Automotive Engine Management System Market Size – Industry Structure Evaluation, Demand Drivers Analysis, Regional Growth Analysis and Identification, Competitive Positioning Review & Global Market Size Forecast to 2032

Overview

Automotive Engine Management System Market size was valued at US$ 98.18 Bn. in 2023 and the total revenue is expected to grow at a CAGR of 5.7% through 2024 to 2030, reaching nearly US$ 144.73 Bn.

Automotive Engine Management System Market Overview

An Automotive Engine Management System (EMS) optimizes the performance of internal combustion engines by controlling fuel injection, ignition timing, and emissions. It uses sensors, actuators, and an Engine Control Unit (ECU) to ensure efficient engine operation, reduced fuel consumption, and compliance with emission regulations. The Automotive Engine Management System Market is driven by advancements in vehicle technology, increased demand for fuel efficiency, and stricter emission regulations. EMS integrates sensors, actuators, and engine control units (ECUs) to improve vehicle performance. With the shift towards hybrid and electric vehicles, EMS technology is evolving to incorporate sophisticated software and microcontrollers. Key players such as Bosch, Continental, Denso, and Delphi Technologies dominate the market, supplying components to automotive OEMs globally. The market is growing due to the increasing production of vehicles and rising consumer expectations for enhanced driving performance, fuel economy, and environmental sustainability.

To know about the Research Methodology :- Request Free Sample Report

Automotive Engine Management System Market Dynamics

Technological Advancements

Advances in electronics, sensors, and software technologies have transformed the automotive engine management system landscape. The growing use of AI-based control algorithms, data-driven engine diagnostics, and real-time adaptation to driving conditions have made these systems more efficient. Innovations in hybrid engine integration and electric powertrain control further bolster the market. The ability to fine-tune engine performance to reduce emissions and enhance fuel efficiency will continue to drive technological advancements in this segment.

Industry Demand

The rise in vehicle production, particularly in regions like Asia-Pacific, where emerging markets are rapidly adopting advanced vehicle technologies, has fueled the demand for automotive engine management systems. Additionally, the automotive industry's ongoing shift towards electric vehicles (EVs) and hybrid electric vehicles (HEVs) has further accelerated the adoption of powertrain control and fuel management systems. This increased demand for more efficient powertrains is expected to drive innovation and the continued integration of engine management solutions in vehicles.

Regulatory Support

Governments worldwide continue to introduce stringent environmental regulations, especially targeting emissions and fuel efficiency. Regulations like Euro 6 in Europe, China 6 standards, and U.S. EPA Tier 3 have necessitated advanced automotive engine management systems. The evolving regulatory frameworks compel automakers to invest in technologies that ensure vehicles meet these standards. This demand for compliance is a key driver for the engine management systems market.

Automotive Engine Management System Market Drivers

Technological Advancements

The automotive engine management system market has benefited immensely from innovations in electronic control units (ECUs), sensors, and algorithms. Advanced engine management systems now utilize sophisticated sensor technologies, including oxygen sensors, pressure sensors, and temperature sensors, that continuously monitor engine performance. These technologies enable real-time monitoring and adjustments to fuel mixture, ignition timing, and exhaust gas recirculation (EGR). As a result, engine management systems are becoming more responsive, accurate, and energy-efficient, significantly improving fuel economy, emissions, and overall vehicle performance.

Industry Demand

The increasing demand for fuel-efficient vehicles and low-emission cars has spurred growth in the automotive engine management system market. With fuel prices fluctuating and environmental concerns growing, consumers and manufacturers alike are prioritizing the development and production of vehicles that deliver better fuel efficiency without sacrificing performance. This is particularly true for the growing EV and hybrid segments, where the need for advanced powertrain control and battery management systems is becoming a key feature of engine management solutions. The demand for smarter engine management systems in both gasoline and electric vehicles has spurred the development of multi-functional and adaptive technologies, driving market growth.

Regulatory Support

Global emissions standards have become increasingly stringent over the years, compelling automakers to adopt innovative engine management solutions. Government regulations such as Euro 7, Tier 3 standards, and China VI emission standards require the use of advanced engine management technologies to ensure that vehicles comply with environmental rules. These regulatory demands have driven automakers to incorporate sophisticated technologies like engine control units (ECUs), fuel management systems, and catalytic converter monitoring systems. These developments ensure that automotive manufacturers can meet the increasingly stringent environmental regulations across different regions.

