Automotive Lubricants Market – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

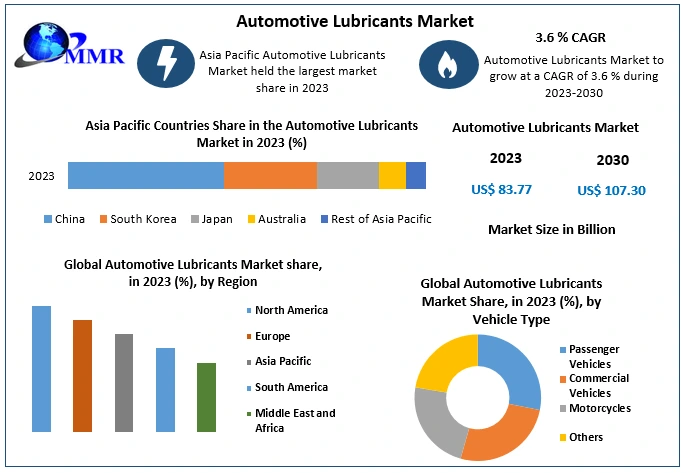

The Automotive Lubricants Market size was valued at USD 89.9 Billion in 2025 and the total Automotive Lubricants revenue is expected to grow at a CAGR of 3.6% from 2025 to 2032, reaching nearly USD 115.16 Billion.

The automotive lubricant industry plays a critical role in the performance, efficiency, and longevity of vehicles. Lubricants are essential for reducing friction, preventing wear and tear, and ensuring smooth engine and transmission function. The global market for automotive lubricants is closely tied to trends in automobile production, demand for transportation, industrial activities, and regulatory frameworks related to emissions and sustainability.

Top automotive lubricant companies dominate the industry with high market share in 2025. Chevron Ceylon Limited leading the market, blending 57.03% of the total production, followed by Indian Oil Corporation Limited (26.51%), Laugfs Holdings Limited (9.18%), and Ceylon Petroleum Corporation (7.28%). The majority of lubricant production was for automotive oils, amounting to 38,072.68 kL, which accounted for over 73% of the total lubricant production. The industrial oil segment was the second-largest, contributing 12,119.24 kL (23%), while marine oils, greases, and other Product Types of lubricants made up a smaller portion. Given that the Government of Sri Lanka (GOSL) generates revenue from authorized lubricant parties through a bi-annual registration fee or a 0.75% levy on sales, the lubricant industry contributed LKR 336 million to the state treasury in 2021.

In the global context, India is one of the largest consumers of automotive lubricants, ranking third in the world. This can be attributed to strong automotive production trends, particularly due to an increasing preference for personal vehicles over public transport, a trend that was accelerated by the COVID-19 pandemic. India’s automotive industry grew by 27% in 2021, even as global demand declined. The Indian automotive lubricants market was estimated at 1.45 billion liters in 2021, with a projected compound annual growth rate (CAGR) of 6.31%, expected to reach 1.97 billion liters by 2026. The dominant segment in India is motorcycle lubricants, with 77.55% of on-road vehicles in 2020 being two-wheelers, followed by passenger vehicles (16.84%) and commercial vehicles (5.61%). Given the rising number of vehicles, the demand for automotive lubricants in India is expected to remain robust.

The demand for automotive lubricants is directly linked to vehicle production and the transportation sector. In 2021, global automotive production rebounded after a sharp decline in 2020 due to pandemic-related disruptions. India saw significant growth (27%), reflecting increased consumer demand, while other markets, especially North America and Europe, experienced slower recoveries. China, India, and Southeast Asian markets continue to be the major contributors to automotive lubricant consumption due to expanding vehicle ownership rates and industrialization.

However, despite these strong trends, the global lubricant market experienced a decline of nearly 2% in 2023, primarily due to economic slowdowns, reduced industrial activity, and a shift toward electric vehicles (EVs), which require fewer lubricants than internal combustion engine (ICE) vehicles. However, long-term projections indicate steady growth through 2032, driven by demand in manufacturing, logistics, and construction sectors, particularly in Asia. Countries like Vietnam are expected to see an increase in lubricant consumption, while North America and Europe are forecasted to see a decline of about 1% per year due to technological advancements, stringent environmental regulations, and a gradual transition to EVs.

