Global Ovarian Cancer Drugs Market size was valued at USD 2.77 Bn in 2023 and is expected to reach USD 8.89 Bn by 2030, at a CAGR of 18.30%.Ovarian Cancer Drugs Market Overview

Ovarian cancer drugs refer to pharmaceutical agents specifically developed to treat ovarian cancer; a deadly disease characterized by abnormal cell growth in the ovaries. These drugs aim to inhibit tumor growth, prevent cancerous cells from spreading to other parts of the body, and improve patient survival rates. They incorporate a diverse range of treatment modalities, including chemotherapy, targeted therapy, immunotherapy and hormone therapy, tailored to the individual needs of patients based on factors such as cancer stage, molecular type, and treatment history which boost the Ovarian Cancer Drugs Market growth. Ovarian cancer drugs signify a beacon of hope in the fight against this devastating disease, offering patients the possibility of prolonged survival, improved quality of life, and a brighter future. As research continues to advance and new therapies emerge, the landscape of ovarian cancer treatment continues to evolve, providing renewed optimism for patients and healthcare providers alike in the quest for better outcomes.To know about the Research Methodology :- Request Free Sample Report The ongoing research and development efforts continue to yield innovative drug therapies, including targeted therapies, immunotherapies, and combination treatments, offering more effective and personalized approaches to combating ovarian cancer. The increasing awareness about the importance of early detection and diagnosis leads to a higher demand for treatment options, driving market growth. The collaborations between pharmaceutical companies, academic institutions, and research organizations foster synergies and accelerate the development and commercialization of novel drugs. The regulatory agencies' expedited approval processes for promising therapies facilitate market entry, expanding treatment options available to patients. The rise in the prevalence of ovarian cancer cases across the globe also contributes to Ovarian Cancer Drugs Market growth, necessitating the continuous development of new drugs to address the evolving needs of patients. The ovarian cancer drugs industry grows due to scientific advancements, strategic collaborations and growing awareness converging to drive innovation and improve outcomes for patients battling this upsetting disease.

Ovarian Cancer Drugs Market Trend

Increasing emphasis on personalized medicine and targeted therapies Targeted therapies, such as Bevacizumab and PARP inhibitors including Olaparib, Rucaparib and Niraparib, are designed to specifically target parts of cancer cells that make them different from normal cells. These drugs work by altering the way cancer cells grow, divide, repair themselves, or interact with other cells. For instance, Bevacizumab, an angiogenesis inhibitor, disrupts the formation of new blood vessels needed for tumor growth, while PARP inhibitors exploit DNA repair mechanisms to induce cancer cell death, particularly in tumors with BRCA gene mutations. These targeted therapies offer a more precise and effective approach to treatment, reducing adverse effects and improving patient outcomes, boosting Ovarian Cancer Drugs Market growth. The drugs such as Mirvetuximab soravtansine that target folate receptor-alpha (FR-alpha) proteins present in ovarian cancer cells provide options for personalized treatment strategies. As research continues to unveil new therapeutic targets and refine existing drugs, personalized medicine is poised to revolutionize ovarian cancer treatment, offering patients tailored therapies based on their unique genetic profiles and tumor characteristics. The arrival of targeted therapies marks a paradigm shift in the management of ovarian cancer, offering hope for enhanced survival and quality of life for patients. By honing in on specific molecular pathways driving tumor growth, these therapies represent a significant advancement in precision medicine. The development of companion diagnostics enables healthcare providers to identify patients who are most likely to benefit from targeted treatments, ensuring more effective and personalized care. As the field of oncology continues to embrace personalized medicine, ongoing research endeavors aim to expand the repertoire of targeted therapies and refine treatment algorithms based on individual patient profiles which further help to fuel Ovarian Cancer Drugs Market growth. Through a comprehensive understanding of tumor biology and genetics, coupled with the integration of innovative drug therapies, personalized medicine holds immense promise in reshaping the future of ovarian cancer treatment, offering new avenues for improved outcomes and prolonged survival for patients battling this formidable disease.Ovarian Cancer Drugs Market Dynamics