Automotive Engine Management System Market Restraints

High Costs

The integration of advanced technologies into engine management systems, such as AI-driven algorithms, multi-sensor networks, and real-time adaptive controls, can increase the overall cost of automotive production. This high initial cost can act as a barrier for manufacturers, especially for small and medium-sized automakers. Additionally, the costs associated with the development and deployment of software systems and ECUs for vehicle platforms add to the expenses for both OEMs and consumers, which can limit adoption, especially in price-sensitive markets.

Regulatory Challenges

While regulatory support drives demand, the complexity of global emissions regulations creates significant challenges for automakers. Navigating different regulations across regions requires substantial investment in research and development (R&D) to ensure compliance. Automotive manufacturers must constantly update their engine management systems to keep pace with shifting regulatory requirements. This adds both time and cost to the manufacturing process and may delay the adoption of new technologies, hindering market growth.

Supply Chain Disruptions

The automotive industry, like many others, has faced significant supply chain disruptions due to global events such as the COVID-19 pandemic and the ongoing semiconductor shortage. These disruptions have affected the production and delivery of critical components for engine management systems, including sensors, ECUs, and fuel injection systems. As a result, automakers may experience delays in meeting production targets, which can hinder market growth and affect the timely adoption of newer engine management technologies.

Automotive Engine Management System Market Opportunities

Emerging markets in Asia-Pacific, Latin America, and Africa present significant growth opportunities for the automotive engine management system market. With rising disposable incomes and increasing vehicle ownership, demand for advanced vehicle technologies is expected to surge. Additionally, governments in these regions are implementing stricter emission standards, which will drive the need for advanced engine management solutions. The demand for fuel-efficient, low-emission vehicles in these markets will create new opportunities for OEMs to integrate next-generation engine management systems into local manufacturing processes.

Continued innovation in electric vehicles (EVs), hybrid vehicles (HEVs), and autonomous driving technologies offers considerable opportunities for engine management system manufacturers. The growth of battery management systems, hybrid powertrain solutions, and EV-specific control units will foster innovation and create a wide range of new applications for engine management technologies. The integration of advanced machine learning algorithms and smart sensors into engine management systems could further improve fuel efficiency and reduce emissions, opening up new markets and applications.

OEMs and Tier 1 suppliers are increasingly making strategic investments in engine management systems to stay competitive in a rapidly changing market. This includes investments in R&D, partnerships with software developers, and acquisitions of small tech startups to incorporate cutting-edge technology into engine management systems. These investments will not only enhance existing technologies but also drive the development of new systems capable of managing complex powertrains and enabling seamless integration of autonomous driving and electric mobility technologies.