In terms of supply, the lubricant industry is highly competitive, with major global players such as Shell, BP (Castrol), Chevron, ExxonMobil, TotalEnergies, and Indian Oil Corporation dominating the market. These companies are investing in synthetic and bio-based lubricants, which offer superior performance and environmental benefits over traditional mineral-based oils. Additionally, regulatory policies focusing on carbon emissions and sustainability are prompting manufacturers to develop low-viscosity, energy-efficient lubricants that improve fuel economy. To know about the Research Methodology :- Request Free Sample Report

To know about the Research Methodology :- Request Free Sample Report

Automotive Lubricants Market Trend

Shift towards Synthetic and Bio-Based Lubricants

The switch to synthetic and bio-based lubricants in the automotive sector stems from their superior performance, environmentally friendly nature and alignment with stringent regulations. Synthetic lubricants outshine conventional mineral oils due to better viscosity, thermal stability and resistance to degradation, enhancing engine efficiency and longevity. Bio-based lubricants, derived from renewable sources, boast lower toxicity, biodegradability and reduced environmental impact, addressing the increasing sustainability demands. Stringent environmental regulations and global standards mandated by governments have directed the Automotive Lubricants Market towards lubricants with decreased emissions, amplifying the industry's shift in this direction.

Technological advancements have rendered the production of synthetic lubricants more cost-effective and scalable, fostering the development of high-performance options meeting industry standards. Rising consumer awareness regarding the environmental impact of conventional lubricants has surged, significantly shaping preferences toward eco-conscious products within the Automotive Lubricants Market. These choices not only benefit vehicles but also align with environmental concerns. The burgeoning automotive industries in emerging markets drive the transition, as these markets are receptive to innovative technologies, embracing synthetic and bio-based lubricants as they expand their automotive sectors.

Automotive Lubricants Market Dynamics

Increasing Demand for High-Performance Lubricants to Boost Market Growth

The increasing need for high-performance lubricants is driven by their essential role in improving operational efficiency and extending machinery lifespan across diverse industries. These lubricants offer superior qualities compared to traditional options, delivering heightened efficiency, prolonged equipment durability and decreased maintenance expenses. Industries relying on heavy machinery such as automotive, manufacturing, aerospace, and energy opt for high-performance lubricants due to their resilience under extreme conditions, elevated temperatures and heavy workloads. Formulated with advanced compositions often integrating synthetic base oils and specialized additives, these lubricants provide exceptional lubrication, minimizing friction, wear, and corrosion within machine components. This leads to reduced downtime, heightened reliability, and optimized equipment performance, boosting the increasing preference for these lubricants within the Automotive Lubricants Market.

The focus on sustainability and adherence to environmental regulations contribute to the surge in demand for high-performance lubricants. These lubricants are engineered more environmentally friendly, promoting reduced emissions and less ecological impact while upholding superior performance standards. As industries strive to comply with stringent environmental norms, the adoption of lubricants with minimized adverse environmental effects becomes increasingly crucial. Ongoing technological advancements and innovations in lubricant formulations significantly expand the Automotive Lubricants Market. Continuous research and development efforts target the creation of lubricants tailored to meet specific industry demands, addressing challenges posed by evolving machinery designs and operational environments. The development of bio-based lubricants derived from renewable sources bolsters market growth, aligning with the global drive towards sustainable practices.

The escalating complexity and sophistication of machinery and equipment also fuel the demand for specialized lubricants. Contemporary machinery operates under demanding conditions, necessitating lubricants capable of delivering superior protection, thermal stability, and compatibility with diverse materials. High-performance lubricants precisely offer these attributes providing to the evolving needs of advanced machinery across industries.

Higher Upfront Costs of Synthetic and Bio-Based Lubricants Deter Immediate Adoption Despite Long-Term Savings Potential

The automotive lubricants market encounters a significant impediment due to the elevated initial costs linked with synthetic and bio-based lubricants when compared to conventional mineral oils. Despite the significant long-term advantages and enhanced performance offered by these advanced lubricants, their higher upfront expenses create a significant barrier to immediate adoption. This obstacle is underpinned by a clear-cut pricing difference while synthetic and bio-based lubricants excel in efficiency, durability and environmental sustainability, their upfront procurement and application costs surpass those of traditional mineral oils. This financial contrast serves as a formidable deterrent, particularly for budget-conscious consumers and businesses, deterring their transition, especially when the immediate benefits have not been readily visible or quantifiable.