Increasing Prevalence of Ovarian Cancer to Boost Market Growth Ovarian cancer is one of the most lethal gynecological malignancies globally, with a significant rise in its incidence rates over the years. This rise is attributed to various factors such as lifestyle changes, environmental influences, and an aging population. As the incidence of ovarian cancer continues to escalate, there is a growing demand for effective treatments to combat this disease. Pharmaceutical companies and research institutions are investing heavily in the development of novel drugs and therapies targeting ovarian cancer. This surge in research and development activities is propelling the Ovarian Cancer Drugs Market Growth, offering patients a wider array of treatment options ranging from traditional chemotherapy to innovative targeted therapies and immunotherapies. The advancements in precision medicine and personalized treatment approaches are driving the Ovarian Cancer Drugs industry, as they enable healthcare professionals to tailor therapies based on individual patient characteristics and tumor profiles, thereby enhancing treatment efficacy and patient outcomes. The increasing prevalence of ovarian cancer underscores the urgent need for therapeutic advancements, thereby boosting the growth of the Ovarian Cancer Drugs Market. The total number of ovarian cancer cases in South Korea is steadily increasing, reflecting the global trend of rising cancer prevalence. As a response, the demand for ovarian cancer drugs is growing, prompting advancements in treatment modalities to address the escalating burden of this disease.With an aging population, the incidence of ovarian cancer is on the ascent, particularly among individuals aged 45 and above, reaching its peak between 75 and 79 years. Genetic predispositions, notably mutations in genes such as BRCA1 and BRCA2, significantly contribute to this increasing prevalence, accentuated by a family history of the disease. The previous diagnoses of cancers such as breast cancer, especially when associated with inherited genetic mutations, amplify the risk of ovarian cancer. Lifestyle factors such as hormone replacement therapy (HRT) post-menopause, smoking and obesity add to the multifaceted landscape of ovarian cancer prevalence, necessitating enhanced therapeutic interventions that boost Ovarian Cancer Drugs Market growth.

High cost associated with novel treatments and therapies to hamper Market Growth The high cost associated with novel treatments and therapies creates financial barriers for patients, limiting their access to potentially life-saving treatments. Ovarian cancer requires long-term and intensive treatment regimens, which lead to substantial out-of-pocket expenses for patients and their families. This financial burden results in treatment delays, discontinuation of therapy, or non-adherence to prescribed medications, ultimately compromising patient outcomes. The high cost of novel therapies strains healthcare systems and insurance providers, leading to challenges in reimbursement and coverage decisions that hamper Ovarian Cancer Drugs Market growth. This exacerbates disparities in access to care, particularly for underserved populations who already face socioeconomic barriers to healthcare access. The affordability of these treatments varies across different regions and healthcare systems, leading to disparities in treatment availability and outcomes. In essence, the high cost of novel ovarian cancer drugs hinders patient access, compromises healthcare affordability, and exacerbates disparities in care, thereby restraining Ovarian Cancer Drugs industry growth and innovation in the field.