Automotive Engine Management System Market Segment Analysis

Automotive Engine Management System Market Segmentation, by Component

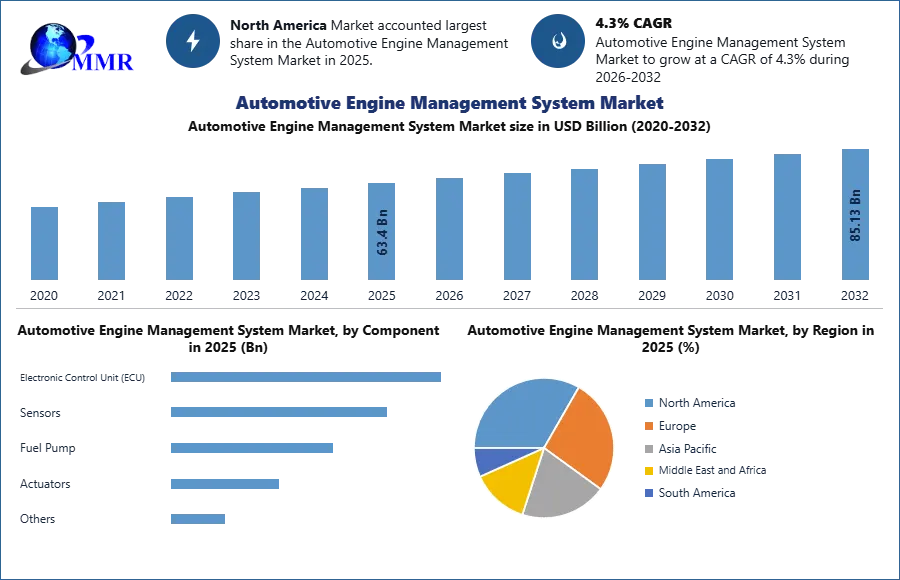

In 2025, the Electronic Control Unit (ECU) segment was the largest in the Automotive Engine Management System Market. The ECU plays a critical role in controlling engine functions such as ignition timing, fuel injection, and air-to-fuel ratio. ECUs are central to the operation of internal combustion engines and have become even more integral with the rise of electric vehicles (EVs) and hybrid engines. Demand for advanced ECUs has surged, driven by the growing adoption of sophisticated engine management systems to meet stringent emissions regulations and fuel efficiency standards. These units enable real-time monitoring, adaptive control, and diagnostic capabilities, supporting higher levels of engine performance and emission control.

The Sensors segment followed closely, driven by increasing requirements for emission control systems and safety standards. Sensors, such as oxygen and pressure sensors, are vital for monitoring the internal conditions of the engine and adjusting the ECU parameters accordingly. These systems ensure that engines operate efficiently, particularly in hybrid and electric vehicles, which rely on precise control to maximize energy use and minimize emissions.

The Fuel Pump segment, although smaller than ECUs and sensors, is crucial for controlling fuel delivery in gasoline and diesel engines. This segment saw strong growth as automakers increasingly focused on improving fuel efficiency and emissions control, particularly with the rise of direct injection systems.

Actuators are also essential as they enable the physical adjustments in the engine, such as controlling the throttle and the exhaust system. These components are critical for improving engine responsiveness and fuel efficiency, particularly in performance vehicles and electric vehicles where precise control over power output is vital.

Automotive Engine Management System Market Segmentation, by Engine Type

The Gasoline Engines segment was the largest in 2025, primarily driven by the continuing popularity of gasoline-powered vehicles, particularly in passenger cars and light commercial vehicles. The adoption of advanced engine management systems in gasoline engines helped manufacturers meet emission regulations and improve fuel efficiency. Technological innovations in fuel injection systems, variable valve timing, and turbocharging have made gasoline engines more efficient, further boosting demand for sophisticated engine management solutions.

Diesel Engines followed as a significant segment, especially in commercial vehicles and heavy-duty trucks. Diesel engines are known for their efficiency in long-distance travel and high-torque applications, making them crucial in the commercial vehicle segment. However, they have come under scrutiny due to their higher emissions compared to gasoline engines, which has led to a greater demand for emission control systems and advanced ECU technologies.

Hybrid Engines have witnessed robust growth in recent years, driven by increasing demand for environmentally friendly and fuel-efficient solutions. The Hybrid Engines segment has gained traction, particularly in passenger cars, where consumers seek a balance between gasoline and electric power. The integration of electric motors with gasoline or diesel engines has made hybrid vehicles a popular choice, increasing the adoption of advanced engine management systems.

The Electric Engines segment saw an increase in demand due to the growing shift towards electric mobility. Electric vehicles (EVs) do not require traditional engine management systems in the same way as internal combustion engines, but they do rely on battery management systems and electric powertrain control units to optimize performance and range. As EV adoption rises, so does the demand for innovative engine management solutions tailored to electric and hybrid vehicles

Automotive Engine Management System Market Regional Analysis

In 2025, North America was the leading region in the Automotive Engine Management System Market, driven by a strong industrial base, advanced technology adoption, and supportive regulatory frameworks. The United States, in particular, played a central role due to the presence of major automotive manufacturers, such as General Motors, Ford, Tesla, and Fiat Chrysler Automobiles. The region also benefits from an advanced testing infrastructure for automotive systems, which encourages continuous R&D and innovation in engine management systems. Furthermore, policy support in the form of stringent emissions regulations like EPA Tier 3 and California Air Resources Board (CARB) standards have compelled automakers in North America to invest in advanced engine management technologies. The growth of electric vehicles (EVs) and the development of autonomous vehicles further increased demand for advanced engine management systems, ensuring North America's dominance in 2025.