A prevalent short-term mindset geared towards immediate affordability amplifies this constraint, with businesses, particularly smaller entities and cost-sensitive industries, prioritizing instant financial viability over potential future gains. Therefore, they exhibit hesitancy in navigating the initially higher costs associated with these advanced lubricants, impeding widespread adoption.

Automotive Lubricants Market Segment Analysis

Based on Product Type, the market is segmented into Engine Oil (Motor Oils), Transmission Oils, Hydraulic Fluids, Greases and Others. Engine Oil (Motor Oils) is expected to dominate the Automotive Lubricants Market during the forecast period. Engine oil, also known as motor oil, reigns as the dominant product type in the market due to its indispensable role in preserving engine health and facilitating optimal vehicle performance. At the core of its prominence lies its multifaceted functionality within the internal combustion engine. Engine oil acts as a lubricant, reducing friction between various moving components within the engine, thereby minimizing wear and tear while ensuring smooth operations. This fundamental function not only safeguards critical engine parts but also contributes significantly to extending the engine's lifespan, a crucial factor influencing consumer preferences. Its role in dissipating heat generated during engine operation is equally essential, preventing overheating and maintaining an optimal operating temperature.

Engine oil assists in keeping the engine clean by carrying away contaminants and debris, preventing sludge buildup and maintaining internal cleanliness, a key aspect for engine longevity and efficiency. Its versatility across diverse vehicle types, from compact cars to heavy-duty trucks and motorcycles, cements its dominance. The necessity for periodic oil changes and routine maintenance perpetuates the continuous demand for engine oil, solidifying its position as the primary and most sought-after product type in the automotive lubricants market. This necessity for frequent replenishment not only underscores its significance but also reinforces its consistent demand, making it an essential and dominant component within the automotive lubricants landscape.

In India, the Volume share of the engine oil is 88% in 2024. Engine oil dominates India's lubricant market due to the extensive use of internal combustion engine vehicles, diverse terrains demanding consistent lubrication, continued reliance on traditional vehicles, and the availability of affordable oil varieties, meeting diverse vehicle needs across the country.

Automotive Lubricants Market Regional Insights

Asia Pacific dominated the Automotive Lubricants Market in 2025 and is expected to continue its dominance over the forecast period. In the Asia-Pacific region, particularly in China and Malaysia, the demand for automotive lubricants has seen a significant surge. With Asia-Pacific leading in finished lubricant demand, the emphasis on fuel efficiency is steering the adoption of synthetic and lighter viscosity grade lubricants, particularly in the passenger car motor oil (PCMO) segment, which holds 40 percent of the Automotive Lubricants Market growth. In China, synthetic oils have seen significant annual growth, while in Malaysia, both semi-synthetic and full-synthetic PCMOs have captured almost 40 percent of the market share.

The Automotive Lubricants Market in the Asia Pacific is vibrant and strong, driven by the region's burgeoning automotive industry. With a substantial vehicle population, including two-wheelers, cars, trucks, and agricultural machinery, the demand for lubricants is consistently high. The market is influenced by factors such as increased vehicle production, diverse driving conditions, and the need for specialized lubricants to meet stringent performance requirements. The region's focus on technological advancements, stringent environmental regulations, and the shift towards synthetic and bio-based lubricants shape the dynamics of the Automotive Lubricants Market in the Asia Pacific.

India boasts a substantial vehicle population, surpassing millions of units across various categories like two-wheelers, cars, trucks, and agricultural machinery. This vast fleet fuels the strong automotive lubricants market, with demand driven by the necessity for engine maintenance and consistent lubrication. The combination of large vehicle counts and diverse vehicle types contributes significantly to the thriving automotive lubricants industry in India.

India helds a strong position in the global heavy vehicles market, standing as the largest tractor producer, second-largest bus manufacturer, and third-largest producer of heavy trucks worldwide. With an annual automobile production of 22.93 million vehicles in 2022, India boasts a substantial domestic demand and act as a key player in international exports. In 2025, the total sales of passenger vehicles reached 3.89 million, while automobile exports from India in the same year stood at 4,761,487 units. The Indian automotive sector, including its strong export orientation, is poised for continued growth.