Risk Factor Description Age The risk of ovarian cancer increases with age, with most cases occurring after menopause. Obesity Being overweight or obese, particularly with a body mass index (BMI) of at least 30, increase the risk of ovarian cancer. Reproductive History Delaying childbirth or never having a full-term pregnancy elevate the risk of ovarian cancer. Hormone Therapy Postmenopausal hormone therapy, particularly estrogen-alone or estrogen combined with progesterone, increases ovarian cancer risk. Family History A family history of ovarian, breast, or colorectal cancer elevates ovarian cancer risk, especially if multiple relatives are affected. Family Cancer Syndromes Certain hereditary cancer syndromes, such as hereditary breast and ovarian cancer syndrome (HBOC) and Lynch syndrome, increase ovarian cancer risk. Genetic Mutations Inherited mutations in genes like BRCA1, BRCA2, MLH1, MSH2, MSH6, and others are associated with a higher risk of ovarian cancer. Fertility Treatment Fertility treatment, particularly in vitro fertilization (IVF), slightly increases the risk of certain types of ovarian tumors. History of Breast Cancer Women with a history of breast cancer, especially those with a family history, have an increased risk of ovarian cancer. Ovarian Cancer Drugs Market Segment Analysis

Based on Drug Class, the market is categorized into PARP Inhibitors, Taxanes, Angiogenesis Inhibitors and Others. PARP Inhibitors are expected to dominate the Ovarian Cancer Drugs Market during the forecast period. PARP inhibitors have the important class for ovarian cancer treatment due to their targeted mechanism of action and significant therapeutic efficacy. By selectively inhibiting the PARP enzyme critical for DNA repair, these inhibitors induce synthetic lethality in cancer cells, particularly those harboring BRCA mutations or homologous recombination deficiency (HRD). This targeted strategy exploits cancer cells' vulnerabilities, leading to their demise while sparing healthy cells. With the approvals of Olaparib, rucaparib, and niraparib, PARP inhibitors have revolutionized ovarian cancer therapy, demonstrating effectiveness across various disease stages, including advanced, recurrent, or resistant cases. Their utility as maintenance therapy post-chemotherapy has solidified their position as a cornerstone treatment. The success of PARP inhibitors underscores their pivotal role in improving patient outcomes and reshaping the ovarian cancer treatment landscape. PARP inhibitors represent a groundbreaking advancement in ovarian cancer treatment, targeting the vital polyadenosine diphosphate-ribose polymerase (PARP) protein crucial for DNA repair within cells. By obstructing PARP activity, these inhibitors thwart the cancer cells' ability to mend DNA damage effectively, ultimately leading to their demise. Initially prescribed for BRCA-mutated metastatic ovarian cancer post-chemotherapy, their scope has expanded to encompass patients irrespective of genetic mutations. Demonstrating efficacy in advanced, recurrent, or resistant ovarian cancer, PARP inhibitors also serve as a maintenance therapy, delaying or preventing recurrence post-chemotherapy, particularly in high-grade serous ovarian cancer cases. This innovative approach offers renewed hope by disrupting cancer cell replication while sparing healthy cells, heralding a promising of improved outcomes and enhanced quality of life for ovarian cancer patients and driving Ovarian Cancer Drugs Market growth.

Ovarian Cancer Drugs Market Regional Insights

