's growth?

Ans: North America leads with a significant market share, followed by Asia Pacific and Europe, due to their robust life sciences sectors.

5. Which types of radar, such as LRR, MRR, or SRR, are widely used in the automotive radar market?

Ans: Long-range radar (LRR), medium-range radar (MRR), and short-range radar (SRR) are used in the automotive radar market, each with specific applications.