The Government of India has introduced strategic initiatives such as the Automotive Mission Plan 2026, a scrappage policy, and a production-linked incentive scheme. These measures aim to position India as a global leader in both two-wheeler and four-wheeler markets by 2032. As a result, the automotive lubricants market in India is expected to have significant growth, aligning with the sector's expansion and advancements. The booming automobile industry's demand for lubricants is expected driven by increased production, exports and the implementation of forward-thinking policies.

Key developments

Efficient Role: Strategic Key Developments in the Market are playing an efficient role in the growth of the market. Innovation and technology are known to be the greatest influencers for the companies to devise strategies for the growth of the business thereby leading to the growth of the market. Here are a handful of these most notable advances:

July 2022 — Shell USA Incorporation and Shell Midstream Partners L.P announced a merger agreement and plan of merger whereby Shell USA would acquire all the common units representing, limited partner interests in SHLX with an approximate value of USD 1.96 billion.

Valvoline announced the sale of the global products business in August 2022 for $2.65 billion in cash. This transaction and arrangement will be an effective means of completing the separation of its global products and retail services companies to change Valvoline into a pure-play automotive service with a long-term target of 20% + earnings per share growth.

ExxonMobil, a well-known powerhouse in the automotive lubricant market, announced the final investment of its kind on the future of India in the presence of Deputy Chief Minister Devendra Fadnavis in May 2023, to construct a lubricant-manufacturing facility in Maharashtra, India. This plan will include an investment of INR 900 crore (US$ 110 million) and have the capacity to produce 159,000 kiloliters of finished lubricants a year which will also commence operations by late 2025.

Tecoil, a Finnish company specializing in Re-Refined Base Oils (RRBOs), was acquired by TotalEnergies in July 2025. Tecoil currently operates a 50,000 ton/year RRBO production plant in Haminia, and its integration within TotalEnergies will facilitate the accelerated deployment of RRB0s in the formulation of high-end lubricants to meet the increasing customer demands for high-performance eco-friendly products.

Automotive Lubricants Market Scope: Inquire before buying

| Automotive Lubricants Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 89.9 USD Billion |

| Forecast Period 2026-2032 CAGR: | 3.6% | Market Size in 2032: | 115.16 USD Billion |

| Segments Covered: | by Product Type | Engine Oil (Motor Oils) Transmission Oils Hydraulic Fluids Greases Others |

|

| by Base Oil Type | Mineral Oil Synthetic Oil Semi-Synthetic Oil Bio-Based Lubricants |

||

| by Additive Type | Dispersants Detergents Anti-wear Additives Viscosity Index Improvers Antioxidants Corrosion Inhibitors |

||

| by Vehicle Type | Passenger Vehicles Commercial Vehicles Motorcycles Others |

||

| by Application | Engine Components Gear & Transmission Systems Brake Systems Cooling Systems Chassis & Bearings |

||

Automotive Lubricants Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and Rest of Europe)

Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina Rest of South America)

Automotive Lubricants Market, Key Players

Global

1. ExxonMobil Corporation (Irving, Texas, United States)

2. Royal Dutch Shell (The Hague, Netherlands)

3. BP Plc (London, United Kingdom)

4. Chevron Corporation (San Ramon, California, United States)

5. TotalEnergies (Paris, France)

North America

1. Valvoline (Lexington, Kentucky, United States)

2. Amsoil Inc. (Superior, Wisconsin, United States)

3. Pennzoil (Shell) (Houston, Texas, United States)

4. Phillips 66 Lubricants (Houston, Texas, United States)

5. Houghton International Inc. (Valley Forge, Pennsylvania, United States)

Europe

1. Fuchs Petrolub SE (Mannheim, Germany)

2. Castrol (BP) (Pangbourne, United Kingdom)

3. Gulf Oil International (London, United Kingdom)

4. Morris Lubricants (Shrewsbury, United Kingdom)

5. Motul (Aubervilliers, France)

6. ENI (Rome, Italy)

7. Neste Oyj (Espoo, Finland)

Asia Pacific

1. Idemitsu Kosan Co., Ltd. (Tokyo, Japan)

2. Petronas Lubricants International (Kuala Lumpur, Malaysia)

3. Sinopec Lubricant Company (Beijing, China)

4. PetroChina Lubricant Company (Beijing, China)

5. Indian Oil Corporation Limited (IOCL) (New Delhi, India)