North America dominated the largest Ovarian Cancer Drugs Market share in 2023 and is expected to continue its dominance over the forecast period. ovarian cancer treatment often involves a combination of chemotherapy drugs and targeted therapies in North America. Carboplatin, a common chemotherapy agent, is frequently used alongside drugs such as paclitaxel (Taxol) to hinder the growth of cancer cells. Bevacizumab (Avastin), a targeted therapy, complements chemotherapy by obstructing the formation of new blood vessels that nourish tumors. PARP inhibitors such as olaparib (Lynparza), niraparib (Zejula), and rucaparib (Rubraca) maintain therapy for advanced ovarian cancer patients who have responded well to platinum-based chemotherapy. These medications target specific pathways within cancer cells, aiming to delay disease progression. Doxorubicin (Doxil), another chemotherapy drug, is also utilized to impede cancer cell growth. Treatment plans are customized based on factors such as cancer stage, patient history, and response to prior therapies, prominence the importance of discussing individualized options with healthcare providers. While these drugs constitute standard treatments as of my last update, ongoing research and development lead to new therapeutic options in the future. In North America, the advancement of ovarian cancer drugs is being significantly driven by recent advances in the field. Shorla Oncology's SH-105, an innovative formulation of a well-established drug awaiting FDA approval, stands out as a promising treatment option for ovarian cancer. Its streamlined administration process, offering a ready-to-administer injectable product, is set to revolutionize drug preparation protocols. The FDA’s recent approval of Cytalux (pafolacianine) represents a milestone in imaging drugs for ovarian cancer, providing surgeons with a vital tool for identifying elusive lesions during surgical procedures which help to drive Ovarian Cancer Drugs Market growth. The harshness of ovarian cancer, which ranks among the most lethal reproductive system cancers in North America, these advancements with SH-105 and Cytalux hold immense potential in advancing patient outcomes and catalyzing innovation within the realm of oncology treatments.The Scope of the Global Ovarian Cancer Drugs Market:Inquire before buying

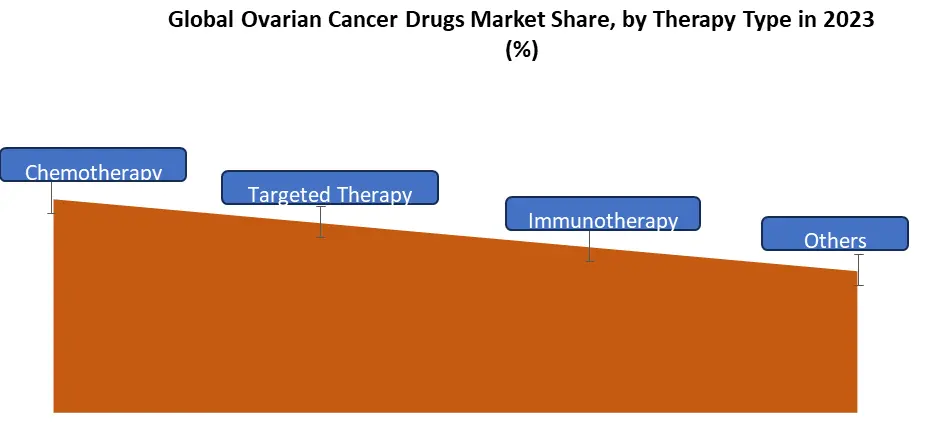

Global Ovarian Cancer Drugs Market Report Coverage Details Base Year: 2023 Forecast Period: 2024-2030 Historical Data: 2018 to 2023 Market Size in 2023: US $ 2.77 Bn. Forecast Period 2024 to 2030 CAGR: 18.30% Market Size in 2030: US $ 8.98 Bn. Segments Covered: by Therapy Type Chemotherapy Targeted Therapy Immunotherapy Others by Drug Class PARP Inhibitors Taxanes Angiogenesis Inhibitors Others by Distribution Channel Hospital Pharmacy Drug Stores and Retail Pharmacy Wholesalers and Distributors Online Pharmacies Others Ovarian Cancer Drugs Market, By Region

North America (United States, Canada and Mexico) Europe (UK, France, Germany, Italy, Spain, Sweden, Austria and the Rest of Europe) Asia Pacific (China, South Korea, Japan, India, Australia, Indonesia, Malaysia, Vietnam, Taiwan, Bangladesh, Pakistan and the Rest of APAC) South America (Brazil, Argentina Rest of South America) Middle East & Africa (South Africa, GCC, Egypt, Nigeria and the Rest of ME&AOvarian Cancer Drugs Key players

Global 1. Pfizer Inc. (New York City, New York, United States) 2. Roche Holding AG (Basel, Switzerland) 3. AstraZeneca (Cambridge, United Kingdom) 4. Merck & Co., Inc. (Kenilworth, New Jersey, United States) 5. Novartis AG (Basel, Switzerland) North America 1. Bristol Myers Squibb (New York City, New York, United States) 2. AbbVie Inc. (North Chicago, Illinois, United States) 3. Johnson & Johnson (New Brunswick, New Jersey, United States) 4. Celgene Corporation (Summit, New Jersey, United States) 5. Amgen Inc. (Thousand Oaks, California, United States) 6. Eli Lilly and Company (Indianapolis, Indiana, United States) 7. Biogen Inc. (Cambridge, Massachusetts, United States) 8. Genentech, Inc. (South San Francisco, California, United States) Europe 1. GlaxoSmithKline (GSK) (Brentford, United Kingdom) 2. Bayer AG (Leverkusen, Germany) 3. Sanofi (Paris, France) Asia Pacific 1. Eisai Co., Ltd. (Tokyo, Japan) 2. Takeda Pharmaceutical Company Limited (Tokyo, Japan) 3. Daiichi Sankyo Company, Limited (Tokyo, Japan) Frequently Asked Questions: 1] What is the growth rate of the Global Ovarian Cancer Drugs Market? Ans. The Global Ovarian Cancer Drugs Market is growing at a significant rate of 18.30% during the forecast period. 