Objective of the Global Automotive Engine Management System Market:

The objective of the report is to present a comprehensive analysis of Global Automotive Engine Management System Market including all the stakeholders of the industry. The past and current status of the industry with forecasted market size and trends are presented in the report with the analysis of complicated data in simple language. The report covers all aspects of the industry with a dedicated study of key players that includes market leaders, followers and new entrants by region.

PORTER, SWOT, PESTEL analysis with the potential impact of micro-economic factors by region on the market are presented in the report. External as well as internal factors that are supposed to affect the business positively or negatively have been analyzed, which will give a clear futuristic view of the industry to the decision-makers. The report also helps in understanding Global Automotive Engine Management System Market dynamics, structure by analyzing the market segments and project the Global Market size.

Clear representation of competitive analysis of key players by type, price, financial position, product portfolio, growth strategies, and regional presence in the Global Automotive Engine Management System Market make the report investor’s guide.

Global Automotive Engine Management System Market is studied by Various Segments:

The report from Maximize market research provides the detail study of various segments of the Global Automotive Engine Management System Market:

The report study has analyzed revenue impact of covid-19 pandemic on the sales revenue of market leaders, market followers and disrupters in the report and same is reflected in our analysis.

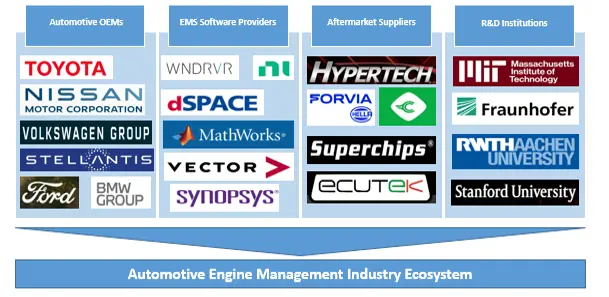

Automotive Engine Management System Industry Ecosystem

Scope of the Global Automotive Engine Management System Market: Inquire before buying

| Automotive Engine Management System Market | |||

|---|---|---|---|

| Report Coverage | Details | ||

| Base Year: | 2025 | Forecast Period: | 2026-2032 |

| Historical Data: | 2020 to 2025 | Market Size in 2025: | 63.4 USD Billion |

| Forecast Period 2026-2032 CAGR: | 4.5% | Market Size in 2032: | 86.28 USD Billion |

| Segments Covered: | by Component | Electronic Control Unit (ECU) Sensors Fuel Pump Actuators Others |

|

| by Engine Type | Gasoline Engines Diesel Engines Hybrid Engines Electric Engines |

||

| by Vehicle Type | Passenger Cars Light Commercial Vehicles (LCVs) Heavy Commercial Vehicles (HCVs) Two-Wheelers |

||

| by Communication Technology | CAN LIN Flexray |

||

Global Automotive Engine Management System Market, by Region

North America (United States, Canada and Mexico)

Europe (UK, France, Germany, Italy, Spain, Sweden, Austria, Turkey, Russia and Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN and Rest of APAC)

Middle East and Africa (South Africa, GCC, Egypt, Nigeria and Rest of ME&A)

South America (Brazil, Argentina, Columbia and Rest of South America)

Recent Developments

Key Players/Competitors Profiles Covered in the Automotive Engine Management System Market Report in Strategic Perspective

- Bosch

- Continental AG

- Delphi Technologies

- Denso Corporation

- Magneti Marelli S.p.A.

- Hitachi Automotive Systems

- Aisin Seiki Co., Ltd.

- Honeywell International Inc.

- Lear Corporation

- Mahle GmbH

- BorgWarner Inc.

- ZF Friedrichshafen AG

- Autoliv Inc.

- Valeo SA

- Visteon Corporation

- Eaton Corporation

- Eberspächer

- Emerson Electric Co.

- Hyundai Mobis

- Schneider Electric

- NXP Semiconductors

- Infineon Technologies

- Texas Instruments

- STMicroelectronics

- Magna International