2] Which region is expected to dominate the Global Ovarian Cancer Drugs Market? Ans. North America is expected to dominate the Ovarian Cancer Drugs Market during the forecast period. 3] What is the expected Global Ovarian Cancer Drugs Market size by 2030? Ans. The Ovarian Cancer Drugs Market size is expected to reach USD 8.98 Billion by 2030. 4] Which are the top players in the Global Ovarian Cancer Drugs Market? Ans. The major top players in the Global Ovarian Cancer Drugs Market are Pfizer Inc. (New York City, New York, United States), Roche Holding AG (Basel, Switzerland), AstraZeneca (Cambridge, United Kingdom), Merck & Co., Inc. (Kenilworth, New Jersey, United States), Novartis AG (Basel, Switzerland) and Others. 5] What are the factors driving the Global Ovarian Cancer Drugs Market growth? Ans. The increasing prevalence of Ovarian Cancer and advancements in treatment modalities are expected to drive market growth during the forecast period.

1. Ovarian Cancer Drugs Market Introduction 1.1. Study Assumption and Market Definition 1.2. Scope of the Study 1.3. Executive Summary 2. Ovarian Cancer Drugs Market: Dynamics 2.1. Ovarian Cancer Drugs Market Trends by Region 2.1.1. North America Ovarian Cancer Drugs Market Trends 2.1.2. Europe Ovarian Cancer Drugs Market Trends 2.1.3. Asia Pacific Ovarian Cancer Drugs Market Trends 2.1.4. Middle East and Africa Ovarian Cancer Drugs Market Trends 2.1.5. South America Ovarian Cancer Drugs Market Trends 2.2. Ovarian Cancer Drugs Market Dynamics by Region 2.2.1. North America 2.2.1.1. North America Ovarian Cancer Drugs Market Drivers 2.2.1.2. North America Ovarian Cancer Drugs Market Restraints 2.2.1.3. North America Ovarian Cancer Drugs Market Opportunities 2.2.1.4. North America Ovarian Cancer Drugs Market Challenges 2.2.2. Europe 2.2.2.1. Europe Ovarian Cancer Drugs Market Drivers 2.2.2.2. Europe Ovarian Cancer Drugs Market Restraints 2.2.2.3. Europe Ovarian Cancer Drugs Market Opportunities 2.2.2.4. Europe Ovarian Cancer Drugs Market Challenges 2.2.3. Asia Pacific 2.2.3.1. Asia Pacific Ovarian Cancer Drugs Market Drivers 2.2.3.2. Asia Pacific Ovarian Cancer Drugs Market Restraints 2.2.3.3. Asia Pacific Ovarian Cancer Drugs Market Opportunities 2.2.3.4. Asia Pacific Ovarian Cancer Drugs Market Challenges 2.2.4. Middle East and Africa 2.2.4.1. Middle East and Africa Ovarian Cancer Drugs Market Drivers 2.2.4.2. Middle East and Africa Ovarian Cancer Drugs Market Restraints 2.2.4.3. Middle East and Africa Ovarian Cancer Drugs Market Opportunities 2.2.4.4. Middle East and Africa Ovarian Cancer Drugs Market Challenges 2.2.5. South America 2.2.5.1. South America Ovarian Cancer Drugs Market Drivers 2.2.5.2. South America Ovarian Cancer Drugs Market Restraints 2.2.5.3. South America Ovarian Cancer Drugs Market Opportunities 2.2.5.4. South America Ovarian Cancer Drugs Market Challenges 2.3. PORTER’s Five Forces Analysis 2.4. PESTLE Analysis 2.5. Technology Roadmap 2.6. Regulatory Landscape by Region 2.6.1. North America 2.6.2. Europe 2.6.3. Asia Pacific 2.6.4. Middle East and Africa 2.6.5. South America 2.7. Key Opinion Leader Analysis For Ovarian Cancer Drugs Industry 2.8. Analysis of Government Schemes and Initiatives For Ovarian Cancer Drugs Industry 2.9. Ovarian Cancer Drugs Market Trade Analysis 2.10. The Global Pandemic Impact on Ovarian Cancer Drugs Market 3. Ovarian Cancer Drugs Market: Global Market Size and Forecast by Segmentation by Demand and Supply Side (by Value in USD Million) 2023-2030 3.1. Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 3.1.1. Chemotherapy 3.1.2. Targeted Therapy 3.1.3. Immunotherapy 3.1.4. Others 3.2. Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 3.2.1. PARP Inhibitors 3.2.2. Taxanes 3.2.3. Angiogenesis Inhibitors 3.2.4. Others 3.3. Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 3.3.1. Hospital Pharmacy 3.3.2. Drug Stores and Retail Pharmacy 3.3.3. Wholesalers and Distributors 3.3.4. Online Pharmacies 3.3.5. Others 3.4. Ovarian Cancer Drugs Market Size and Forecast, by Region (2023-2030) 3.4.1. North America 3.4.2. Europe 3.4.3. Asia Pacific 3.4.4. Middle East and Africa 3.4.5. South America 4. North America Ovarian Cancer Drugs Market Size and Forecast by Segmentation (by Value in USD Million) 2023-2030 4.1. North America Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 4.1.1. Chemotherapy 4.1.2. Targeted Therapy 4.1.3. Immunotherapy 4.1.4. Others 4.2. North America Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 4.2.1. PARP Inhibitors 4.2.2. Taxanes 4.2.3. Angiogenesis Inhibitors 4.2.4. Others 4.3. North America Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 4.3.1. Hospital Pharmacy 4.3.2. Drug Stores and Retail Pharmacy 4.3.3. Wholesalers and Distributors 4.3.4. Online Pharmacies 4.3.5. Others 4.4. North America Ovarian Cancer Drugs Market Size and Forecast, by Country (2023-2030) 4.4.1. United States 4.4.1.1. United States Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 4.4.1.1.1. Chemotherapy 4.4.1.1.2. Targeted Therapy 4.4.1.1.3. Immunotherapy 4.4.1.1.4. Others 4.4.1.2. United States Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 4.4.1.2.1. PARP Inhibitors 4.4.1.2.2. Taxanes 4.4.1.2.3. Angiogenesis Inhibitors 4.4.1.2.4. Others 4.4.1.3. United States Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 4.4.1.3.1. Hospital Pharmacy 4.4.1.3.2. Drug Stores and Retail Pharmacy 4.4.1.3.3. Wholesalers and Distributors 4.4.1.3.4. Online Pharmacies 4.4.1.3.5. Others 4.4.2. Canada 4.4.2.1. Canada Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 4.4.2.1.1. Chemotherapy 4.4.2.1.2. Targeted Therapy 4.4.2.1.3. Immunotherapy 4.4.2.1.4. Others 4.4.2.2. Canada Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 4.4.2.2.1. PARP Inhibitors 4.4.2.2.2. Taxanes 4.4.2.2.3. Angiogenesis Inhibitors 4.4.2.2.4. Others 4.4.2.3. Canada Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 4.4.2.3.1. Hospital Pharmacy 4.4.2.3.2. Drug Stores and Retail Pharmacy 4.4.2.3.3. Wholesalers and Distributors 4.4.2.3.4. Online Pharmacies 4.4.2.3.5. Others 4.4.3. Mexico 4.4.3.1. Mexico Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 4.4.3.1.1. Chemotherapy 4.4.3.1.2. Targeted Therapy 4.4.3.1.3. Immunotherapy 4.4.3.1.4. Others 4.4.3.2. Mexico Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 4.4.3.2.1. PARP Inhibitors 4.4.3.2.2. Taxanes 4.4.3.2.3. Angiogenesis Inhibitors 4.4.3.2.4. Others 4.4.3.3. Mexico Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 4.4.3.3.1. Hospital Pharmacy 4.4.3.3.2. Drug Stores and Retail Pharmacy 4.4.3.3.3. Wholesalers and Distributors 4.4.3.3.4. Online Pharmacies 4.4.3.3.5. Others 5. Europe Ovarian Cancer Drugs Market Size and Forecast by Segmentation (by Value in USD Million) 2023-2030 5.1. Europe Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 5.2. Europe Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 5.3. Europe Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 5.4. Europe Ovarian Cancer Drugs Market Size and Forecast, by Country (2023-2030) 5.4.1. United Kingdom 5.4.1.1. United Kingdom Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 5.4.1.2. United Kingdom Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 5.4.1.3. United Kingdom Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 5.4.2. France 5.4.2.1. France Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 5.4.2.2. France Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 5.4.2.3. France Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 5.4.3. Germany 5.4.3.1. Germany Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 5.4.3.2. Germany Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 5.4.3.3. Germany Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 5.4.4. Italy 5.4.4.1. Italy Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 5.4.4.2. Italy Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 5.4.4.3. Italy Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 5.4.5. Spain 5.4.5.1. Spain Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 5.4.5.2. Spain Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 5.4.5.3. Spain Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 5.4.6. Sweden 5.4.6.1. Sweden Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 5.4.6.2. Sweden Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 5.4.6.3. Sweden Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 5.4.7. Austria 5.4.7.1. Austria Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 5.4.7.2. Austria Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 5.4.7.3. Austria Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 5.4.8. Rest of Europe 5.4.8.1. Rest of Europe Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 5.4.8.2. Rest of Europe Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 5.4.8.3. Rest of Europe Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 6. Asia Pacific Ovarian Cancer Drugs Market Size and Forecast by Segmentation (by Value in USD Million) 2023-2030 6.1. Asia Pacific Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 6.2. Asia Pacific Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 6.3. Asia Pacific Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 6.4. Asia Pacific Ovarian Cancer Drugs Market Size and Forecast, by Country (2023-2030) 6.4.1. China 6.4.1.1. China Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 6.4.1.2. China Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 6.4.1.3. China Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 6.4.2. S Korea 6.4.2.1. S Korea Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 6.4.2.2. S Korea Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 6.4.2.3. S Korea Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 6.4.3. Japan 6.4.3.1. Japan Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 6.4.3.2. Japan Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 6.4.3.3. Japan Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 6.4.4. India 6.4.4.1. India Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 6.4.4.2. India Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 6.4.4.3. India Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 6.4.5. Australia 6.4.5.1. Australia Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 6.4.5.2. Australia Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 6.4.5.3. Australia Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 6.4.6. Indonesia 6.4.6.1. Indonesia Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 6.4.6.2. Indonesia Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 6.4.6.3. Indonesia Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 6.4.7. Malaysia 6.4.7.1. Malaysia Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 6.4.7.2. Malaysia Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 6.4.7.3. Malaysia Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 6.4.8. Vietnam 6.4.8.1. Vietnam Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 6.4.8.2. Vietnam Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 6.4.8.3. Vietnam Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 6.4.9. Taiwan 6.4.9.1. Taiwan Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 6.4.9.2. Taiwan Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 6.4.9.3. Taiwan Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 6.4.10. Rest of Asia Pacific 6.4.10.1. Rest of Asia Pacific Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 6.4.10.2. Rest of Asia Pacific Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 6.4.10.3. Rest of Asia Pacific Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 7. Middle East and Africa Ovarian Cancer Drugs Market Size and Forecast by Segmentation (by Value in USD Million) 2023-2030 7.1. Middle East and Africa Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 7.2. Middle East and Africa Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 7.3. Middle East and Africa Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 7.4. Middle East and Africa Ovarian Cancer Drugs Market Size and Forecast, by Country (2023-2030) 7.4.1. South Africa 7.4.1.1. South Africa Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 7.4.1.2. South Africa Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 7.4.1.3. South Africa Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 7.4.2. GCC 7.4.2.1. GCC Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 7.4.2.2. GCC Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 7.4.2.3. GCC Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 7.4.3. Nigeria 7.4.3.1. Nigeria Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 7.4.3.2. Nigeria Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 7.4.3.3. Nigeria Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 7.4.4. Rest of ME&A 7.4.4.1. Rest of ME&A Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 7.4.4.2. Rest of ME&A Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 7.4.4.3. Rest of ME&A Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 8. South America Ovarian Cancer Drugs Market Size and Forecast by Segmentation (by Value in USD Million) 2023-2030 8.1. South America Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 8.2. South America Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 8.3. South America Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 8.4. South America Ovarian Cancer Drugs Market Size and Forecast, by Country (2023-2030) 8.4.1. Brazil 8.4.1.1. Brazil Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 8.4.1.2. Brazil Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 8.4.1.3. Brazil Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 8.4.2. Argentina 8.4.2.1. Argentina Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 8.4.2.2. Argentina Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 8.4.2.3. Argentina Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 8.4.3. Rest Of South America 8.4.3.1. Rest Of South America Ovarian Cancer Drugs Market Size and Forecast, by Therapy Type (2023-2030) 8.4.3.2. Rest Of South America Ovarian Cancer Drugs Market Size and Forecast, by Drug Class (2023-2030) 8.4.3.3. Rest Of South America Ovarian Cancer Drugs Market Size and Forecast, by Distribution Channel (2023-2030) 9. Global Ovarian Cancer Drugs Market: Competitive Landscape 9.1. MMR Competition Matrix 9.2. Competitive Landscape 9.3. Key Players Benchmarking 9.3.1. Company Name 9.3.2. Business Segment 9.3.3. End-user Segment 9.3.4. Revenue (2022) 9.3.5. Company Locations 9.4. Leading Ovarian Cancer Drugs Market Companies, by market capitalization 9.5. Market Structure 9.5.1. Market Leaders 9.5.2. Market Followers 9.5.3. Emerging Players 9.6. Mergers and Acquisitions Details 10. Company Profile: Key Players 10.1. Pfizer Inc. (New York City, New York, United States) 10.1.1. Company Overview 10.1.2. Business Portfolio 10.1.3. Financial Overview 10.1.4. SWOT Analysis 10.1.5. Strategic Analysis 10.1.6. Scale of Operation (small, medium, and large) 10.1.7. Details on Partnership 10.1.8. Regulatory Accreditations and Certifications Received by Them 10.1.9. Awards Received by the Firm 10.1.10. Recent Developments 10.2. Roche Holding AG (Basel, Switzerland) 10.3. AstraZeneca (Cambridge, United Kingdom) 10.4. Merck & Co., Inc. (Kenilworth, New Jersey, United States) 10.5. Novartis AG (Basel, Switzerland) 10.6. Bristol Myers Squibb (New York City, New York, United States) 10.7. AbbVie Inc. (North Chicago, Illinois, United States) 10.8. Johnson & Johnson (New Brunswick, New Jersey, United States) 10.9. Celgene Corporation (Summit, New Jersey, United States) 10.10. Amgen Inc. (Thousand Oaks, California, United States) 10.11. Eli Lilly and Company (Indianapolis, Indiana, United States) 10.12. Biogen Inc. (Cambridge, Massachusetts, United States) 10.13. Genentech, Inc. (South San Francisco, California, United States) 10.14. GlaxoSmithKline (GSK) (Brentford, United Kingdom) 10.15. Bayer AG (Leverkusen, Germany) 10.16. Sanofi (Paris, France) 10.17. Eisai Co., Ltd. (Tokyo, Japan) 10.18. Takeda Pharmaceutical Company Limited (Tokyo, Japan) 10.19. Daiichi Sankyo Company, Limited (Tokyo, Japan) 11. Key Findings 12. Industry Recommendations 13. Ovarian Cancer Drugs Market: Research Methodology 14. Terms and Glossary